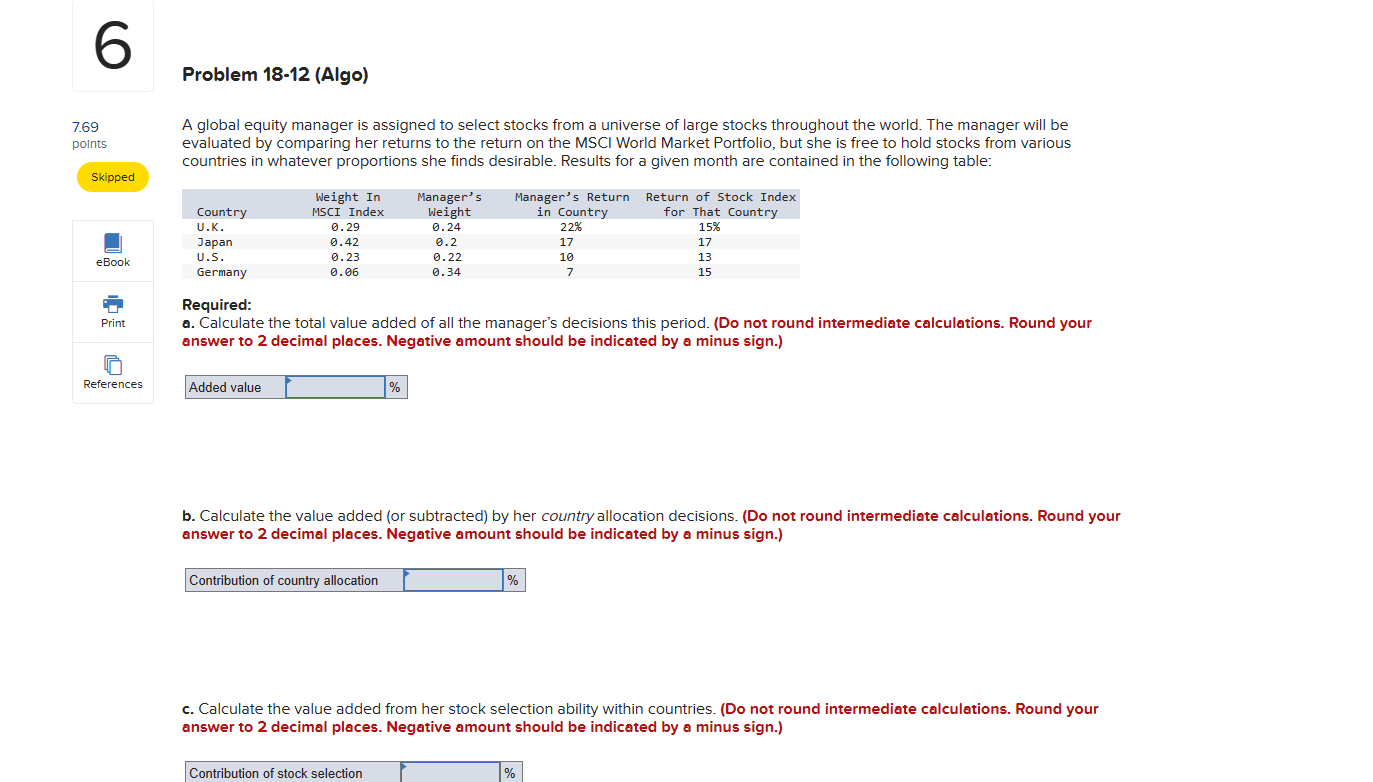

769 points Skipped O References Problem 18-12 (Alge) A global equity manager is assigned to select stocks from a universe of large stocks throughout the

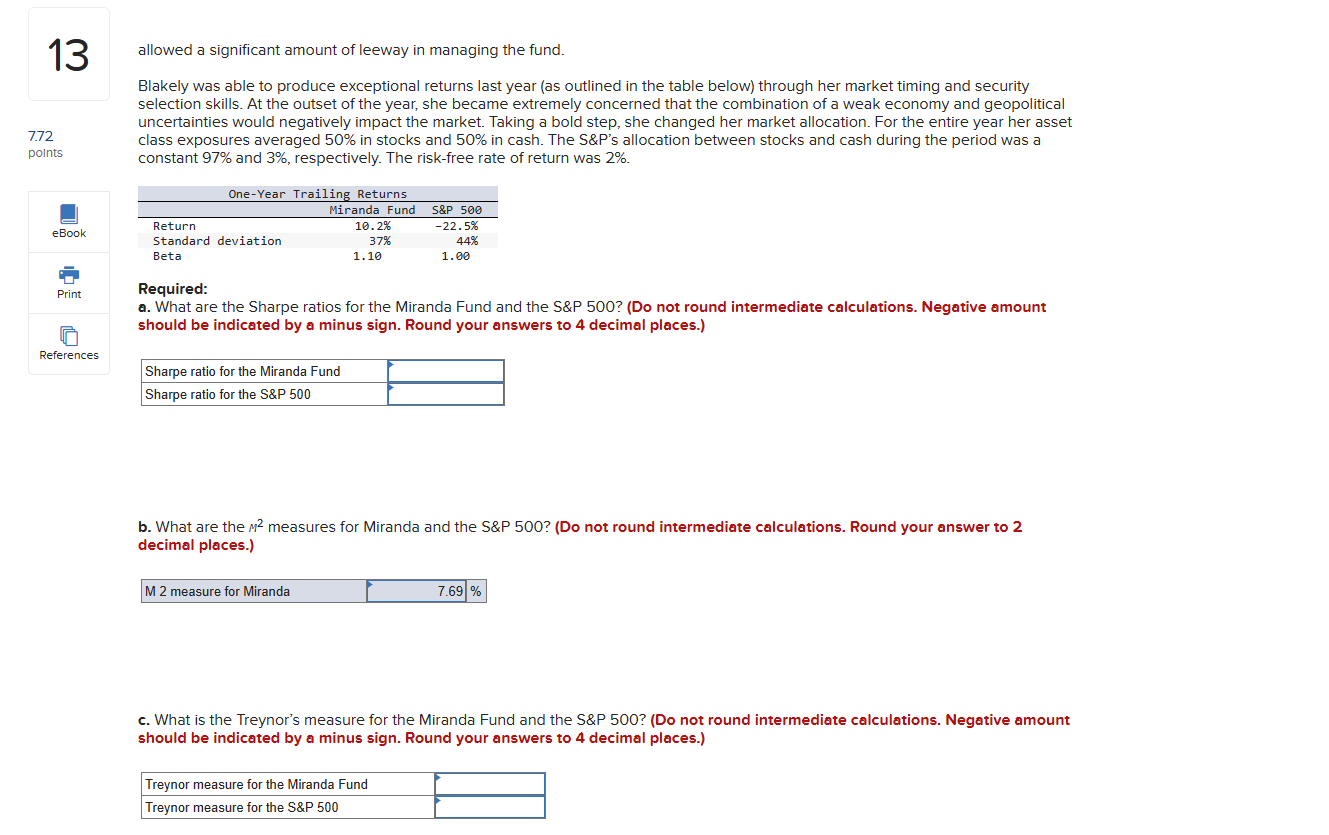

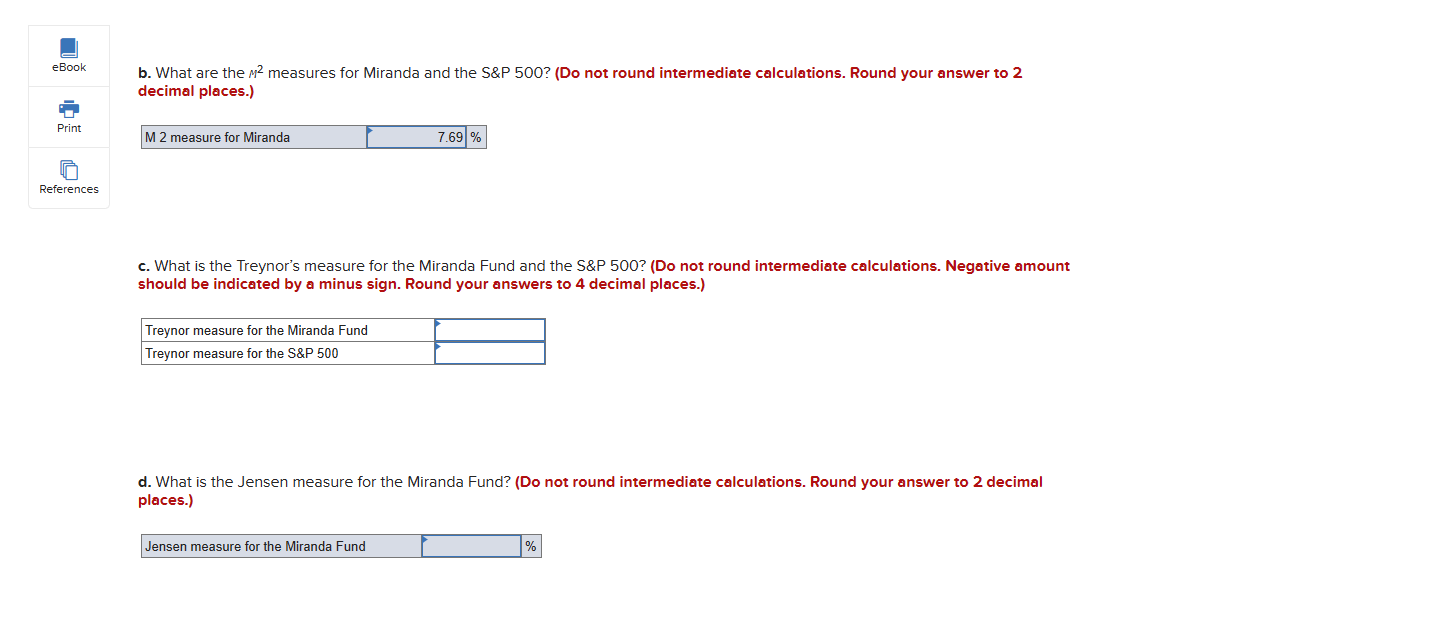

769 points Skipped O References Problem 18-12 (Alge) A global equity manager is assigned to select stocks from a universe of large stocks throughout the world. The manager will be evaluated by comparing her returns to the return on the MSCI World Market Portfalio, but she is free to hold stocks from various countries in whatever propertions she finds desirable. Results for a given month are contained in the following table: Weight In Manager's Manager's Return Return of Stock Index Country MSCI Index beight in Country for That Country U.K. @.29 @.24 22% 15% Japan 8.42 a.2 17 17 U.s. .23 8.22 1a 13 Germany 0.86 @.34 7 15 Required: a. Calculate the total value added of all the manager's decisions this period. (Do not round intermediate calculations. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Added value | |% b. Calculate the value added (or subtracted) by her country allocation decisions. (Do not round intermediate calculations. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Contribution of country allocation | % c. Calculate the value added from her stock selection ability within countries. (Do not round intermediate calculations. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Contribution of stock selection | % 13 772 points References allowed a significant amount of leeway in managing the fund. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak econemy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset class exposures averaged 50% in stocks and 50% in cash. The S&F's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2%. One-Year Trailing Returns Miranda Fund S&P 506 Return 12.2% -22.5% Standard deviation 37% 44% Beta 1.19 1l.e@ Required: a. What are the Sharpe ratios for the Miranda Fund and the S&P 5007 (Do not round intermediate calculations. Negative amount should be indicated by a minus sign. Round your answers to 4 decimal places.) Sharpe ratio for the Miranda Fund Sharpe ratio for the S&P 500 b. What are the n? measures for Miranda and the S&P 5007 (Do not round intermediate calculations. Round your answer to 2 decimal places.) M 2 measure for Miranda % . What is the Treynor's measure for the Miranda Fund and the S&P 5007 (Do not round intermediate calculations. Negative amount should be indicated by a minus sign. Round your answers to 4 decimal places.) Treynor measure for the Miranda Fund Treynor measure for the S&P 500 Book b. What are the M2 measures for Miranda and the S&P 500? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Print M 2 measure for Miranda 7.69 % References c. What is the Treynor's measure for the Miranda Fund and the S&P 500? (Do not round intermediate calculations. Negative amount should be indicated by a minus sign. Round your answers to 4 decimal places.) Treynor measure for the Miranda Fund Treynor measure for the S&P 500 d. What is the Jensen measure for the Miranda Fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Jensen measure for the Miranda Fund %

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance