Select the best answer for each of the following questions. Explain the reason for your selection. a.

Question:

Select the best answer for each of the following questions. Explain the reason for your selection.

a. Which of the following would be least likely to be considered an objective of internal control?

(1) Checking the accuracy and reliability of accounting data.

(2) Detecting management fraud.

(3) Encouraging adherence to managerial policies.

(4) Safeguarding assets.

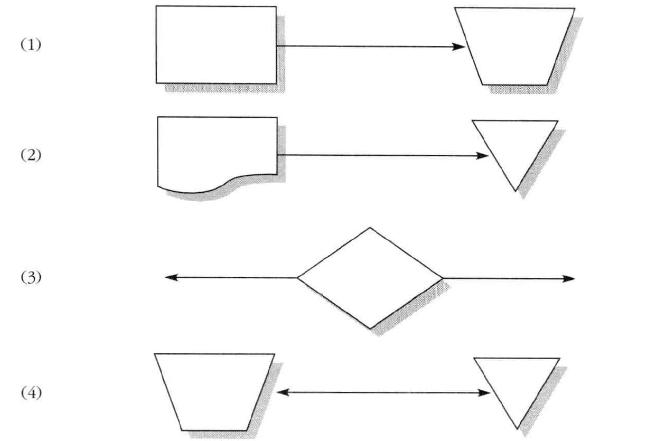

b. Which of the symbols on the following page indicate that a file has been consulted?

c. When a CPA decides that the work performed by internal auditors may have an effect on the nature, timing, and extent of the CPA's procedures, the CPA should consider the competence and objectivity of the internal auditors. Relative to objectivity, the CPA should:

(1) Consider the organizational level to which the internal auditors report the results of their work.

(2) Review the internal auditors' work.

(3) Consider the qualifications of the internal audit staff.

(4) Review the training program in effect for the internal audit staff.

d. Effective internal control in a small company that has an insufficient number of employees to permit proper separation of responsibilities can be improved by:

(1) Employment of temporary personnel to aid in the separation of duties.

(2) Direct participation by the owner in key recordkeeping and control activities of the business.

(3) Engaging a CPA to perform monthly write-up work.

(4) Delegation to each employee of full, clear-cut responsibility for a separate major transaction cycle.

e. Of the following statements about internal control, which one is not valid?

(1) No one person should be responsible for the custody and the recording of an asset.

(2) Transactions must be properly authorized before such transactions are processed.

(3) Because of the cost-benefit relationship, a client may apply controls on a test basis.

(4) Controls reasonably ensure that collusion among employees cannot occur.

f. Proper segregation of functional responsibilities calls for separation of the (1) Authorization, recordkeeping, and custodial functions.

(2) Authorization, execution, and payment functions.

(3) Receiving, shipping, and custodial functions.

(4) Authorization, approval, and execution functions.

Step by Step Answer:

Here are the best answers for each of the questions along with explanations a Least likely to be considered an objective of internal control The corre...View the full answer

Principles Of Auditing And Other Assurance Services

ISBN: 9780072327267

13th Edition

Authors: Ray Whittington, Kurt Pany