Consider the HullWhite model where the short rate process follows where Z t is a Brownian process

Question:

Consider the Hull–White model where the short rate process follows

![dr = [(t) art] dt + o dZt, -](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/5/7/7/460655cc0b457dfe1700577457452.jpg)

where Zt is a Brownian process under the risk neutral measure Q. Using the relation

![d[r(t)eat] = $(t)eat dt + oeat dz(t),](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/5/7/7/566655cc11eec73b1700577564073.jpg) show that

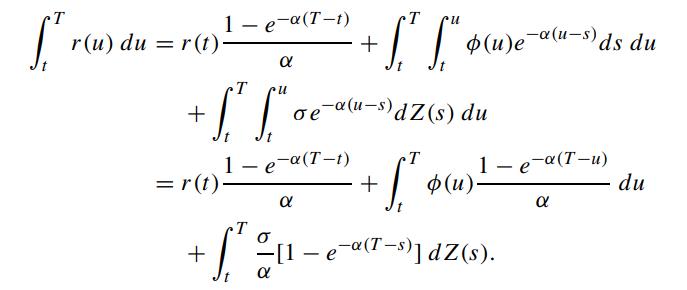

show that

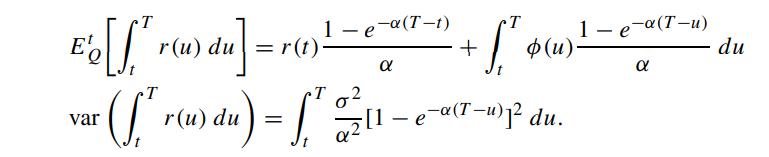

Accordingly, the mean and variance of ∫tT r(u) du are found to be

Compute the bond price B(r, t; T).

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Qurat Ul Ain

Successful writing is about matching great style with top content. As an experienced freelance writer specialising in article writing and ghostwriting, I can provide you with that perfect combination, adapted to suit your needs.

I have written articles on subjects including history, management, and finance. Much of my work is ghost-writing, so I am used to adapting to someone else's preferred style and tone. I have post-graduate qualifications in history, teaching, and social science, as well as a management diploma, and so am well equipped to research and write in these areas.

265+ Reviews

421+ Question Solved

Related Book For

Question Posted: