Answered step by step

Verified Expert Solution

Question

1 Approved Answer

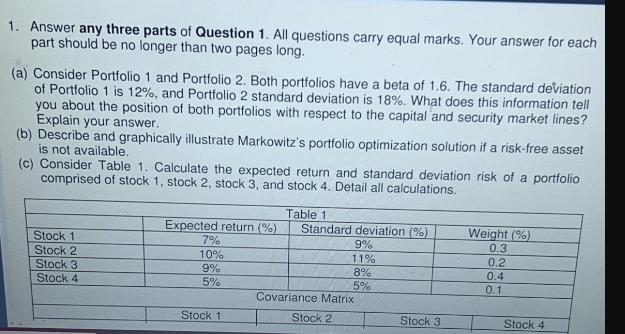

1. Answer any three parts of Question 1. All questions carry equal marks. Your answer for each part should be no longer than two

1. Answer any three parts of Question 1. All questions carry equal marks. Your answer for each part should be no longer than two pages long. (a) Consider Portfolio 1 and Portfolio 2. Both portfolios have a beta of 1.6. The standard deviation of Portfolio 1 is 12%, and Portfolio 2 standard deviation is 18%. What does this information tell you about the position of both portfolios with respect to the capital and security market lines? Explain your answer. (b) Describe and graphically illustrate Markowitz's portfolio optimization solution if a risk-free asset is not available. (c) Consider Table 1. Calculate the expected return and standard deviation risk of a portfolio comprised of stock 1, stock 2, stock 3, and stock 4. Detail all calculations. Stock 1. Stock 2 Stock 3 Stock 4 Expected return (%) 7% 10% 9% 5% Stock 1 Table 1 Standard deviation (%) 9% 11% 8% 5% Covariance Matrix Stock 2 Stock 3 Weight (%) 0.3 0.2 0.4 0.1 Stock 4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Answer a The information provided about Portfolio 1 and Portfolio 2 allows us to analyze their positions with respect to the capital market line CML and security market line SML Both portfolios have t...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Elements Of Chemical Reaction Engineering

Authors: H. Fogler

6th Edition

013548622X, 978-0135486221