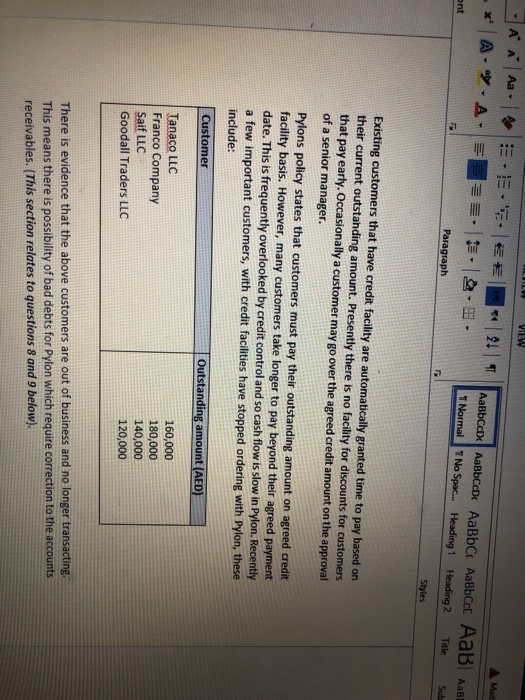

1 * *, *'A Font 21 ABCD AaBbcede AaBbc AaBbcc AaB AaBbce .A. . . . . 1 Normal 1 No Spac... Heading 1 Heading 2 Title Subtitle Paragraph Styles Brief company background Pylon LLC has been in business since 1998 and has grown rapidly over the middle east. The company is a distributor of electronic parts and equipment to the IT industry in the GCC region. Pylon has some strong internal controls policies and procedures over its business environment both internally and externally. However, the business environment is semi- computerized. Business transaction - Processing customer order Orders may arrive by email, telephone, or from a field representative who visited the customer. These orders are processed, and orders are shipped to the customers. The customer order processing is computerized, and all bar-codes are selected from a drop-down menu in the order processing procedure. Prices for orders are automatically shown against each part selected. Business transaction - Granting credit The company has many customers both old and new. Some new customers have been in business for many years, however, have recently started to trade with Pylon. Other customers have been trading with Pylon for 4-7 years. Most existing customers are given credit facilities and payment period is between 1 - 3 months, depending on the background of the company and its trading history. Credit facility provided to new customers is subject to vetting (checking) of the customer according to the company policy. Credit amounts range between AED 50,000 to AED 1 million. There is a hierarchy of credit approvers within Pylon who approve credit facilities for accepted customers ranging from senior managers to the Board of Directors. Policy requires that new customers applying for credit must: Business transaction - Granting credit The company has many customers both old and new. Some new customers have been in business for many years, however, have recently started to trade with Pylon. Other customers have been trading with Pylon for 4-7 years. Most existing customers are given credit facilities and payment period is between 1-3 months, depending on the background of the company and its trading history. Credit facility provided to new customers is subject to vetting (checking) of the customer according to the company policy. Credit amounts range between AED 50,000 to AED 1 million There is a hierarchy of credit approvers within Pylon who approve credit facilities for accepted customers ranging from senior managers to the Board of Directors. Policy requires that new customers applying for credit must: 1. Have been in business for at least past seven years with audit accounts as evidence 2. They should provide at least last 5 years bank statements to prove their existence 3. New customers must provide 5 references from existing suppliers with whom they have been trading 4. Existing suppliers must have traded with the new customers for at least 1 year 5. New customers must provide their business cash flow forecast for next three years if their credit application is for over AED 100,000 The due diligence for credit facility is carried out by a third-party company on behalf of Pylon LLC. SH (UNITED STATES) LILY VIEW AAA. -*' A .A. EE . 18. 2 . T Normal 1 No Spac... Heading 1 Heading 2 Title Sut ont Paragraph Styles Existing customers that have credit facility are automatically granted time to pay based on their current outstanding amount. Presently there is no facility for discounts for customers that pay early. Occasionally a customer may go over the agreed credit amount on the approval of a senior manager. Pylons policy states that customers must pay their outstanding amount on agreed credit facility basis. However, many customers take longer to pay beyond their agreed payment date. This is frequently overlooked by credit control and so cash flow is slow in Pylon. Recently a few important customers, with credit facilities have stopped ordering with Pylon, these include: Customer Outstanding amount (AED) Tanaco LLC Franco Company Saif LLC Goodall Traders LLC 160,000 180,000 140,000 120,000 There is evidence that the above customers are out of business and no longer transacting. This means there is possibility of bad debts for Pylon which require correction to the accounts receivables. (This section relates to questions 8 and 9 below). - HD Webcam ACC 3113_MID TERM GROUP WORK -20%.docx - Word MAILINGS REVIEW VIEW REFERENCES A = == . 9.3. AaBbCcDc AaBbCcDc AaBbcc AaBbcc 1 Normal 1 No Spac... Heading 1 Heading 2 Paragraph Styles Cash Transaction Cycle - Processing cash receipts The sales cycle is complete upon receipt of cash from the customers. Once cash is received from customers the relevant records are updated and accounts receivable is also updated. Some customers send cash or deposit cash in Pylons bank account directly. The company's normal practice is to demand cheque payment which means customers cannot pay by other means such as bank transfers and credit cards which is a factor in late customer payments. The cheques are received by post and banked the next day by the cashier who handles all cash receipts and payments. He makes a list of all cheques and hands then over to the credit clerk who then updates customer accounts. The cashier attends to some cash paying customers personally at their business premises to collect the cash. ma No Spac... Heading 1 Heading 2 Paragraph Styles INTERNAL CONTROL RELATED QUESTIONS 3. Discuss the robustness of the credit granting procedure in Pylon identifying any strengths and weaknesses that exist (7 marks) Identify and discuss the audit evidence for sales in Pylon (6 marks) 5. Identify and explain the internal controls that currently exist in Pylon (6 marks) Identify the weaknesses in internal controls that currently exist in the company (7 marks) Identify and explain how internal control system could be improved in Pylon (7 marks) 8. Identify and explain how you would apply a substantive test to Accounts Receivables (7 marks) 19. Identity and explain how you would apply a Test of control to Accounts Receivables (7 marks) 10. Discuss if any matters are of serious or material that could impact upon audit opinion (7 marks) 11. Identity and explain any issues of concern in the cash transaction cycle and how this can be improved (6 Marks) 1 * *, *'A Font 21 ABCD AaBbcede AaBbc AaBbcc AaB AaBbce .A. . . . . 1 Normal 1 No Spac... Heading 1 Heading 2 Title Subtitle Paragraph Styles Brief company background Pylon LLC has been in business since 1998 and has grown rapidly over the middle east. The company is a distributor of electronic parts and equipment to the IT industry in the GCC region. Pylon has some strong internal controls policies and procedures over its business environment both internally and externally. However, the business environment is semi- computerized. Business transaction - Processing customer order Orders may arrive by email, telephone, or from a field representative who visited the customer. These orders are processed, and orders are shipped to the customers. The customer order processing is computerized, and all bar-codes are selected from a drop-down menu in the order processing procedure. Prices for orders are automatically shown against each part selected. Business transaction - Granting credit The company has many customers both old and new. Some new customers have been in business for many years, however, have recently started to trade with Pylon. Other customers have been trading with Pylon for 4-7 years. Most existing customers are given credit facilities and payment period is between 1 - 3 months, depending on the background of the company and its trading history. Credit facility provided to new customers is subject to vetting (checking) of the customer according to the company policy. Credit amounts range between AED 50,000 to AED 1 million. There is a hierarchy of credit approvers within Pylon who approve credit facilities for accepted customers ranging from senior managers to the Board of Directors. Policy requires that new customers applying for credit must: Business transaction - Granting credit The company has many customers both old and new. Some new customers have been in business for many years, however, have recently started to trade with Pylon. Other customers have been trading with Pylon for 4-7 years. Most existing customers are given credit facilities and payment period is between 1-3 months, depending on the background of the company and its trading history. Credit facility provided to new customers is subject to vetting (checking) of the customer according to the company policy. Credit amounts range between AED 50,000 to AED 1 million There is a hierarchy of credit approvers within Pylon who approve credit facilities for accepted customers ranging from senior managers to the Board of Directors. Policy requires that new customers applying for credit must: 1. Have been in business for at least past seven years with audit accounts as evidence 2. They should provide at least last 5 years bank statements to prove their existence 3. New customers must provide 5 references from existing suppliers with whom they have been trading 4. Existing suppliers must have traded with the new customers for at least 1 year 5. New customers must provide their business cash flow forecast for next three years if their credit application is for over AED 100,000 The due diligence for credit facility is carried out by a third-party company on behalf of Pylon LLC. SH (UNITED STATES) LILY VIEW AAA. -*' A .A. EE . 18. 2 . T Normal 1 No Spac... Heading 1 Heading 2 Title Sut ont Paragraph Styles Existing customers that have credit facility are automatically granted time to pay based on their current outstanding amount. Presently there is no facility for discounts for customers that pay early. Occasionally a customer may go over the agreed credit amount on the approval of a senior manager. Pylons policy states that customers must pay their outstanding amount on agreed credit facility basis. However, many customers take longer to pay beyond their agreed payment date. This is frequently overlooked by credit control and so cash flow is slow in Pylon. Recently a few important customers, with credit facilities have stopped ordering with Pylon, these include: Customer Outstanding amount (AED) Tanaco LLC Franco Company Saif LLC Goodall Traders LLC 160,000 180,000 140,000 120,000 There is evidence that the above customers are out of business and no longer transacting. This means there is possibility of bad debts for Pylon which require correction to the accounts receivables. (This section relates to questions 8 and 9 below). - HD Webcam ACC 3113_MID TERM GROUP WORK -20%.docx - Word MAILINGS REVIEW VIEW REFERENCES A = == . 9.3. AaBbCcDc AaBbCcDc AaBbcc AaBbcc 1 Normal 1 No Spac... Heading 1 Heading 2 Paragraph Styles Cash Transaction Cycle - Processing cash receipts The sales cycle is complete upon receipt of cash from the customers. Once cash is received from customers the relevant records are updated and accounts receivable is also updated. Some customers send cash or deposit cash in Pylons bank account directly. The company's normal practice is to demand cheque payment which means customers cannot pay by other means such as bank transfers and credit cards which is a factor in late customer payments. The cheques are received by post and banked the next day by the cashier who handles all cash receipts and payments. He makes a list of all cheques and hands then over to the credit clerk who then updates customer accounts. The cashier attends to some cash paying customers personally at their business premises to collect the cash. ma No Spac... Heading 1 Heading 2 Paragraph Styles INTERNAL CONTROL RELATED QUESTIONS 3. Discuss the robustness of the credit granting procedure in Pylon identifying any strengths and weaknesses that exist (7 marks) Identify and discuss the audit evidence for sales in Pylon (6 marks) 5. Identify and explain the internal controls that currently exist in Pylon (6 marks) Identify the weaknesses in internal controls that currently exist in the company (7 marks) Identify and explain how internal control system could be improved in Pylon (7 marks) 8. Identify and explain how you would apply a substantive test to Accounts Receivables (7 marks) 19. Identity and explain how you would apply a Test of control to Accounts Receivables (7 marks) 10. Discuss if any matters are of serious or material that could impact upon audit opinion (7 marks) 11. Identity and explain any issues of concern in the cash transaction cycle and how this can be improved (6 Marks)