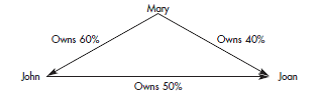

The following diagram depicts the relationships among Mary Company, Johan Company, and Joan Company on December 31, 2014: Mary Company purchases its interest in John

The following diagram depicts the relationships among Mary Company, Johan Company, and Joan Company on December 31, 2014:

Mary Company purchases its interest in John Company on January 1, 2012, for $204,000. John Company purchases its interest in Joan Company on January 1, 2013, for $75,000. Mary Company purchases its interest in Joan Company on January 1, 2014, for $72,000. All investments are accounted for under the equity method. Control over Joan Company does not occur until the January 1, 2014, acquisition. Thus, a D&D schedule will be prepared for the investment in Joan as of January 1, 2014.

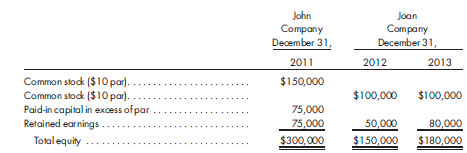

The following stockholders? equities are available:

On January 2, 2014, Joan Company sells a merchandise to Joan Company for $20,000. The machine has a book value of $10,000, with an estimated life of five years and is being depreciated on a straight-line basis.

John Company sells $20,000 of merchandise to Joan Company during 2014 to realize a gross profit of 30%. Of this merchandise, $5,000 remains in Joan Company?s December 31, 2014, inventory. Joan owes Johan $3,000 on December 31, 2014, for merchandise delivered during 2014.

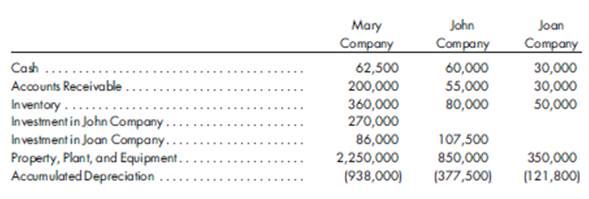

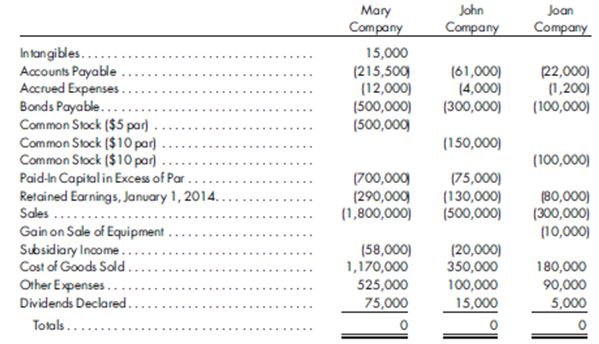

Trial balances of the three companies prepared from general ledger account balances on December 31, 2014, are as follows:

Prepare the worksheet necessary to produce the consolidated financial statements of Mary Company and its subsidiaries as of December 31, 2014. Include the determination and distribution of excess and income distribution schedules. Any excess of cost is assumed to be attributable to goodwill.

John Owns 60% Mary Owns 50% Owns 40% Joan Common stock ($10 par). Common stock ($10 par).. Paid-in capital in excess of par Retained earnings.. Total equity John Company December 31, 2011 $150,000 75,000 75,000 $300,000 Joan Company December 31, 2012 $100,000 50,000 $150,000 2013 $100,000 80,000 $180,000 Cash Accounts Receivable Inventory... Investment in John Company Investment in Joan Company. Property, Plant, and Equipment.. Accumulated Depreciation. Mary Company 62,500 200,000 360,000 270,000 John Company 60,000 55,000 80,000 86,000 107,500 2,250,000 850,000 (938,000) (377,500) Joan Company 30,000 30,000 50,000 350,000 (121,800) Intangibles..... Accounts Payable Accrued Expenses. Bonds Payable... Common Stock ($5 par). Common Stock ($10 par) Common Stock ($10 par) Paid-In Capital in Excess of Par. Retained Earnings, January 1, 2014.. Sales ...... Gain on Sale of Equipment Subsidiary Income. Cost of Goods Sold. Other Expenses.. Dividends Declared.. Totals........ Mary Company John Joan Company Company 15,000 (215,500) (61,000) (12,000) (4,000) (500,000) (300,000) (500,000) (150,000) (700,000) (75,000) (290,000) (130,000) (1,800,000) (500,000) (58,000) (20,000) 1,170,000 350,000 100,000 15,000 525,000 75,000 (22,000) (1,200) (100,000) (100,000) (80,000) (300,000) (10,000) 180,000 90,000 5,000

Step by Step Solution

3.43 Rating (143 Votes )

There are 3 Steps involved in it

Step: 1

Calculate noncontrolling interest value It is given that J Company purchases its interest in Jo Comp...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Paul M. Fischer, William J. Tayler, Rita H. Cheng

11th edition

538480289, 978-0538480284