1. Based on the article above, what factor would you think determines how firms can pass on costs or retain profit shares from sales of a product when key input prices fluctuate? 2. The article above mentions the product Aspirin and Coffee. a) Is Aspirin likely to have an elastic or inelastic Demand Curve? b) Is Coffee likely to have an elastic or inelastic Demand Curve? 3. Looking at the Figure above, what do you conclude: Which demand curve, elastic or inelastic, is more beneficial to consumers in terms of Price decrease? Why?

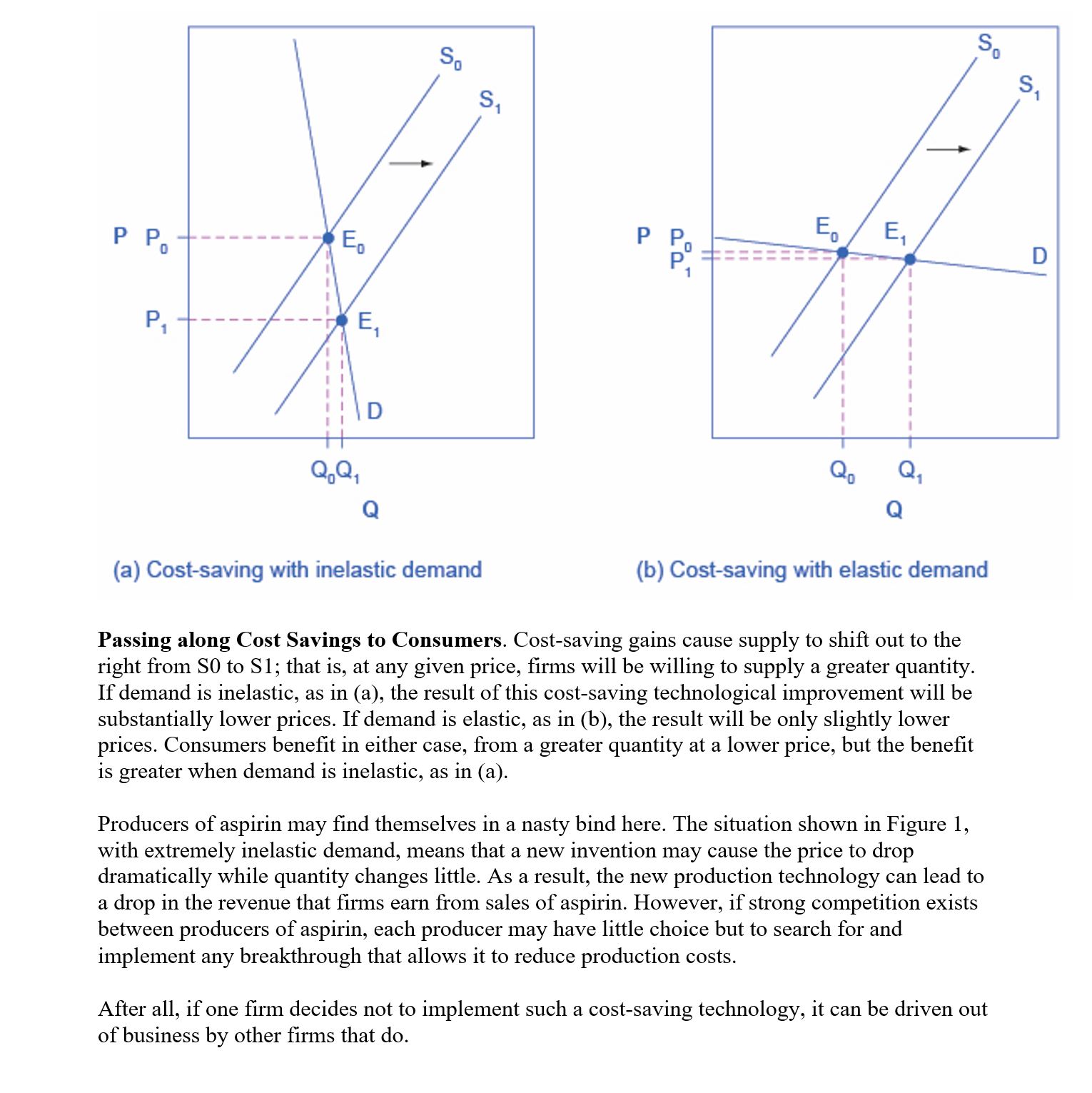

(a) Cost-saving with inelastic demand (b) Cost-saving with elastic demand Passing along Cost Savings to Consumers. Cost-saving gains cause supply to shift out to the right from SO to SI; that is, at any given price, rms will be willing to supply a greater quantity. If demand is inelastic, as in (a), the result of this costsaving technological improvement will be substantially lower prices. If demand is elastic, as in (b), the result will be only slightly lower prices. Consumers benet in either case, from a greater quantity at a lower price, but the benet is greater when demand is inelastic, as in (a). Producers of aspirin may nd themselves in a nasty bind here. The situation shown in Figure l, with extremely inelastic demand, means that a new invention may cause the price to drop dramatically while quantity changes little. As a result, the new production technology can lead to a drop in the revenue that rms earn from sales of aspirin. However, if strong competition exists between producers of aspirin, each producer may have little choice but to search for and implement any breakthrough that allows it to reduce production costs. After all, if one rm decides not to implement such a cost-saving technology, it can be driven out of business by other rms that do. Customers and Changing Costs We can see that understanding elasticity helps a rm set a price that maximizes total revenue. What happens if the farm's production costs change, though? And what is the impact on customers? Most businesses are continually trying to gure out ways to produce at a lower cost, as one path to earnng higher prots. It is a challenge to do this, though, when the price of a key input over which a rm has no control rises. If the cost of a key input rises, can the rm pass along those higher costs to consumers in the form of higher prices? For example, many chemical companies use petroleum as a key input, but they have no control over the world market price for crude oil. Coffee shops use coffee as a key input, but they have no control over the world market price of coffee. Conversely, if new and less expensive ways of producing are invented, can the rm keep the benets in the fonn of higher prots, or will the market pressure them to pass along the gains to consumers in the form of lower prices? The price elasticity of demand plays a key role in answering these questions. Imagine that, as a consumer of legal pharmaceutical products, you read a news story about a technological breakthrough in the production of aspirin: Now every aspirin factory can make aspirin more cheaply than it did before. What does this discovery mean to the rm? Figure 1, below, illustrates two possibilities. In Figure 1 (a), the demand curve is drawn as highly inelastic. In this case, a technological breakthrough that shifts supply to the right, from SO to 81, so that the equilibrium shifts from E0 to E1, creates a substantially lower price for the product with relatively little impact on the quantity sold. In Figure 1 (b), the demand curve is drawn as highly elastic. In this case, the technological breakthrough leads to a much greater quantity being sold in the market at very close to the original price. Consumers benefit more, in general, when the demand curve is more inelastic because the shift in the supply results in a much lower price for consumers