Answered step by step

Verified Expert Solution

Question

1 Approved Answer

1. 2. 3. 4. Suppose that call options on ExxonMobil stock with time to expiration 3 months and strike price $90 are selling at an

1.

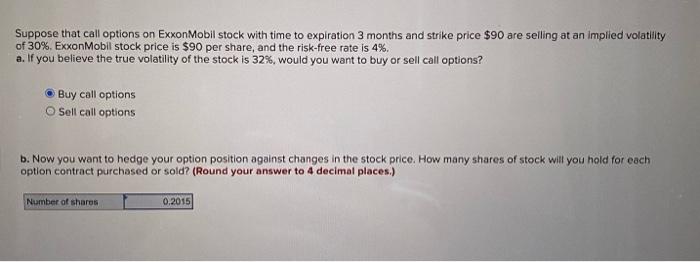

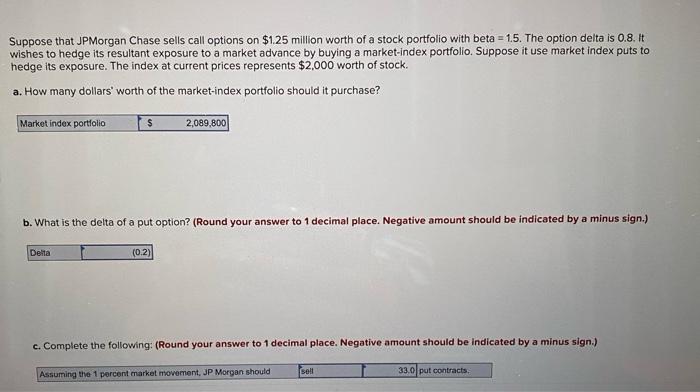

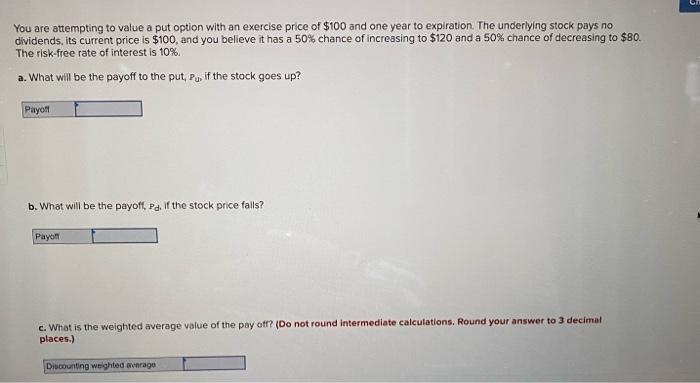

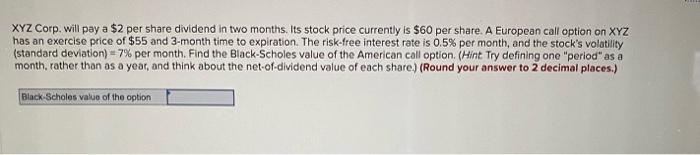

Suppose that call options on ExxonMobil stock with time to expiration 3 months and strike price $90 are selling at an implied volatility of 30%. ExxonMobil stock price is $90 per share, and the risk-free rate is 4%. a. If you believe the true volatility of the stock is 32%, would you want to buy or sell call options? Buy call options Sell call options b. Now you want to hedge your option position against changes in the stock price. How many shares of stock will you hold for each option contract purchased or sold? (Round your answer to 4 decimal places.) Suppose that JPMorgan Chase sells call options on $1.25 million worth of a stock portfolio with beta =1.5. The option delta is 0.8. It wishes to hedge its resultant exposure to a market advance by buying a market-index portfolio. Suppose it use market index puts to hedge its exposure. The index at current prices represents $2,000 worth of stock. a. How many dollars' worth of the market-index portfolio should it purchase? b. What is the delta of a put option? (Round your answer to 1 decimal place. Negative amount should be indicated by a minus sign.) c. Complete the following: (Round your answer to 1 decimal place. Negative amount should be indicated by a minus sign.) You are attempting to value a put option with an exercise price of $100 and one year to expiration. The underlying stock pays no dividends, its current price is $100, and you believe it has a 50% chance of increasing to $120 and a 50% chance of decreasing to $80. The risk-free rate of interest is 10%. a. What will be the payoff to the put, Pu if the stock goes up? b. What will be the payoff, Pd, if the stock price falls? c. What is the weighted average value of the pay otf? (Do not round intermediate calculations. Round your answer to 3 decimal places.) XYZ Corp. Will pay a $2 per share dividend in two months. Its stock price currently is $60 per share. A European call option on XYZ has an exercise price of $55 and 3-month time to expiration. The risk-free interest rate is 0.5% per month, and the stock's volatility (standard deviation) =7% per month. Find the Black-Scholes value of the American call option. (Hint Try defining one "period" as a month, rather than as a year, and think about the net-of-dividend value of each share) (Round your answer to 2 decimal piaces.) 2.

3.

4.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Acquisition Finance

Authors: Tom Speechley

2nd Edition

1780436599, 978-1780436593