Question: 5.4.11 Computer Challenge Let U0;U1; : : : be independent random variables, each uniformly distributed on the interval .0;1/. Define a stochastic process fSng recursively

5.4.11 Computer Challenge Let U0;U1; : : : be independent random variables, each uniformly distributed on the interval .0;1/. Define a stochastic process fSng recursively by setting

![]()

(This is an example of a discrete-time, continuous-state, Markov process.)

When n becomes large, the distribution of Sn approaches that of a random variable S D S1, and S must have the same probability distribution as U.1CS/, where U and S are independent. We write this in the form

![]()

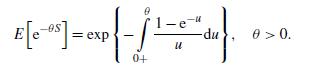

from which it is easy to determine that E[S] D 1;Var[S] D 12 , and even (the Laplace transform)

The probability density function f .s/ satisfies

What is the 99th percentile of the distribution of S? (Note: Consider the shot noise process of Section 5.4.1. When the Poisson process has rate D 1 and the impulse response function is the exponential h.x/ D expf????xg, then the shot noise I.t/ has, in the limit for large t, the same distribution as S.)

So 0 and Sn+1 = Un(1+Sn) for n > 0.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts