Nancy Nanny opened a child-care facility on January 1, Year 1. Use the Chart of Accounts below

Question:

Nancy Nanny opened a child-care facility on January 1, Year 1. Use the Chart of Accounts below to complete the requirements on the following pages for Nancy Nanny Child Care.

NANCY NANNY CHILD CARE?Year 1

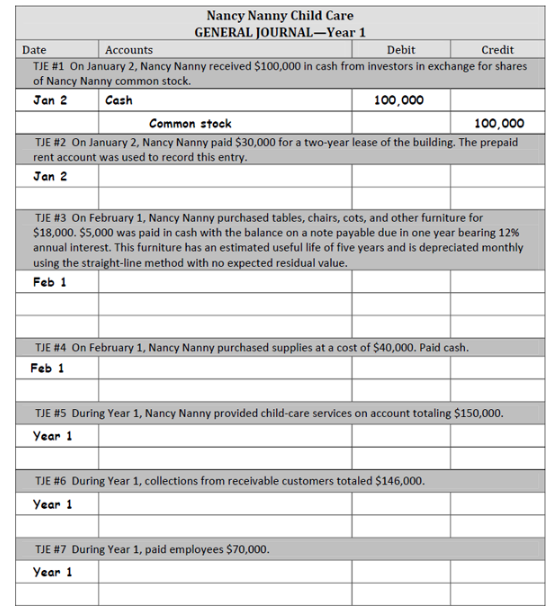

Q1 The following transactions occurred during Year 1. the first year of business, for Nancy Nanny Child Care. Record each transaction in proper journal entry format below using debits and credits.

NANCY NANNY CHII D CARE??YEAR 1

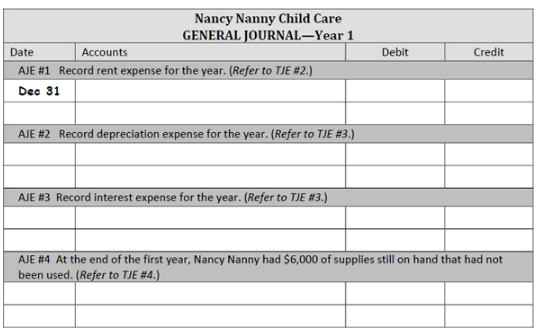

Q2 At the end of Year 1. Nancy Nanny made the following adjusting journal entries. Record each adjusting entry in proper journal entry format below using debits and credits.

NANCY NANNY CHILD CARE?Year 1

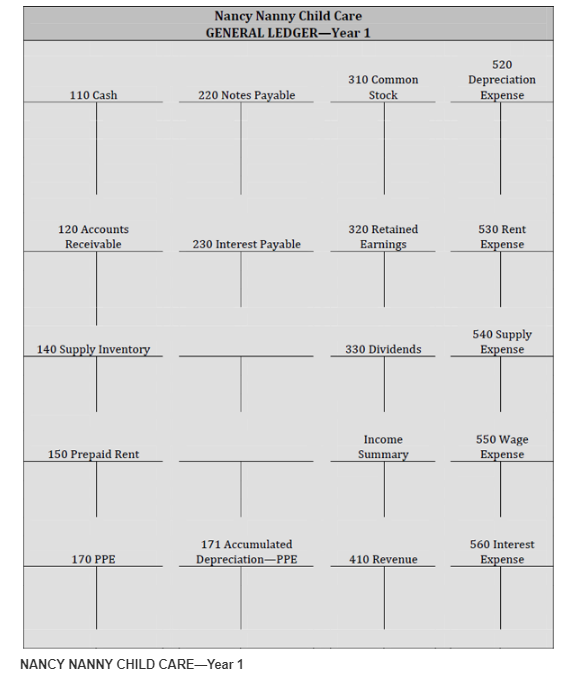

Q3 Post the Transaction Journal Entries from Q1 and the Adjusting Journal Entries from Q2 to the General Ledger below.

Q4 Compute the ending balance for each account.

NANCY NANNY CHILD CARE??Year 1

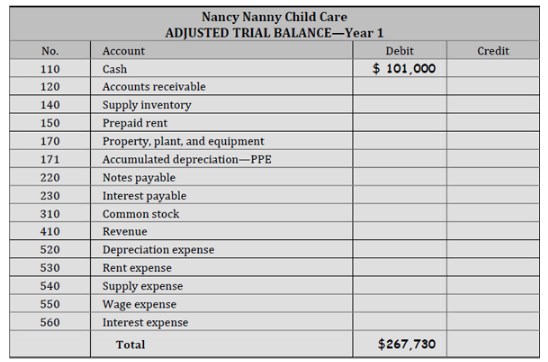

Use the ending balances computed in the General Ledger to prepare the Adjusted Trial Balance below.

NANCY NANNY CHILD CARE??Year 1

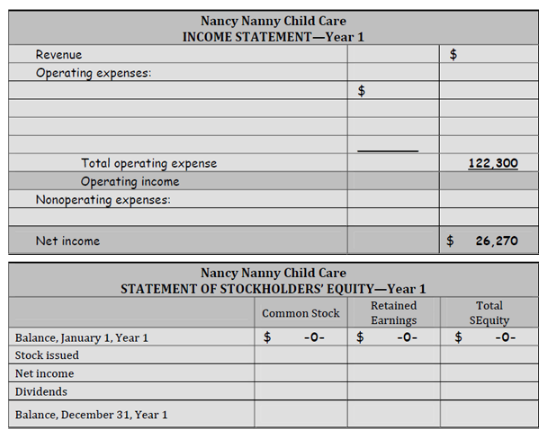

Use amounts from the Adjusted Trial Balance to prepare the Income Statement and the Statement of Stockholders? Equity. Use the forms provided below.

NANCY NANNY CHILD CARE?Year 1

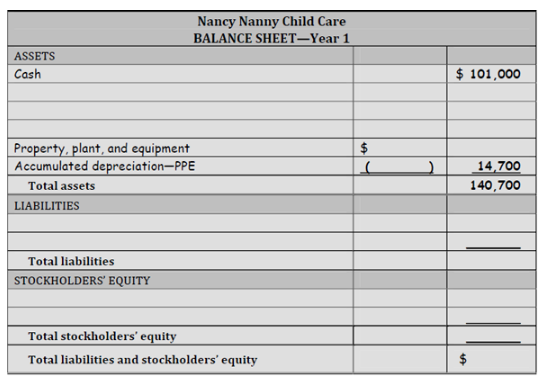

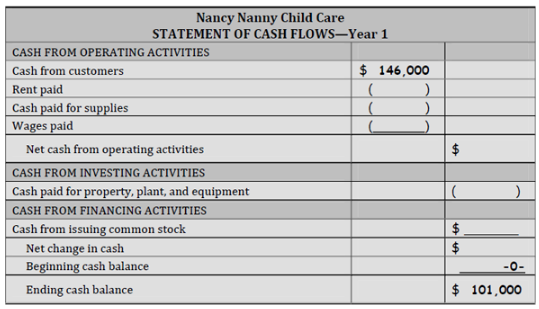

Q7 Use amounts from the General Ledger, Adjusted Trial Balance. and the Statement of Stockholders' Equity to prepare the Balance Sheet and the Statement of Cash Flows. Use the forms provided below.

NANCY NANNY CHILD CARE ??Year 1

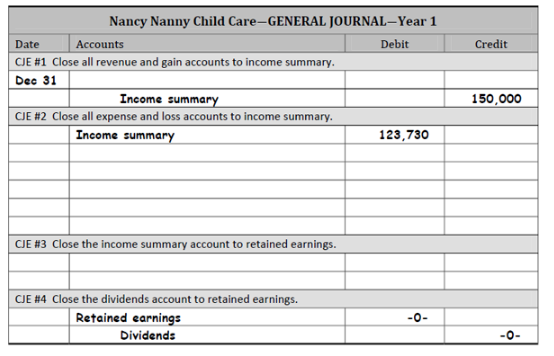

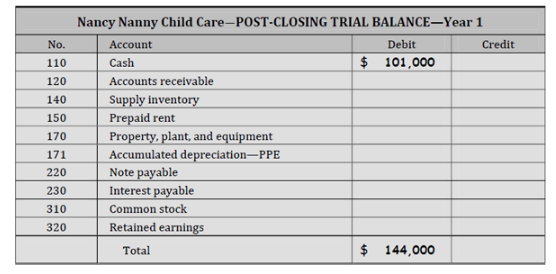

Q8 Use amounts from the Adjusted Trial Balance to prepare Closing Journal Entries and the Post-Closing Trial Balance. Use the forms provided below.

Expert Answer:

Accounting cycle Accounting cycle is the collective process of identifying and recording the transactions in journals and posting them in respective ledger accounts It also includes preparing unadjust... View the full answer

Intermediate Accounting

ISBN: 978-0324659139

11th edition

Authors: Loren A. Nikolai, John D. Bazley, Jefferson P. Jones