Andreas Broszio just started as an analyst for Credit Suisse in Geneva, Switzerland. He receives the following

Question:

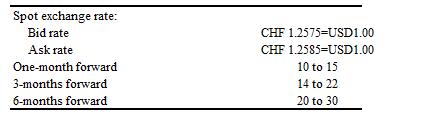

Andreas Broszio just started as an analyst for Credit Suisse in Geneva, Switzerland. He receives the following quotes for Swiss francs (CHF) against the dollar (USD) for spot, 1 month forward, 3 months forward, and 6 months forward.

a. Calculate outright quotes for bid and ask and the number of points spread between each.

b. What do you notice about the spread as quotes evolve from spot toward 6 months?

c. What is the 6-month Swiss bill rate?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a b It widens most likely a result of ...View the full answer

Answered By

Fahmin Arakkal

Tutoring and Contributing expert question and answers to teachers and students.

Primarily oversees the Heat and Mass Transfer contents presented on websites and blogs.

Responsible for Creating, Editing, Updating all contents related Chemical Engineering in

latex language

8+ Reviews

22+ Question Solved

Related Book For

Multinational Business Finance

ISBN: 9780137496013

16th Edition

Authors: David K. Eiteman, Arthur I. Stonehill, Michael H. Moffett

Question Posted: