Question

1. On January 1, year 1, Flop Co. purchased a machine for $528,000 and depreciated it by the straight-line method using an estimated useful life

1. On January 1, year 1, Flop Co. purchased a machine for $528,000 and depreciated it by the straight-line method using an estimated useful life of eight years with no salvage value. On January 1, year 4, Flop determined that the machine had a useful life of six years from the date of acquisition and will have a salvage value of $48,000. An accounting change was made in year 4 to reflect these additional data. The accumulated depreciation for this machine should have a balance at December 31, year 4, of

a. $308,000

b. $292,000

c. $320,000

d. $352,000

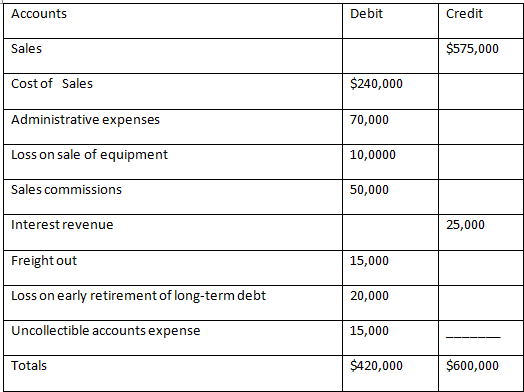

2. Flop Co.'s trial balance of income statement accounts for the year ended December 31, year 2, included the following:

Other information:

Finished goods inventory:

January 1, year 2 $400,000

December 31, year 2 360,000

Flop's income tax rate is 30%. In Flop's year 2 multiple-step income statement,

What amount should Flop report as the cost of goods manufactured?

a. $200,000

b. $295,000

c. $280,000

d. $215,000

Accounts Sales Cost of Sales Administrative expenses Loss on sale of equipment Sales commissions Interest revenue Freight out Loss on early retirement of long-term debt Uncollectible accounts expense Totals Debit $240,000 70,000 10,0000 50,000 15,000 20,000 15,000 $420,000 Credit $575,000 25,000 $600,000

Step by Step Solution

3.41 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

1 528000 x 38 198000 Accumulated Depreciation 528000 19...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: kieso, weygandt and warfield.

14th Edition

9780470587232, 470587288, 470587237, 978-0470587287