Question

1. Answer all parts of the following question. [25 marks in total.] a) Briefly explain the Capital Asset Pricing Model (CAPM). (5 marks) b) Explain

1. Answer all parts of the following question. [25 marks in total.] a) Briefly explain the Capital Asset Pricing Model (CAPM). (5 marks)

b) Explain how the CAPM can be used to inform mean-variance portfolio decisions in practice, and how the existence of transaction costs might challenge the validity of the CAPM. (10 marks)

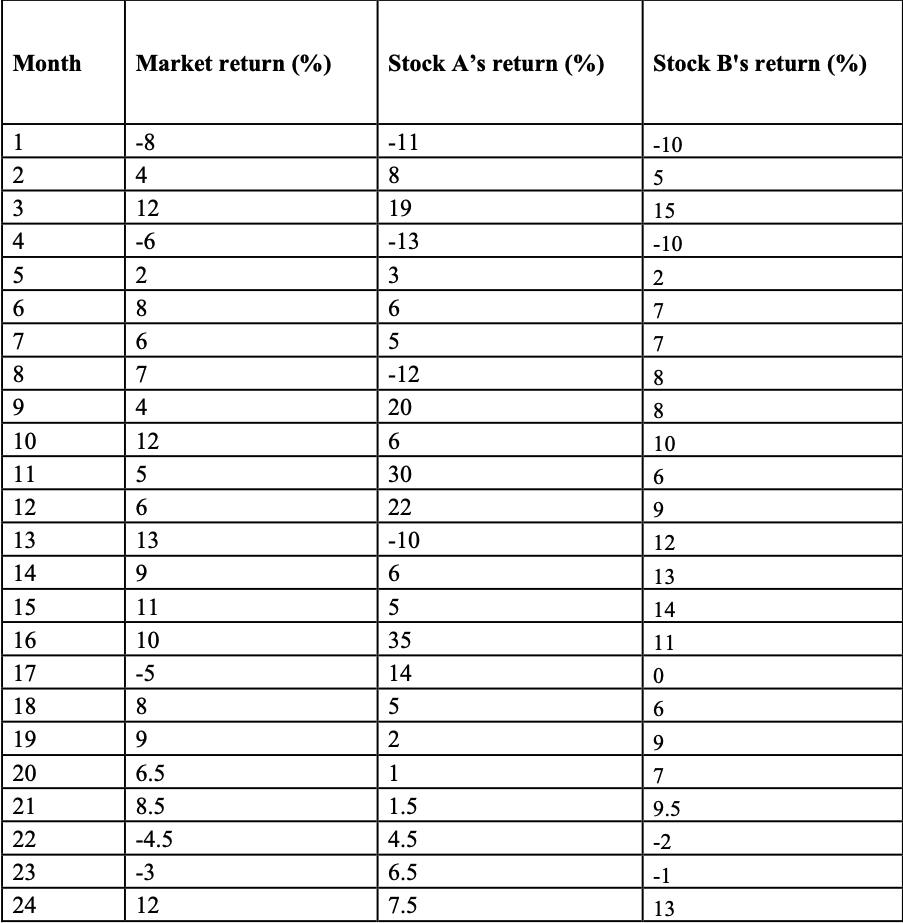

c) The following table provides the observed returns for the past 24 months on the market and on stocks A and B. Calculate the expected return, variance, and standard deviation for the market and a portfolio X that consists of A and B. For the portfolio X, dynamic rebalancing is applied for each month such that your portfolio X has 10% in A and 90% in B. Calculate and interpret beta for portfolio X. (10 marks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Portfolio Performance Measurement And Benchmarking

Authors: Jon Christopherson, David Carino, Wayne Ferson

1st Edition

0071496653, 978-0071496650