Answered step by step

Verified Expert Solution

Question

1 Approved Answer

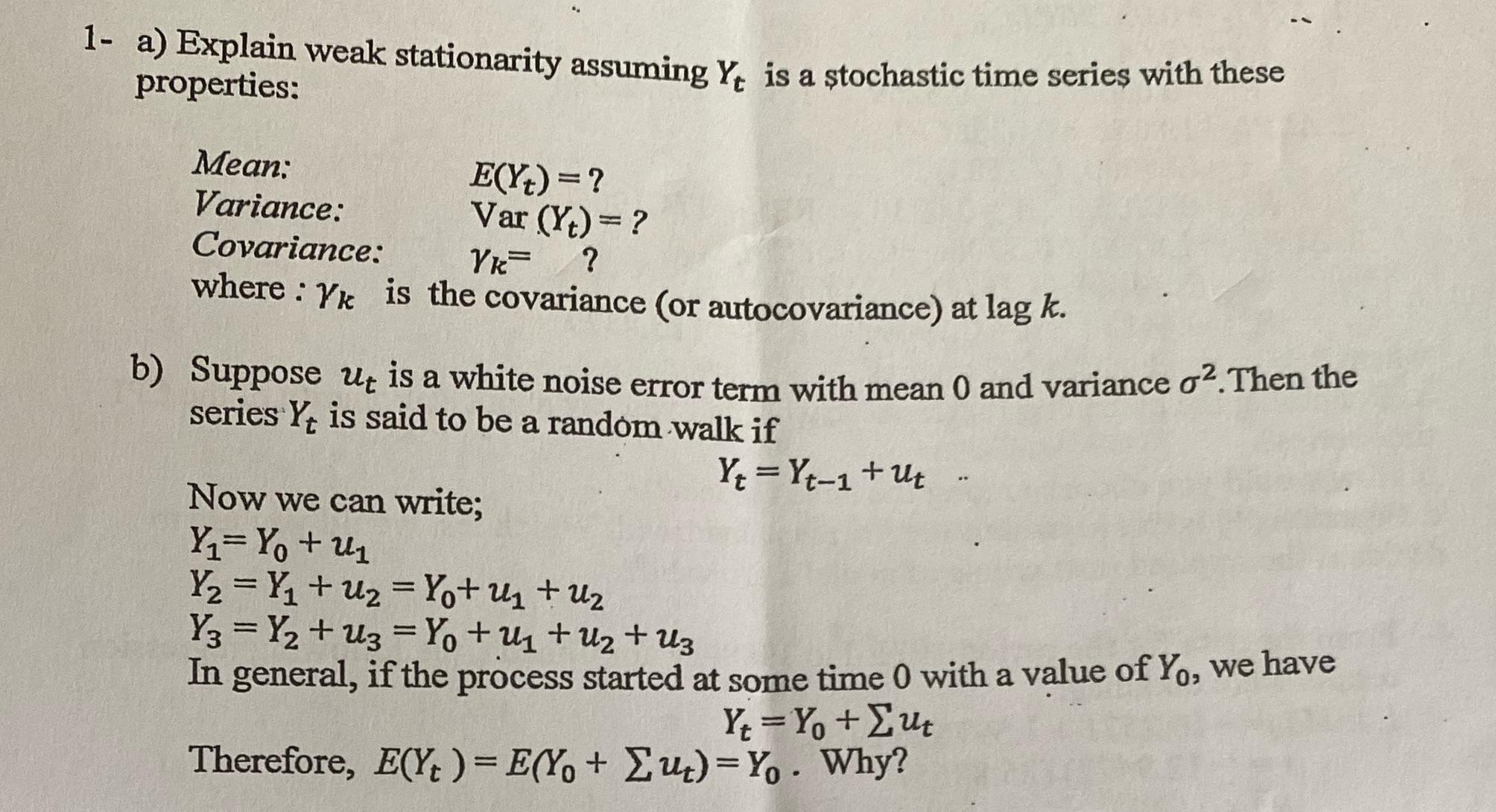

1- a) Explain weak stationarity assuming Yt is a stochastic time series with these properties: Mean: Variance: Covariance: E(Y) = ? Var (Yt) =

1- a) Explain weak stationarity assuming Yt is a stochastic time series with these properties: Mean: Variance: Covariance: E(Y) = ? Var (Yt) = ? Yk= ? where Yk is the covariance (or autocovariance) at lag k. b) Suppose ut is a white noise error term with mean 0 and variance o2. Then the series Yt is said to be a random walk if Yt=Yt-1+ut Now we can write; Y=Y + U Y=Y+U = Yo+U+U Y3 = Y + U3 = Y + U+U+Uz 1 In general, if the process started at some time 0 with a value of Yo, we have Yt=Yo + ut Therefore, E(Yt) = E(Yo + Zut) = Yo . Why?

Step by Step Solution

★★★★★

3.39 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

a Weak stationarity implies 1 The mean EY is constant over time It does not depend on t 2 T...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forecasting for Economics and Business

Authors: Gloria Gonzalez Rivera

1st edition

131474936, 978-1315510415, 1315510413, 978-0131474932