Answered step by step

Verified Expert Solution

Question

1 Approved Answer

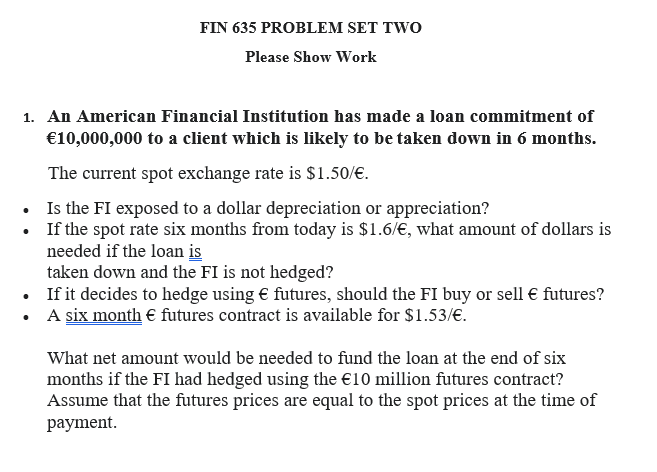

1. An American Financial Institution has made a loan commitment of 10,000,000 to a client which is likely to be taken down in 6 months.

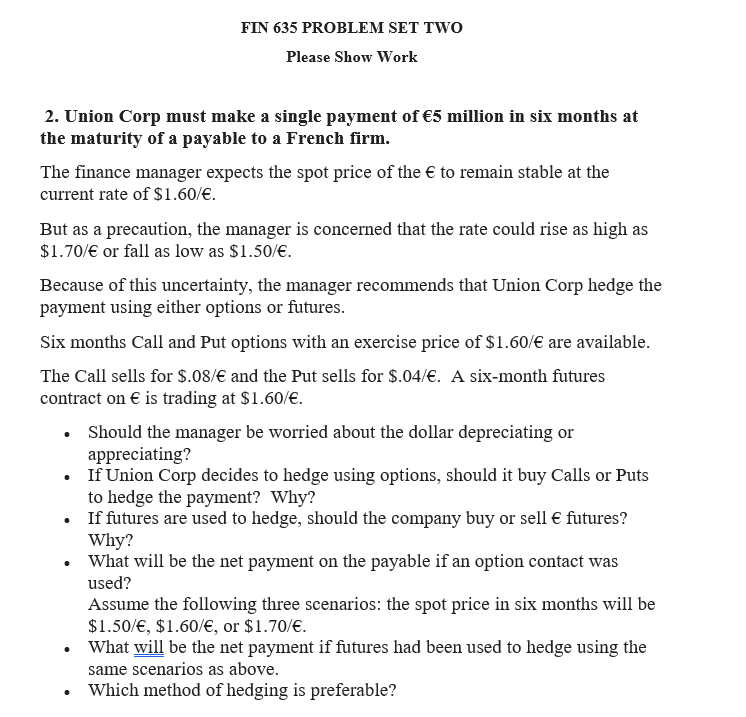

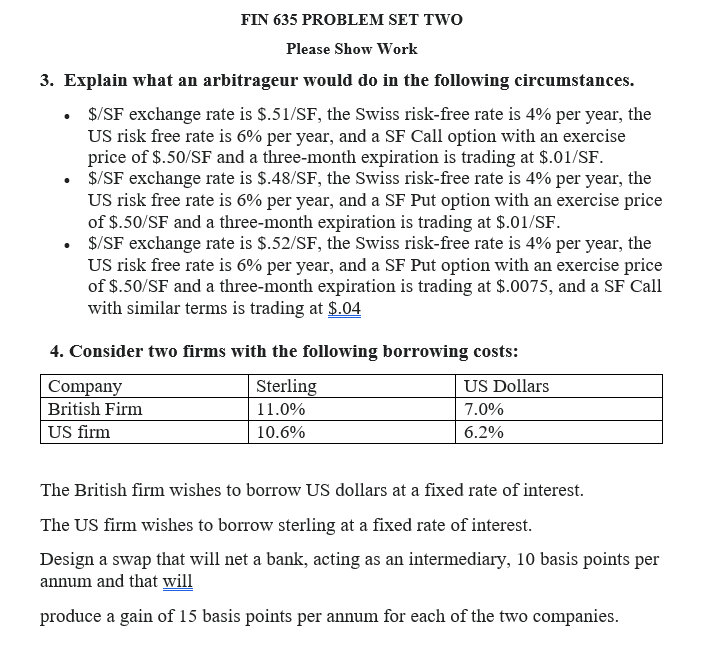

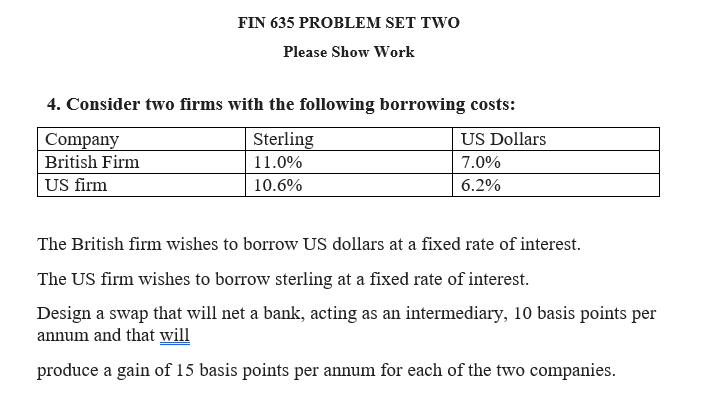

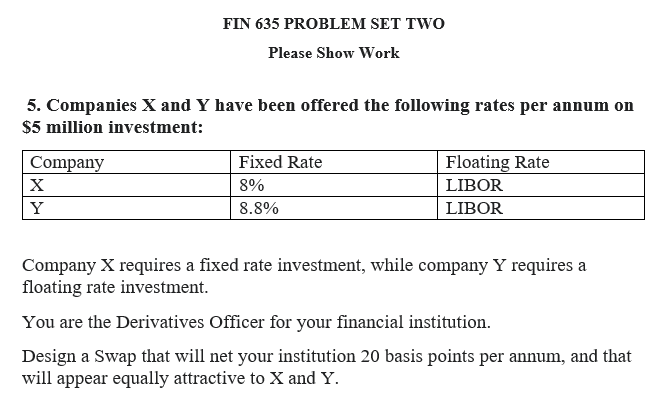

1. An American Financial Institution has made a loan commitment of 10,000,000 to a client which is likely to be taken down in 6 months. The current spot exchange rate is $1.50/. - Is the FI exposed to a dollar depreciation or appreciation? - If the spot rate six months from today is $1.6/, what amount of dollars is needed if the loan is taken down and the FI is not hedged? - If it decides to hedge using futures, should the FI buy or sell futures? - A sixmonth futures contract is available for $1.53/. What net amount would be needed to fund the loan at the end of six months if the FI had hedged using the 10 million futures contract? Assume that the futures prices are equal to the spot prices at the time of payment. 2. Union Corp must make a single payment of 5 million in six months at the maturity of a payable to a French firm. The finance manager expects the spot price of the to remain stable at the current rate of $1.60/. But as a precaution, the manager is concerned that the rate could rise as high as $1.70/ or fall as low as $1.50/. Because of this uncertainty, the manager recommends that Union Corp hedge the payment using either options or futures. Six months Call and Put options with an exercise price of $1.60/ are available. The Call sells for $.08/ and the Put sells for $.04/. A six-month futures contract on is trading at $1.60/. - Should the manager be worried about the dollar depreciating or appreciating? - If Union Corp decides to hedge using options, should it buy Calls or Puts to hedge the payment? Why? - If futures are used to hedge, should the company buy or sell futures? Why? - What will be the net payment on the payable if an option contact was used? Assume the following three scenarios: the spot price in six months will be $1.50/,$1.60/, or $1.70/. - What will be the net payment if futures had been used to hedge using the same scenarios as above. - Which method of hedging is preferable? Please Show Work 3. Explain what an arbitrageur would do in the following circumstances. - $/SF exchange rate is $.51/SF, the Swiss risk-free rate is 4% per year, the US risk free rate is 6% per year, and a SF Call option with an exercise price of $.50/SF and a three-month expiration is trading at \$.01/SF. - $/SF exchange rate is $.48/SF, the Swiss risk-free rate is 4% per year, the US risk free rate is 6% per year, and a SF Put option with an exercise price of $.50/SF and a three-month expiration is trading at $.01/SF. - $/SF exchange rate is $.52/SF, the Swiss risk-free rate is 4% per year, the US risk free rate is 6% per year, and a SF Put option with an exercise price of $.50/SF and a three-month expiration is trading at \$.0075, and a SF Call with similar terms is trading at $$.04 4. Consider two firms with the following borrowing costs: The British firm wishes to borrow US dollars at a fixed rate of interest. The US firm wishes to borrow sterling at a fixed rate of interest. Design a swap that will net a bank, acting as an intermediary, 10 basis points per annum and that will produce a gain of 15 basis points per annum for each of the two companies. FIN 635 PROBLEM SET TWO Please Show Work 4. Consider two firms with the following borrowing costs: The British firm wishes to borrow US dollars at a fixed rate of interest. The US firm wishes to borrow sterling at a fixed rate of interest. Design a swap that will net a bank, acting as an intermediary, 10 basis points per annum and that will produce a gain of 15 basis points per annum for each of the two companies. 5. Companies X and Y have been offered the following rates per annum on $5 million investment: Company X requires a fixed rate investment, while company Y requires a floating rate investment. You are the Derivatives Officer for your financial institution. Design a Swap that will net your institution 20 basis points per annum, and that will appear equally attractive to X and Y

1. An American Financial Institution has made a loan commitment of 10,000,000 to a client which is likely to be taken down in 6 months. The current spot exchange rate is $1.50/. - Is the FI exposed to a dollar depreciation or appreciation? - If the spot rate six months from today is $1.6/, what amount of dollars is needed if the loan is taken down and the FI is not hedged? - If it decides to hedge using futures, should the FI buy or sell futures? - A sixmonth futures contract is available for $1.53/. What net amount would be needed to fund the loan at the end of six months if the FI had hedged using the 10 million futures contract? Assume that the futures prices are equal to the spot prices at the time of payment. 2. Union Corp must make a single payment of 5 million in six months at the maturity of a payable to a French firm. The finance manager expects the spot price of the to remain stable at the current rate of $1.60/. But as a precaution, the manager is concerned that the rate could rise as high as $1.70/ or fall as low as $1.50/. Because of this uncertainty, the manager recommends that Union Corp hedge the payment using either options or futures. Six months Call and Put options with an exercise price of $1.60/ are available. The Call sells for $.08/ and the Put sells for $.04/. A six-month futures contract on is trading at $1.60/. - Should the manager be worried about the dollar depreciating or appreciating? - If Union Corp decides to hedge using options, should it buy Calls or Puts to hedge the payment? Why? - If futures are used to hedge, should the company buy or sell futures? Why? - What will be the net payment on the payable if an option contact was used? Assume the following three scenarios: the spot price in six months will be $1.50/,$1.60/, or $1.70/. - What will be the net payment if futures had been used to hedge using the same scenarios as above. - Which method of hedging is preferable? Please Show Work 3. Explain what an arbitrageur would do in the following circumstances. - $/SF exchange rate is $.51/SF, the Swiss risk-free rate is 4% per year, the US risk free rate is 6% per year, and a SF Call option with an exercise price of $.50/SF and a three-month expiration is trading at \$.01/SF. - $/SF exchange rate is $.48/SF, the Swiss risk-free rate is 4% per year, the US risk free rate is 6% per year, and a SF Put option with an exercise price of $.50/SF and a three-month expiration is trading at $.01/SF. - $/SF exchange rate is $.52/SF, the Swiss risk-free rate is 4% per year, the US risk free rate is 6% per year, and a SF Put option with an exercise price of $.50/SF and a three-month expiration is trading at \$.0075, and a SF Call with similar terms is trading at $$.04 4. Consider two firms with the following borrowing costs: The British firm wishes to borrow US dollars at a fixed rate of interest. The US firm wishes to borrow sterling at a fixed rate of interest. Design a swap that will net a bank, acting as an intermediary, 10 basis points per annum and that will produce a gain of 15 basis points per annum for each of the two companies. FIN 635 PROBLEM SET TWO Please Show Work 4. Consider two firms with the following borrowing costs: The British firm wishes to borrow US dollars at a fixed rate of interest. The US firm wishes to borrow sterling at a fixed rate of interest. Design a swap that will net a bank, acting as an intermediary, 10 basis points per annum and that will produce a gain of 15 basis points per annum for each of the two companies. 5. Companies X and Y have been offered the following rates per annum on $5 million investment: Company X requires a fixed rate investment, while company Y requires a floating rate investment. You are the Derivatives Officer for your financial institution. Design a Swap that will net your institution 20 basis points per annum, and that will appear equally attractive to X and Y Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Guide To Audit Data Analytics

Authors: AICPA

1st Edition

1945498641, 978-1945498640