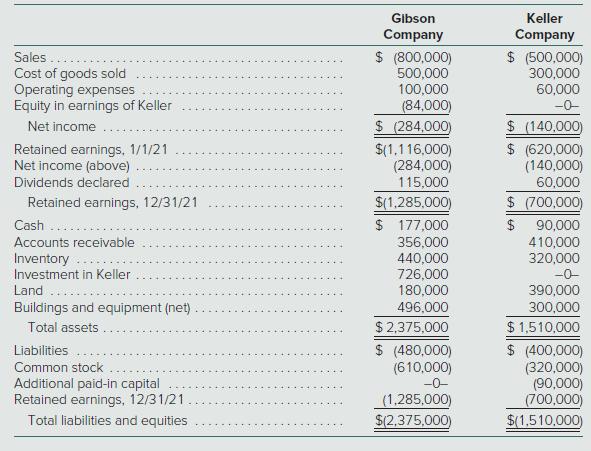

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2021,

Question:

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2021, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2020, in exchange for various considerations totaling $570,000. At the acquisition date, the fair value of the noncontrolling interest was $380,000 and Keller’s book value was $850,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $100,000. This intangible asset is being amortized over 20 years. Gibson uses the partial equity method to account for its investment in Keller.

Gibson sold Keller land with a book value of $60,000 on January 2, 2020, for $100,000. Keller still holds this land at the end of the current year. Keller regularly transfers inventory to Gibson. In 2020, it shipped inventory costing $100,000 to Gibson at a price of $150,000. During 2021, intra-entity shipments totaled $200,000, although the original cost to Keller was only $140,000. In each of these years, 20 percent of the merchandise was not resold to outside parties until the period following the transfer. Gibson owes Keller $40,000 at the end of 2021.

a. Prepare a worksheet to consolidate the separate 2021 financial statements for Gibson and Keller.

b. How would the consolidation entries in requirement (a) have differed if Gibson had sold a building on January 2, 2020, with a $60,000 book value (cost of $140,000) to Keller for $100,000 instead of land, as the problem reports? Assume that the building had a 10-year remaining life at the date of transfer.

Step by Step Answer:

Consideration transferred 570000 Noncontrolling interest fair value 380000 Subsidiary fair value at acquisitiondate 950000 Book value 850000 Fair value in excess of book value 100000 Remaining Annual ...View the full answer

Advanced Accounting

ISBN: 9781260247824

14th Edition

Authors: Joe Ben Hoyle, Thomas Schaefer, Timothy Doupnik