Answered step by step

Verified Expert Solution

Question

1 Approved Answer

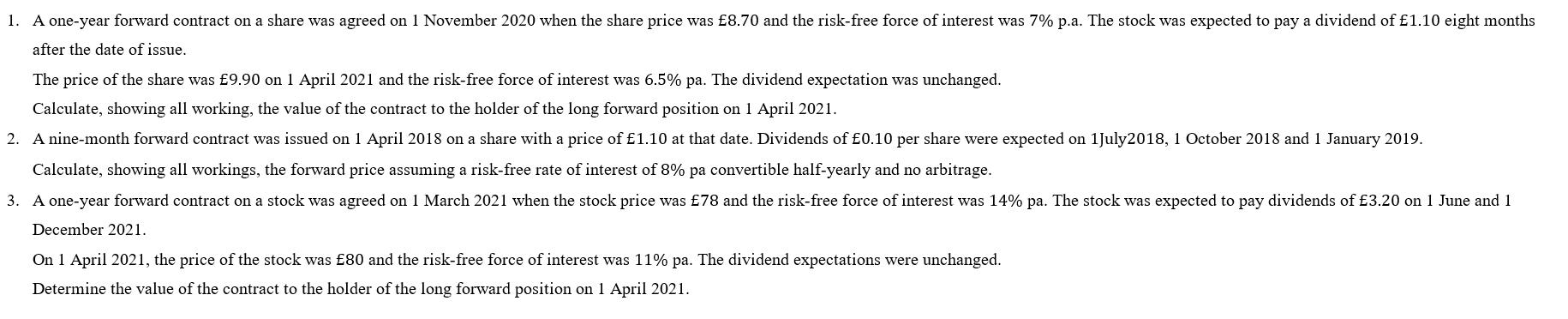

1. A one-year forward contract on a share was agreed on 1 November 2020 when the share price was 8.70 and the risk-free force

1. A one-year forward contract on a share was agreed on 1 November 2020 when the share price was 8.70 and the risk-free force of interest was 7% p.a. The stock was expected to pay a dividend of 1.10 eight months after the date of issue. The price of the share was 9.90 on 1 April 2021 and the risk-free force of interest was 6.5% pa. The dividend expectation was unchanged. Calculate, showing all working, the value of the contract to the holder of the long forward position on 1 April 2021. 2. A nine-month forward contract was issued on 1 April 2018 on a share with a price of 1.10 at that date. Dividends of 0.10 per share were expected on 1July 2018, 1 October 2018 and 1 January 2019. Calculate, showing all workings, the forward price assuming a risk-free rate of interest of 8% pa convertible half-yearly and no arbitrage. 3. A one-year forward contract on a stock was agreed on 1 March 2021 when the stock price was 78 and the risk-free force of interest was 14% pa. The stock was expected to pay dividends of 3.20 on 1 June and 1 December 2021. On 1 April 2021, the price of the stock was 80 and the risk-free force of interest was 11% pa. The dividend expectations were unchanged. Determine the value of the contract to the holder of the long forward position on 1 April 2021.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Business Finance

Authors: David K. Eiteman, Arthur I. Stonehill, Michael H. Moffett

16th Edition

013749601X, 978-0137496013