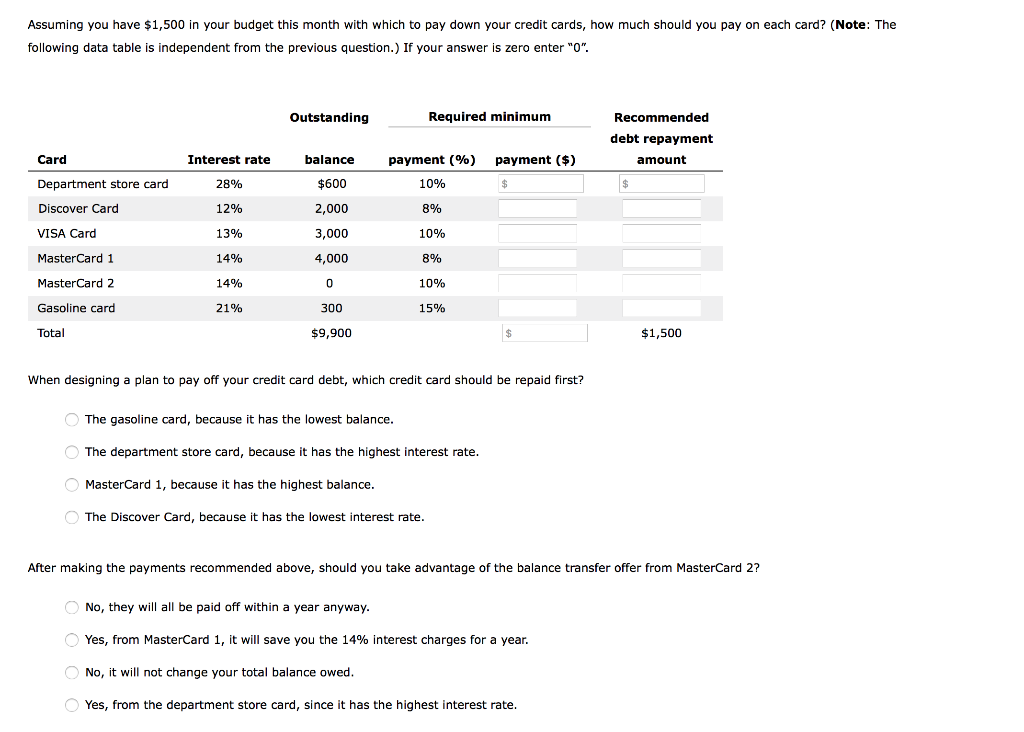

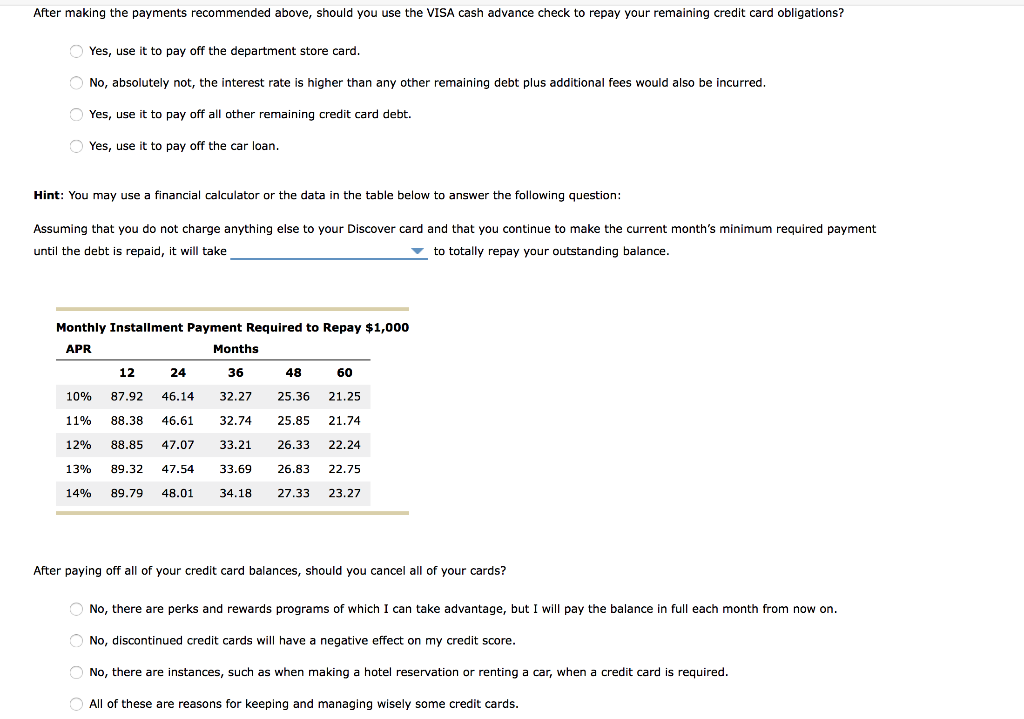

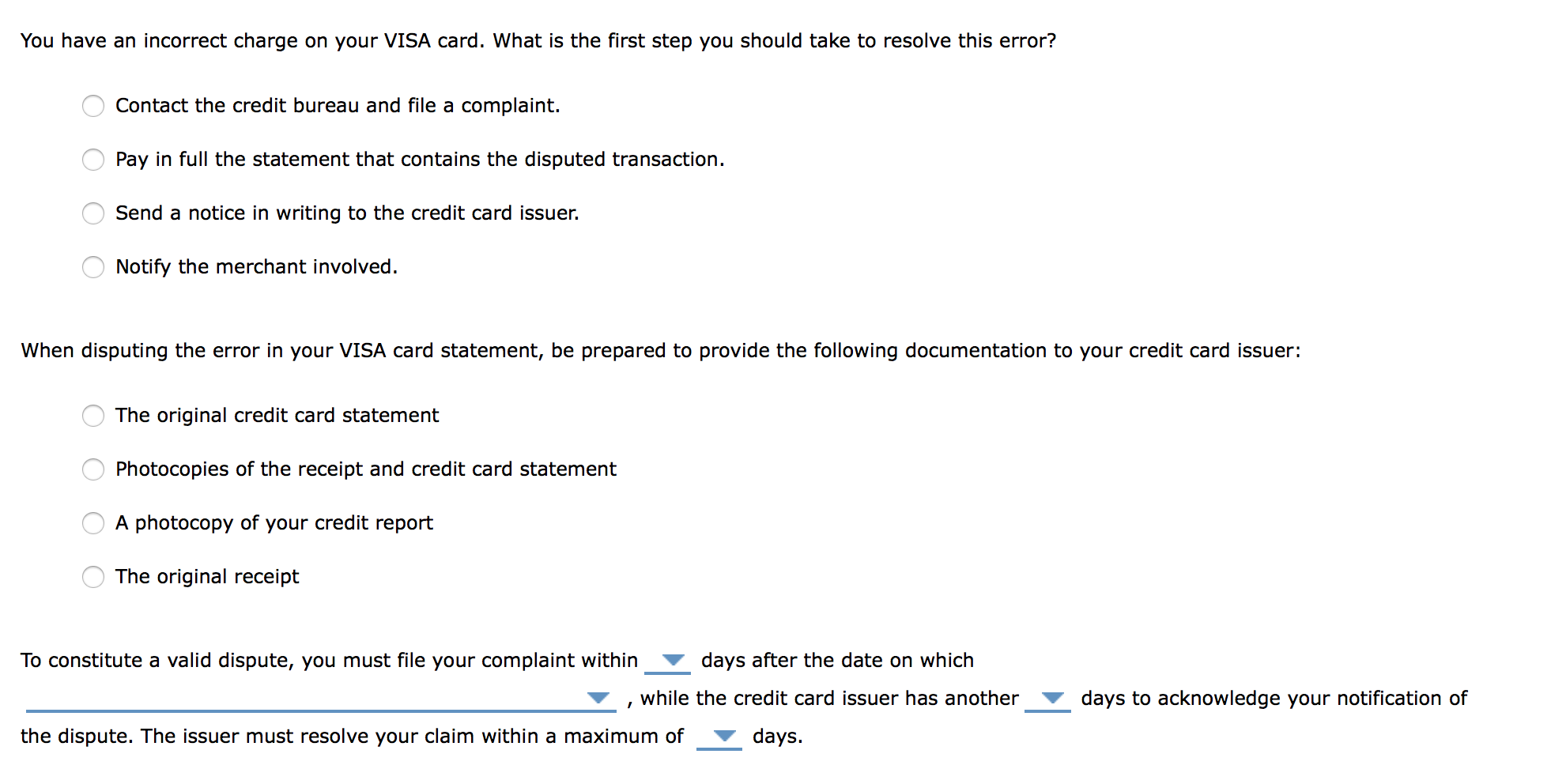

1. Apply What You've Learned - Managing Credit Cards and ConsumerLoans Scenario: You are 30 years old, married, have two children, and household income (take-home pay) of $3,500 per month. Your credit and consumer debt is as follows: Car loan, 6% interest rate, $10,000 balance, $295 per month Department store card, 28% interest rate, $600 balance, minimum payment 5% of balance Discover Card, 12% interest rate, $2,000 balance, minimum payment 2% of balance VISA Card, 13% interest rate, $3,000 balance, minimum payment 2% of balance MasterCard 1, 14% interest rate, $4,000 balance, minimum payment 2% of balance MasterCard 2, 14% interest rate, $0 balance, minimum payment 2% of balance Gasoline card, 21% interest rate, $300 balance, minimum payment 5% of balance Assume all credit cards will assess a $35 late fee and ongoing penalty interest of 8% above the current rate if you miss a payment. Your recent VISA card statement came with a blank cash advance check (for up to $10,000) with terms of 23.99% APR and a fee of 3% if you use it. Your recent MasterCard 2 statement came with a balance transfer offer (up to $4,000) with no fee and 0% APR for 12 months, after which the normal interest rate applies. You recently found an incorrect amount charged on your VISA card from a store you frequent often. You'd like to come up with a plan to eliminate all of your credit card debt. In general, is it a good idea to make only minimum payments on your credit cards? Yes, this allows you more flexibility in your cash budget. O Yes, you can invest the money saved each month to earn interest. No, it will cause your interest rate to go up. o No, the small payment requirement is mathematically guaranteed to keep you in debt for many years. Assuming you have $1,500 in your budget this month with which to pay down your credit cards, how much should you pay on each card? (Note: The following data table is independent from the previous question.) If your answer is zero enter "0". Outstanding Required minimum Recommended debt repayment amount Card Interest rate 28% balance $600 Department store card payment (%) payment ($) 10% 8% $ Discover Card 12% 2,000 VISA Card 13% 3,000 10% 14% 4,000 8% MasterCard 1 MasterCard 2 14% 0 10% 21% 300 15% Gasoline card Total $9,900 $ $1,500 When designing a plan to pay off your credit card debt, which credit card should be repaid first? The gasoline card, because it has the lowest balance. The department store card, because it has the highest interest rate. MasterCard 1, because it has the highest balance. The Discover Card, because it has the lowest interest rate. . After making the payments recommended above, should you take advantage of the balance transfer offer from MasterCard 2? No, they will all be paid off within a year anyway. Yes, from MasterCard 1, it will save you the 14% interest charges for a year. No, it will not change your total balance owed. Yes, from the department store card, since it has the highest interest rate. After making the payments recommended above, should you use the VISA cash advance check to repay your remaining credit card obligations? Yes, use it to pay off the department store card. No, absolutely not, the interest rate is higher than any other remaining debt plus additional fees would also be incurred. Yes, use it to pay off all other remaining credit card debt. Yes, use it to pay off the car loan. Hint: You may use a financial calculator or the data in the table below to answer the following question: Assuming that you do not charge anything else to your Discover card and that you continue to make the current month's minimum required payment until the debt is repaid, it will take to totally repay your outstanding balance. Monthly Installment Payment Required to Repay $1,000 APR Months 12 24 36 48 60 10% 87.92 46.14 32.27 25.36 21.25 11% 88.38 46.61 32.74 25.85 21.74 12% 88.85 47.07 33.21 26.33 22.24 13% 89.32 47.54 33.69 26.83 22.75 14% 89.79 48.01 34.18 27.33 23.27 After paying off all of your credit card balances, should you cancel all of your cards? No, there are perks and rewards programs of which I can take advantage, but I will pay the balance in full each month from now on. No, discontinued credit cards will have a negative effect on my credit score. No, there are instances, such as when making a hotel reservation or renting a car, when a credit card is required. All of these are reasons for keeping and managing wisely some credit cards. You have an incorrect charge on your VISA card. What is the first step you should take to resolve this error? Contact the credit bureau and file a complaint. Pay in full the statement that contains the disputed transaction. Send a notice in writing to the credit card issuer. Notify the merchant involved. When disputing the error in your VISA card statement, be prepared to provide the following documentation to your credit card issuer: The original credit card statement Photocopies of the receipt and credit card statement A photocopy of your credit report The original receipt To constitute a valid dispute, you must file your complaint within days after the date on which while the credit card issuer has another days to acknowledge your notification of the dispute. The issuer must resolve your claim within a maximum of days. 1. Apply What You've Learned - Managing Credit Cards and ConsumerLoans Scenario: You are 30 years old, married, have two children, and household income (take-home pay) of $3,500 per month. Your credit and consumer debt is as follows: Car loan, 6% interest rate, $10,000 balance, $295 per month Department store card, 28% interest rate, $600 balance, minimum payment 5% of balance Discover Card, 12% interest rate, $2,000 balance, minimum payment 2% of balance VISA Card, 13% interest rate, $3,000 balance, minimum payment 2% of balance MasterCard 1, 14% interest rate, $4,000 balance, minimum payment 2% of balance MasterCard 2, 14% interest rate, $0 balance, minimum payment 2% of balance Gasoline card, 21% interest rate, $300 balance, minimum payment 5% of balance Assume all credit cards will assess a $35 late fee and ongoing penalty interest of 8% above the current rate if you miss a payment. Your recent VISA card statement came with a blank cash advance check (for up to $10,000) with terms of 23.99% APR and a fee of 3% if you use it. Your recent MasterCard 2 statement came with a balance transfer offer (up to $4,000) with no fee and 0% APR for 12 months, after which the normal interest rate applies. You recently found an incorrect amount charged on your VISA card from a store you frequent often. You'd like to come up with a plan to eliminate all of your credit card debt. In general, is it a good idea to make only minimum payments on your credit cards? Yes, this allows you more flexibility in your cash budget. O Yes, you can invest the money saved each month to earn interest. No, it will cause your interest rate to go up. o No, the small payment requirement is mathematically guaranteed to keep you in debt for many years. Assuming you have $1,500 in your budget this month with which to pay down your credit cards, how much should you pay on each card? (Note: The following data table is independent from the previous question.) If your answer is zero enter "0". Outstanding Required minimum Recommended debt repayment amount Card Interest rate 28% balance $600 Department store card payment (%) payment ($) 10% 8% $ Discover Card 12% 2,000 VISA Card 13% 3,000 10% 14% 4,000 8% MasterCard 1 MasterCard 2 14% 0 10% 21% 300 15% Gasoline card Total $9,900 $ $1,500 When designing a plan to pay off your credit card debt, which credit card should be repaid first? The gasoline card, because it has the lowest balance. The department store card, because it has the highest interest rate. MasterCard 1, because it has the highest balance. The Discover Card, because it has the lowest interest rate. . After making the payments recommended above, should you take advantage of the balance transfer offer from MasterCard 2? No, they will all be paid off within a year anyway. Yes, from MasterCard 1, it will save you the 14% interest charges for a year. No, it will not change your total balance owed. Yes, from the department store card, since it has the highest interest rate. After making the payments recommended above, should you use the VISA cash advance check to repay your remaining credit card obligations? Yes, use it to pay off the department store card. No, absolutely not, the interest rate is higher than any other remaining debt plus additional fees would also be incurred. Yes, use it to pay off all other remaining credit card debt. Yes, use it to pay off the car loan. Hint: You may use a financial calculator or the data in the table below to answer the following question: Assuming that you do not charge anything else to your Discover card and that you continue to make the current month's minimum required payment until the debt is repaid, it will take to totally repay your outstanding balance. Monthly Installment Payment Required to Repay $1,000 APR Months 12 24 36 48 60 10% 87.92 46.14 32.27 25.36 21.25 11% 88.38 46.61 32.74 25.85 21.74 12% 88.85 47.07 33.21 26.33 22.24 13% 89.32 47.54 33.69 26.83 22.75 14% 89.79 48.01 34.18 27.33 23.27 After paying off all of your credit card balances, should you cancel all of your cards? No, there are perks and rewards programs of which I can take advantage, but I will pay the balance in full each month from now on. No, discontinued credit cards will have a negative effect on my credit score. No, there are instances, such as when making a hotel reservation or renting a car, when a credit card is required. All of these are reasons for keeping and managing wisely some credit cards. You have an incorrect charge on your VISA card. What is the first step you should take to resolve this error? Contact the credit bureau and file a complaint. Pay in full the statement that contains the disputed transaction. Send a notice in writing to the credit card issuer. Notify the merchant involved. When disputing the error in your VISA card statement, be prepared to provide the following documentation to your credit card issuer: The original credit card statement Photocopies of the receipt and credit card statement A photocopy of your credit report The original receipt To constitute a valid dispute, you must file your complaint within days after the date on which while the credit card issuer has another days to acknowledge your notification of the dispute. The issuer must resolve your claim within a maximum of days