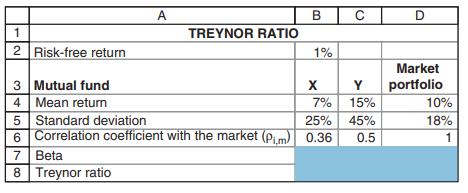

(Treynor ratio) The risk-free rate is 1%. You observe two fund managers (X and Y) and the...

Question:

(Treynor ratio) The risk-free rate is 1%. You observe two fund managers (X and Y) and the market portfolio.

a. Calculate the beta of each stock and the market portfolio

b. Calculate the Treynor ratio for each stock and the market portfolio.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Vijesh J

My passion to become a tutor is a lifetime milestone. Being a finance and marketing professional with hands-on experience in wealth management, portfolio management, team handling and actively contributing in promoting the company. Highly talented in managing and educating students in most attractive ways were students get involved. I will always give perfection to my works. Time is the most important for the works and I provide every answer on time without a delay. I will proofread each and every work and will deliver a with more perfection.

5+ Reviews

15+ Question Solved

Related Book For

Principles Of Finance Wtih Excel

ISBN: 9780190296384

3rd Edition

Authors: Simon Benninga, Tal Mofkadi

Question Posted: