Question:

You have completed your audit of Egral Ltd, a large listed company. Your main day-to-day contact during the audit was Ms Poon, the accountant, although you also had some dealings with the finance director, Mr Sullivan, and the audit committee.

As part of completion procedures, your assistant has prepared the following draft management letter for your consideration.

Required

a. Critically analyse the draft management letter and outline suggestions for improvement.

b. Assume you found some minor errors during the audit (such as an accrual not taken up) that were rectified by the time the financial statements were issued. Would you include these in the management letter? Why or why not?

Transcribed Image Text:

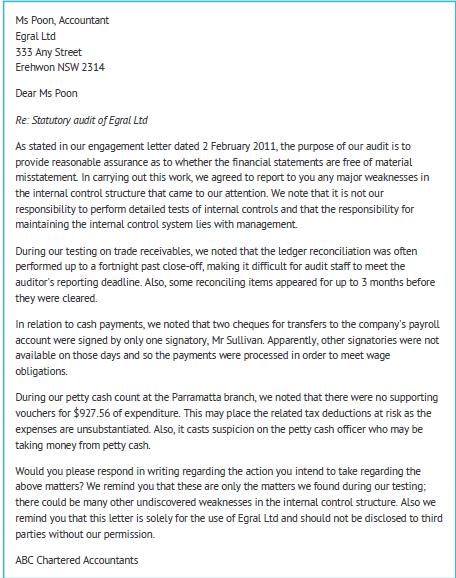

Ms Poon, Accountant Egral Ltd 333 Any Street Erehwon NSW 2314 Dear Ms Poon Re: Statutory audit of Egral Ltd As stated in our engagement letter dated 2 February 2011, the purpose of our audit is to provide reasonable assurance as to whether the financial statements are free of material misstatement. In carrying out this work, we agreed to report to you any major weaknesses in the internal control structure that came to our attention. We note that it is not our responsibility to perform detailed tests of internal controls and that the responsibility for maintaining the internal control system lies with management. During our testing on trade receivables, we noted that the ledger reconciliation was often performed up to a fortnight past close-off, making it difficult for audit staff to meet the auditor's reporting deadline. Also, some reconciling items appeared for up to 3 months before they were cleared. In relation to cash payments, we noted that two cheques for transfers to the company's payroll account were signed by only one signatory, Mr Sullivan. Apparently, other signatories were not available on those days and so the payments were processed in order to meet wage obligations. During our petty cash count at the Parramatta branch, we noted that there were no supporting vouchers for $927.56 of expenditure. This may place the related tax deductions at risk as the expenses are unsubstantiated. Also, it casts suspicion on the petty cash officer who may be taking money from petty cash. Would you please respond in writing regarding the action you intend to take regarding the above matters? We remind you that these are only the matters we found during our testing; there could be many other undiscovered weaknesses in the internal control structure. Also we remind you that this letter is solely for the use of Egral Ltd and should not be disclosed to third parties without our permission. ABC Chartered Accountants