Answered step by step

Verified Expert Solution

Question

1 Approved Answer

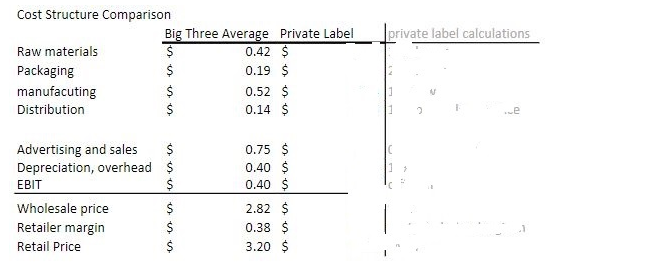

$ 0.52 $ Distribution 0.14 $ Cost Structure Comparison Raw materials Packaging manufacuting Big Three Average Private Label private label calculations $ SS ess

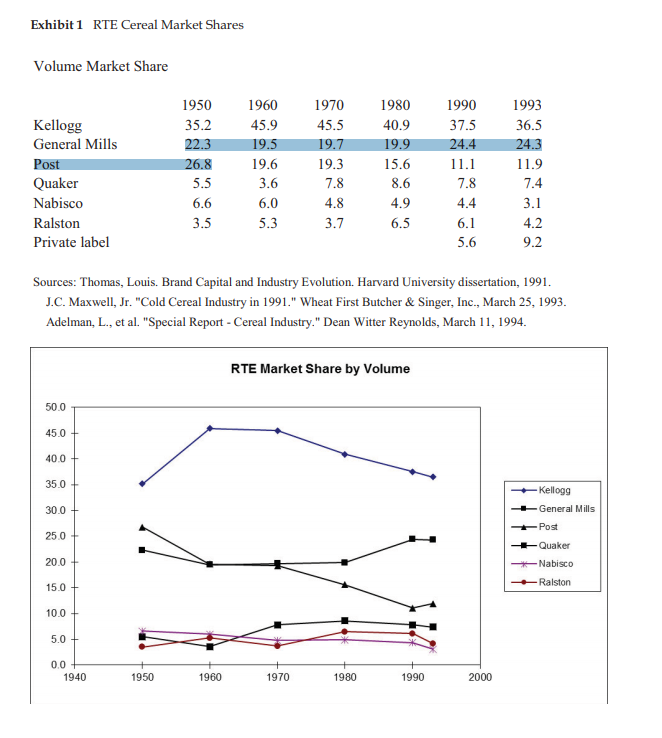

$ 0.52 $ Distribution 0.14 $ Cost Structure Comparison Raw materials Packaging manufacuting Big Three Average Private Label private label calculations $ SS ess 0.42 $ 0.19 $ 1 2 e Advertising and sales Depreciation, overhead $ EBIT Wholesale price Retailer margin Retail Price ssssss $ 0.75 $ 0.40 $ $ 0.40 $ $ 2.82 $ $ 0.38 $ $ 3.20 $ The Ready-to-Eat Breakfast Cereal Industry in 1994 (A) 795-191 Purina spun off its cereal, baby food, cookie, and cracker businesses by forming Ralcorp Holdings, an entirely independent publicly traded company. Ralston Purina shareholders received stock in the new company, and Ralston Purina retained no ownership stake whatsoever. Cereals accounted for 61 percent of this new company's sales. In addition to its branded and private label cereals, Ralston had developed a large line of licensed cereals in the 1980s. These cereals were relatively short-lived brands tied to a movie or television show. Ralston was the leader in the production of these cereals, which constituted as much as one fourth of their sales volume in the late 1980s. While these brands were extremely popular in the late 1980s and early 1990s, their popularity soon subsided. In fact, Ralston discontinued all licensed cereals in 1993. One industry source declared, "The most extraordinary non-event of 1993 cereal marketing was that not a single character-endorsed brand was introduced. In the year of Jurassic Park, Aladdin, Beavis and Butthead, and Barney, no cereal company tied its new product to a movie, TV or toy personality."15 The Private Label Threat From 1991 to 1994, sales of private label cereal grew 50% to nearly $500 million, or 9.2% of all cereal sales by volume. 16 Private labels' share of the RTE cereal industry was projected to pass 15% by 2000. For grocery products as a whole, private label products accounted for 19% of unit sales and were anticipated to grow to 30% by 2000.17 Despite the inroads made by private label cereals in the 1990s, not everyone was convinced that they presented a serious threat to the profitability of the branded manufacturers. A General Mills spokesperson said, "As the price of [RTE] cereals creeps up over time, I would think there would be opportunity for those companies in certain areas. But I don't think we would see them as a threat to any of our particular brands."18 Low price was the primary appeal of private label cereals. Private label cereals averaged $1.90 per pound at retail, 40% less than the Big Three average of about $3.20 per pound. Private labels did little advertising and made few attempts to differentiate their products in other ways. What little advertising they did undertake was devoted to raising awareness of their price advantage relative to branded cereals. Private label manufacturer Malt-O-Meal, for example, ran magazine ads showing a $2.03 bag of Malt-O-Meal's Sugar Puffs next to a $3.16 box of Sugar Crisp. The caption read: "You may not be able to tell the difference in your bowl, but we're sure you'll be able to tell the difference at the cash register."19 Private label cereals offered lower prices to the consumer, but were also perceived to offer better margins to the retailer, which contributed to a willingness of grocers to promote private labels enthusiastically. Private labels typically offered grocers 15% margins, compared to 12% margins for branded cereals. "Private label offers a good markup for us and savings for the consumer," said one grocer. "It doesn't take a genius to tell which products to put the signs next to."20 However, one trade journal argued that "many retailers may not understand the fully burdened cost of private label. That is, how the costs of warehousing, merchandising, shrinkage and other issues affect private label profitability, compared with national brands." Industry analyst Bob McCann added, "I'm not entirely sure that what seems obvious is the right answer."21 The high prices and ubiquitous coupons of branded cereals were blamed by many for the market share gains of private labels. One industry observer said, "coupons have been a major eroding factor. Without them, shoppers feel like they are overpaying. Private label is an alternative if there is no coupon and no sales price."22 The heavy use of coupons had more generally diminished brand loyalty by encouraging price-sensitive brand-switching. Brand loyalty was seen to have been further eroded by failed extensions of popular brands. One industry consultant argued that, "these brand extensions come out, and if they die, it tends to diminish the idea that these products are superior."23 Production and marketing of private label cereals changed dramatically in the early 1990s. For years private label suffered from poor quality and limited product variety. Black and white label generic brands found only short-lived success in the 1980s, and private label manufacturers discovered that even value-conscious consumers demanded a level of quality near that of a branded product. Increases in technological competence among private label manufacturers led to private label cereals that rivaled the branded products for quality. Still, the manufacturing costs per pound for a private label could be as much as 10-20% lower than for a Big Three firm because of their focus on simpler cereals with less labor intensive processes and fewer expensive fruits and nuts. Some private labels did away with the cereal box and sold cereals in clear plastic bags, reducing packaging costs by up to 25%. Private labels relied on wholesalers and third-party distributors--which received approximately a 10% margin on the wholesale price paid by the retailer--for distribution of their products. These distributors did little more than deliver the product to stores and did not provide the on-site presence of the Big Three's large national salesforces. The Big Three had systematically and publicly refused to produce private label cereals. In fact, some Kellogg packages boasted, "We don't make cereals for anyone else." While Ralston had at one point virtually monopolized the private label cereal market, by 1994 its market share of the private label cereals was estimated to have fallen to about 50%. After Ralston, the most established producer of private label cereals was Malt-O-Meal, which had been in the business since the 1970s. Other, more recent entrants into the private label RTE business included Grist Mill (the nation's leading supplier of private label granola bars and pie crusts) and McKee Baking (the nation's leading snack cake manufacturer with its Little Debbie brand). Malt-O-Meal Malt-O-Meal, which had been producing hot cereal since 1919, began producing RTE breakfast cereal in the early 1970s. By 1989, its 14 varieties of cereal accounted for approximately 2% of the total RTE market. Its cereal was sold both through private label arrangements with major supermarket chains, including Kroger and Safeway, and under the Malt-O-Meal name. 24 Cereal marketed under the Malt-O-Meal name was sold in economical 15-ounce clear plastic bags. From 1989 to 1994, sales grew from $94 million to $210 million, about three quarters of which derived from RTE cereals. This growth Exhibit 1 RTE Cereal Market Shares Volume Market Share 1950 1960 1970 1980 1990 1993 Kellogg 35.2 45.9 45.5 40.9 37.5 36.5 General Mills 22.3 19.5 19.7 19.9 24.4 24.3 Post 26.8 19.6 19.3 15.6 11.1 11.9 Quaker 5.5 3.6 7.8 8.6 7.8 7.4 Nabisco 6.6 6.0 4.8 4.9 4.4 3.1 Ralston 3.5 5.3 3.7 6.5 6.1 4.2 Private label 5.6 9.2 Sources: Thomas, Louis. Brand Capital and Industry Evolution. Harvard University dissertation, 1991. J.C. Maxwell, Jr. "Cold Cereal Industry in 1991." Wheat First Butcher & Singer, Inc., March 25, 1993. Adelman, L., et al. "Special Report - Cereal Industry." Dean Witter Reynolds, March 11, 1994. 50.0 45.0 40.0 RTE Market Share by Volume 35.0 30.0 25.0 20.0 15.0 10.0 5.0 0.0 1940 1950 1960 1970 1980 1990 2000 -Kellogg -General Mills -Post Quaker Nabisco Ralston

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture capital and the finance of innovation

Authors: Andrew Metrick

2nd Edition

9781118137888, 470454709, 1118137884, 978-0470454701