On January 1, 2019, Parker, Inc., a U.S.-based firm, acquired 100 percent of Suffolk PLC located in

Question:

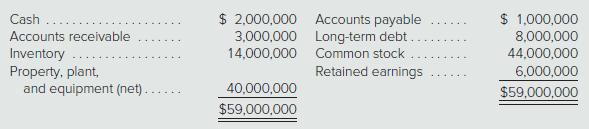

On January 1, 2019, Parker, Inc., a U.S.-based firm, acquired 100 percent of Suffolk PLC located in Great Britain for consideration paid of 52,000,000 British pounds (£), which was equal to fair value. The excess of fair value over book value is attributable to land (part of property, plant, and equipment) and is not subject to depreciation. Parker accounts for its investment in Suffolk at cost. On January 1, 2019, Suffolk reported the following balance sheet:

Suffolk’s 2019 income was recorded at £2,000,000. It declared and paid no dividends in 2019.

On December 31, 2020, two years after the date of acquisition, Suffolk submitted the following trial balance to Parker for consolidation:

Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 1,500,000

Accounts Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,200,000

Inventory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18,000,000

Property, Plant, and Equipment (net) . . . . . . . . . . . . . . . . . 36,000,000

Accounts Payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (1,450,000)

Long-Term Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (5,000,000)

Common Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (44,000,000)

Retained Earnings, 1/1/20 . . . . . . . . . . . . . . . . . . . . . . . . . (8,000,000)

Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (28,000,000)

Cost of Goods Sold . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16,000,000

Depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,000,000

Other Expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,000,000

Dividends, 1/30/20 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,750,000

–0–

Other than paying dividends, no intra-entity transactions occurred between the two companies. Relevant U.S. dollar exchange rates for the British pound follow:

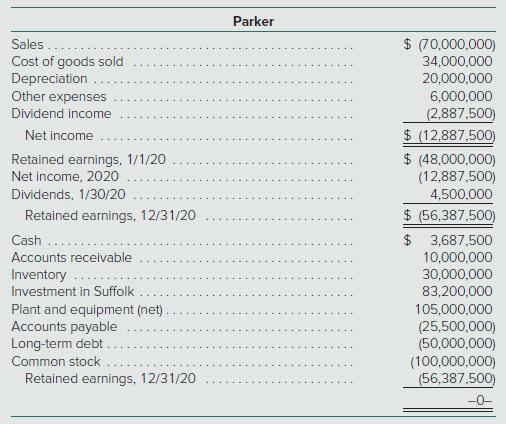

The December 31, 2020, financial statements (before consolidation with Suffolk) follow. Dividend income is the U.S. dollar amount of dividends received from Suffolk translated at the $1.65/£ exchange rate at January 30, 2020. The amounts listed for dividend income and all affected accounts (i.e., net income, December 31 retained earnings, and cash) reflect the $1.65/£ exchange rate at January 30, 2020.

Credit balances are in parentheses.

Parker’s chief financial officer (CFO) wishes to determine the effect that a change in the value of the British pound would have on consolidated net income and consolidated stockholders’ equity. To help assess the foreign currency exposure associated with the investment in Suffolk, the CFO requests assistance in comparing consolidated results under actual exchange rate fluctuations with results that would have occurred had the dollar value of the pound remained constant or declined during the first two years of Parker’s ownership.

Required

Use Excel to complete the following four parts:

Part I. Given the relevant exchange rates presented,

a. Translate Suffolk’s December 31, 2020, trial balance from British pounds to U.S. dollars. The British pound is Suffolk’s functional currency.

b. Prepare a schedule that details the change in Suffolk’s cumulative translation adjustment (beginning net assets, income, dividends, etc.) for 2019 and 2020.

c. Prepare the December 31, 2020, consolidation worksheet for Parker and Suffolk.

d. Prepare the 2020 consolidated income statement and the December 31, 2020, consolidated balance sheet.

Worksheets should possess the following qualities:

∙ Each spreadsheet should be programmed so that all relevant amounts adjust appropriately when different values of exchange rates (subsequent to January 1, 2019) are entered into it.

∙ Be sure to program Parker’s dividend income, cash, and retained earnings to reflect the dollar value of alternative January 30, 2020, exchange rates.

Part II. Repeat tasks (a), (b), (c), and (d) from Part I to determine consolidated net income and consolidated stockholders’ equity if the exchange rate had remained at $1.60/£ over the period 2019 to 2020.

Part III. Repeat tasks (a), (b), (c), and (d) from Part I to determine consolidated net income and consolidated stockholders’ equity if the following exchange rates had existed:

Part IV. Prepare a report that provides Parker’s CFO the risk assessments requested. Focus on profitability, cash flow, and the debt-to-equity ratio.

Step by Step Answer:

This assignment requires translation of foreign currency financial statements under three different sets of assumptions regarding changes in the US dollar value of the British pound Under the first se...View the full answer

Advanced Accounting

ISBN: 9781260247824

14th Edition

Authors: Joe Ben Hoyle, Thomas Schaefer, Timothy Doupnik