1)

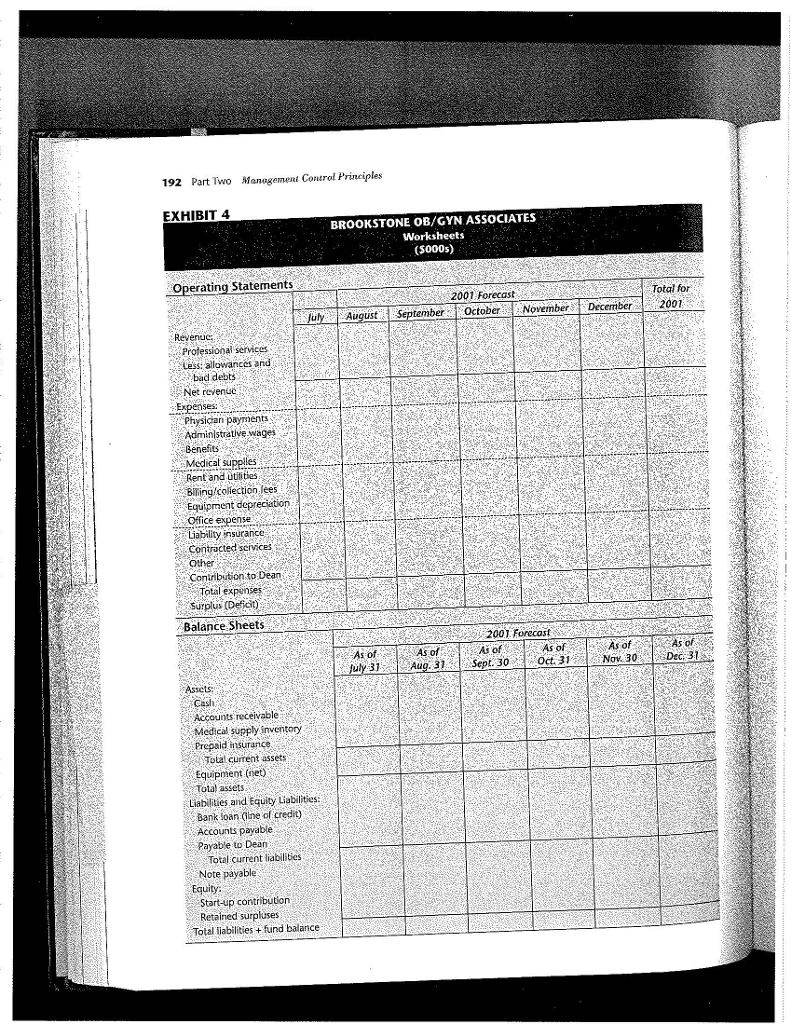

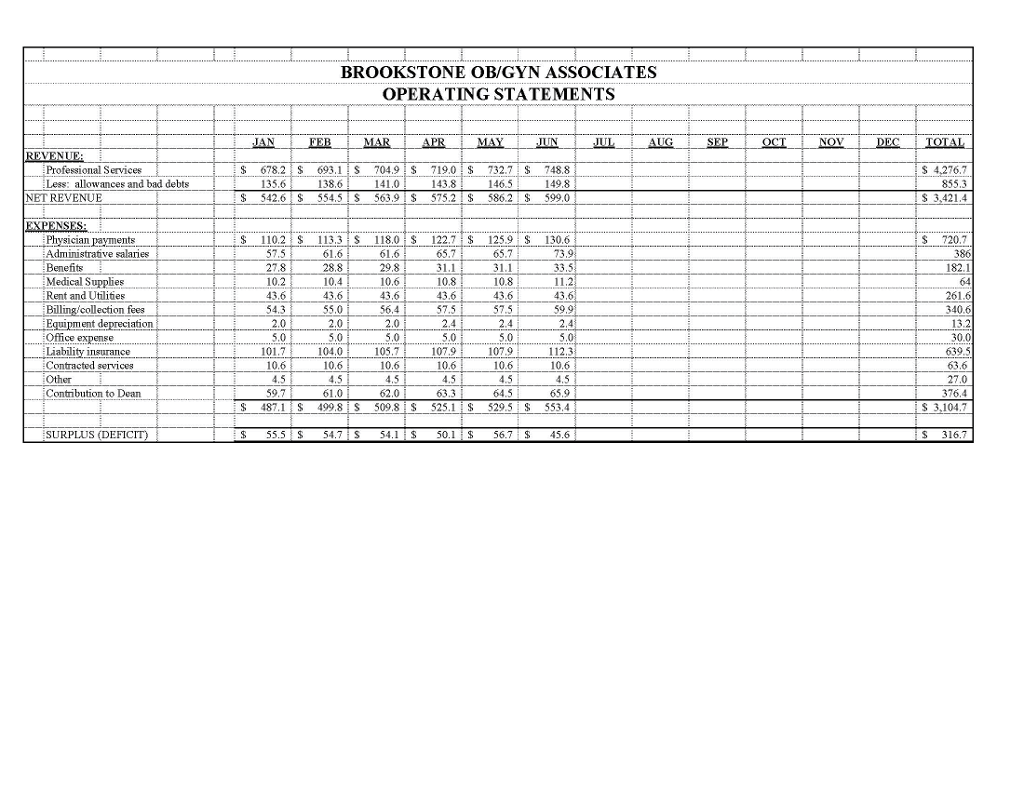

a). Prepare a Projected Operating Statement on the accrual basis for July December using the assumptions provided in Exhibit 3.

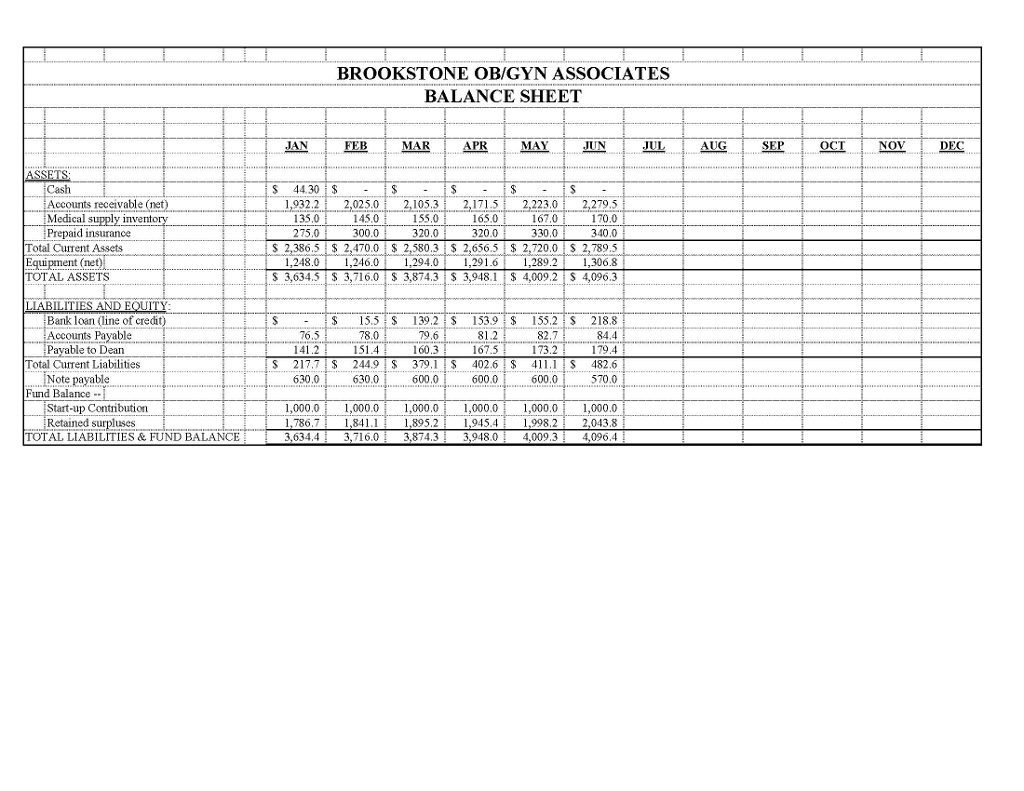

b). Prepare a Projected Balance Sheet on the accrual basis for July December using the assumptions provided in Exhibit 3 and additional information provided it the case.

Formulas for Pro Forma Balance Sheet for July - December

Accounts Receivable: Beginning Balance + Current Month Net Sales Revenue

Collections on Accounts Receivable (5 month lag)

Equipment: Beginning Balance + Purchases Depreciation Dean Payable: Beginning Balance + 11% Net Revenue 11% Collections Retained Earnings: Beginning Balance +/- Surplus/Deficit

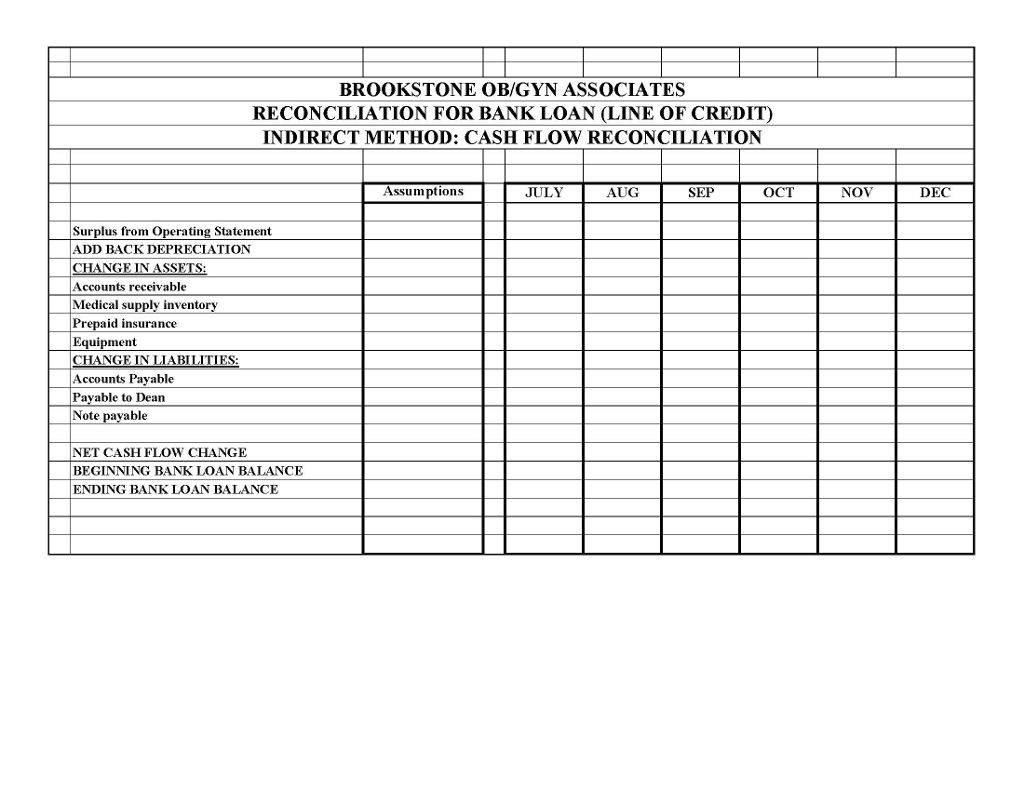

c). Prepare a Projected Bank Loan Reconciliation for July December using the assumptions provided in Exhibit 3 and additional information (including the Operating Statement and Balance Sheet) provided in the case.

Briefly describe the decline in available cash position.

Briefly describe other strategic options that are available.

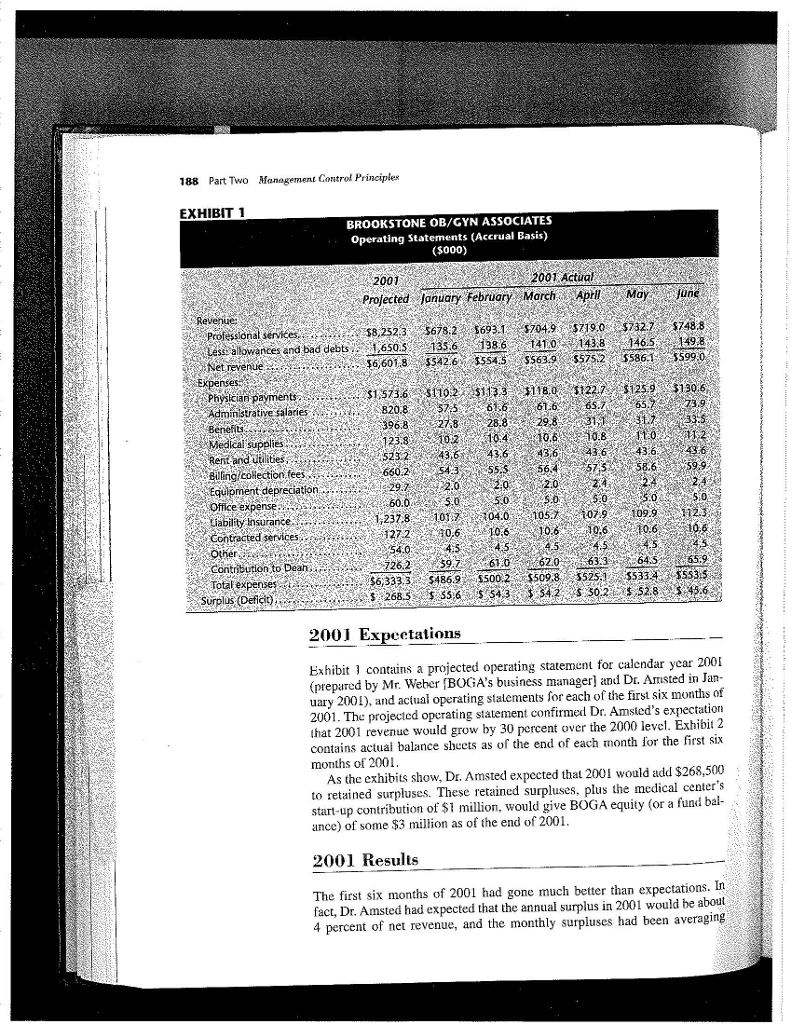

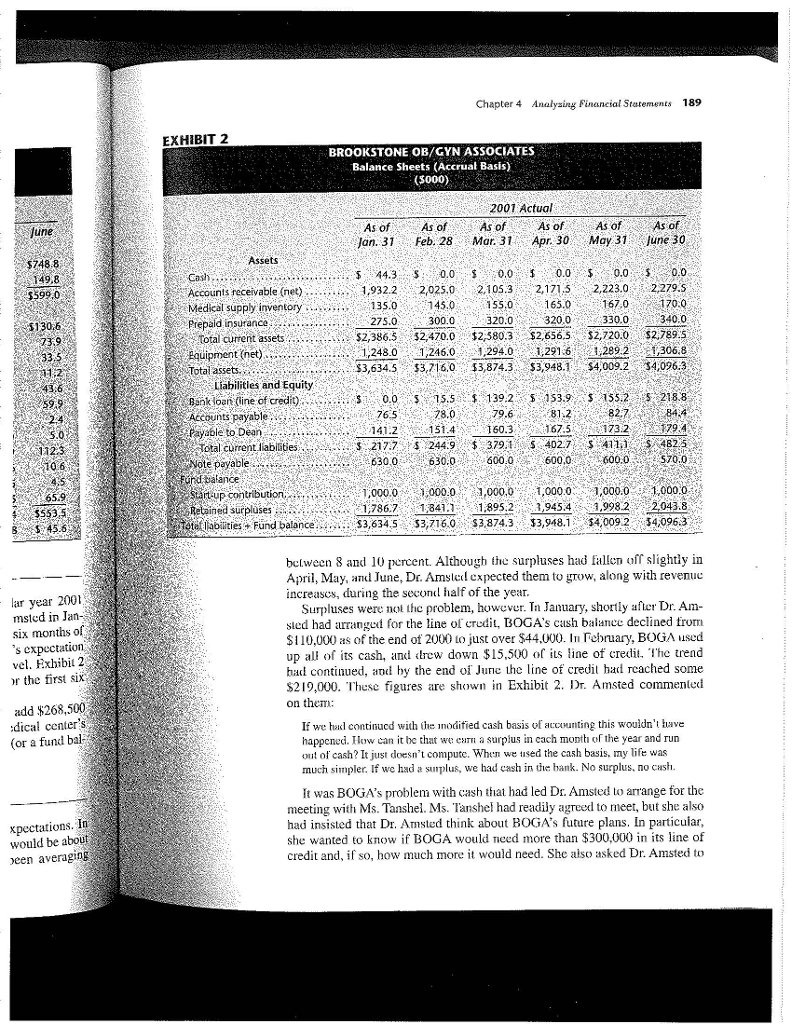

Chapter 4 Analysing Financial Statements 187 Case 4-3 Brookstone Ob-Gyn Associates* 7.00. ch as rown pro rnher 0, and onthly the meals In mid-July 2001, Dr. Mark Amsted, chair of the department of obstetrics and gynecology at Brookstone Medical School, chief of Ob-Gyn at Brookstone Mcdical Center, and president of Brookstone Ob-Gyn Associales (BOGA), was concerned about his upcoming meeting with the Iarris National Bank He planned to present a request for a increase in BOGA's line of credit. As had happened in the past, the bank's approval o his rquest was critical to BOGA's conlinucd operations. Although the dean of the medical school had approved his request to approach the bank, Dr. Amsted was uncertain ahout the bank's reaction cCall In conjunction with Dr. Amsted's January request for a$300,000 line of credit, the hank had asked hi to prepare some projections for the 2001 oper- ating year. IIe had done this, indicating that he expected 200 revenue to be 30 percent greater than 2000 revenue After switching to an accrual system of accounling, Dr. Arnsted had been pieased to learn that 2000 had been a prof table year for the group. His projections indicated that 2001 also would be profitable. t until month Ic sent ed the Problems e be as ms you Despite the growth in revenues ad the group's profitability, BOGA's cash flow was once again becoming an issuc. Indecd, as he began to prepare for the meeting with the bank, Dr. Amsted realized that he faced to problums related Lo BOGA's cash flows. He comnente: month, ormula In January, I establisel a $300,000 linc of eredit with thc Harris Bank. We expectei to have somc cash flow difficulties, and ! thought this would help us copc with them until our cash caught up whor pritability. Now I'm not surc 5300,( is enough! vember tements atching vhen the There's related problem, too. Until 2000, we kept our tinancial records un what thc accountants calied a modified cash basis. Thaf was ptetty simpic. Revenues were reconded when we received a cash payment from a patient or third- parly payer. Expenses were recorded when the cash was paid out. The nly exception was plant and equipment purchases, where the accountants said we needed to use depreciation instead of cash as theexpense. When I applied the Harris Bank for the line of credit, Ms. Tanshel [the bank's loan officer] told me that a modified cash basis was not an acceptable way to present our financial statements. The bank required us to submit our statements on an accrual basis. According to our accountants, the most significant change needed to satisfy the bank's requirement was to record revenue when a patient received services, rather than when we actually received the related cash payment through ing nnecte This case was prepared by Professor David W. Young. Copyright O by David W. Young. Chapter 4 Analysing Financial Statements 187 Case 4-3 Brookstone Ob-Gyn Associates* 7.00. ch as rown pro rnher 0, and onthly the meals In mid-July 2001, Dr. Mark Amsted, chair of the department of obstetrics and gynecology at Brookstone Medical School, chief of Ob-Gyn at Brookstone Mcdical Center, and president of Brookstone Ob-Gyn Associales (BOGA), was concerned about his upcoming meeting with the Iarris National Bank He planned to present a request for a increase in BOGA's line of credit. As had happened in the past, the bank's approval o his rquest was critical to BOGA's conlinucd operations. Although the dean of the medical school had approved his request to approach the bank, Dr. Amsted was uncertain ahout the bank's reaction cCall In conjunction with Dr. Amsted's January request for a$300,000 line of credit, the hank had asked hi to prepare some projections for the 2001 oper- ating year. IIe had done this, indicating that he expected 200 revenue to be 30 percent greater than 2000 revenue After switching to an accrual system of accounling, Dr. Arnsted had been pieased to learn that 2000 had been a prof table year for the group. His projections indicated that 2001 also would be profitable. t until month Ic sent ed the Problems e be as ms you Despite the growth in revenues ad the group's profitability, BOGA's cash flow was once again becoming an issuc. Indecd, as he began to prepare for the meeting with the bank, Dr. Amsted realized that he faced to problums related Lo BOGA's cash flows. He comnente: month, ormula In January, I establisel a $300,000 linc of eredit with thc Harris Bank. We expectei to have somc cash flow difficulties, and ! thought this would help us copc with them until our cash caught up whor pritability. Now I'm not surc 5300,( is enough! vember tements atching vhen the There's related problem, too. Until 2000, we kept our tinancial records un what thc accountants calied a modified cash basis. Thaf was ptetty simpic. Revenues were reconded when we received a cash payment from a patient or third- parly payer. Expenses were recorded when the cash was paid out. The nly exception was plant and equipment purchases, where the accountants said we needed to use depreciation instead of cash as theexpense. When I applied the Harris Bank for the line of credit, Ms. Tanshel [the bank's loan officer] told me that a modified cash basis was not an acceptable way to present our financial statements. The bank required us to submit our statements on an accrual basis. According to our accountants, the most significant change needed to satisfy the bank's requirement was to record revenue when a patient received services, rather than when we actually received the related cash payment through ing nnecte This case was prepared by Professor David W. Young. Copyright O by David W. Young