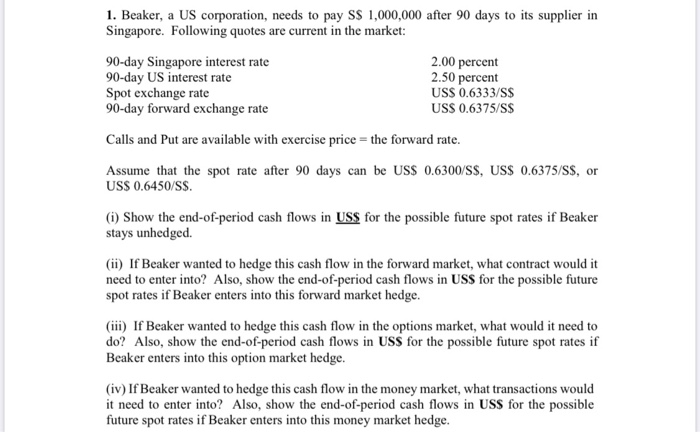

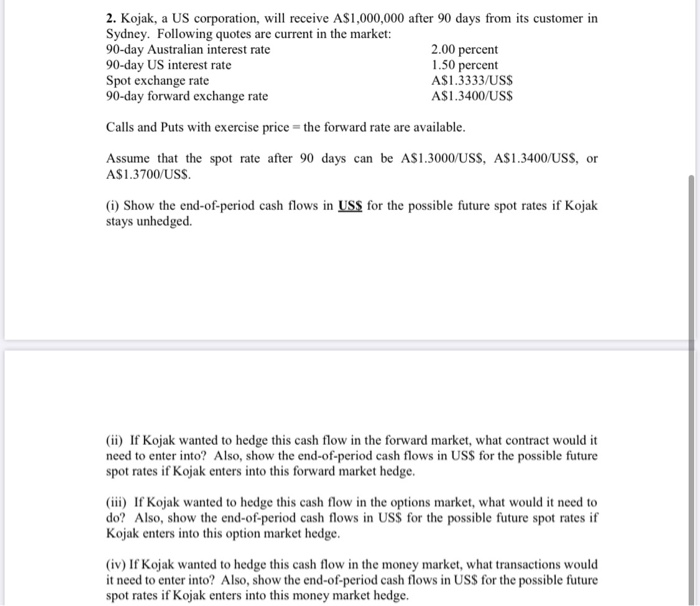

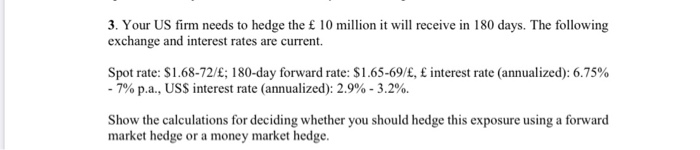

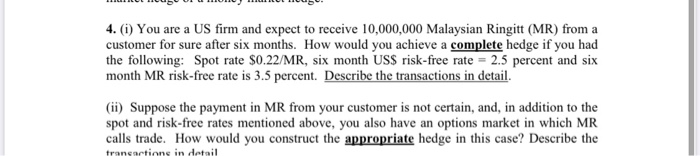

1. Beaker, a US corporation, needs to pay SS 1,000,000 after 90 days to its supplier in Singapore. Following quotes are current in the market: 90-day Singapore interest rate 90-day US interest rate Spot exchange rate 90-day forward exchange rate 2.00 percent 2.50 percent US$ 0.6333/S$ US$ 0.6375/SS Calls and Put are available with exercise price = the forward rate. Assume that the spot rate after 90 days can be US$ 0.6300/S$, US$ 0.6375/SS, or US$ 0.6450/S$. (i) Show the end-of-period cash flows in US$ for the possible future spot rates if Beaker stays unhedged. (ii) If Beaker wanted to hedge this cash flow in the forward market, what contract would it need to enter into? Also, show the end-of-period cash flows in USS for the possible future spot rates if Beaker enters into this forward market hedge. (iii) If Beaker wanted to hedge this cash flow in the options market, what would it need to do? Also, show the end-of-period cash flows in US$ for the possible future spot rates if Beaker enters into this option market hedge. (iv) If Beaker wanted to hedge this cash flow in the money market, what transactions would it need to enter into? Also, show the end-of-period cash flows in USS for the possible future spot rates if Beaker enters into this money market hedge. 2. Kojak, a US corporation, will receive A$1,000,000 after 90 days from its customer in Sydney. Following quotes are current in the market: 90-day Australian interest rate 2.00 percent 90-day US interest rate 1.50 percent Spot exchange rate A$1.3333/US$ 90-day forward exchange rate A$1.3400/US$ Calls and Puts with exercise price = the forward rate are available. Assume that the spot rate after 90 days can be A$1.3000/USS, A$ 1.3400/USS, or A$1.3700/USS. (i) Show the end-of-period cash flows in US$ for the possible future spot rates if Kojak stays unhedged. (ii) If Kojak wanted to hedge this cash flow in the forward market, what contract would it need to enter into? Also, show the end-of-period cash flows in USS for the possible future spot rates if Kojak enters into this forward market hedge. (iii) If Kojak wanted to hedge this cash flow in the options market, what would it need to do? Also, show the end-of-period cash flows in USS for the possible future spot rates if Kojak enters into this option market hedge. (iv) If Kojak wanted to hedge this cash flow in the money market, what transactions would it need to enter into? Also, show the end-of-period cash flows in USS for the possible future spot rates if Kojak enters into this money market hedge. 3. Your US firm needs to hedge the 10 million it will receive in 180 days. The following exchange and interest rates are current. Spot rate: $1.68-72/; 180-day forward rate: $1.65-69/, interest rate (annualized): 6.75% - 7% p.a., US$ interest rate (annualized): 2.9% - 3.2%. Show the calculations for deciding whether you should hedge this exposure using a forward market hedge or a money market hedge. LLOC Hub 1 U HU ILUL Hubu. 4. (i) You are a US firm and expect to receive 10,000,000 Malaysian Ringitt (MR) from a customer for sure after six months. How would you achieve a complete hedge if you had the following: Spot rate $0.22/MR, six month US$ risk-free rate = 2.5 percent and six month MR risk-free rate is 3.5 percent. Describe the transactions in detail. (ii) Suppose the payment in MR from your customer is not certain, and, in addition to the spot and risk-free rates mentioned above, you also have an options market in which MR calls trade. How would you construct the appropriate hedge in this case? Describe the transactions in detail 1. Beaker, a US corporation, needs to pay SS 1,000,000 after 90 days to its supplier in Singapore. Following quotes are current in the market: 90-day Singapore interest rate 90-day US interest rate Spot exchange rate 90-day forward exchange rate 2.00 percent 2.50 percent US$ 0.6333/S$ US$ 0.6375/SS Calls and Put are available with exercise price = the forward rate. Assume that the spot rate after 90 days can be US$ 0.6300/S$, US$ 0.6375/SS, or US$ 0.6450/S$. (i) Show the end-of-period cash flows in US$ for the possible future spot rates if Beaker stays unhedged. (ii) If Beaker wanted to hedge this cash flow in the forward market, what contract would it need to enter into? Also, show the end-of-period cash flows in USS for the possible future spot rates if Beaker enters into this forward market hedge. (iii) If Beaker wanted to hedge this cash flow in the options market, what would it need to do? Also, show the end-of-period cash flows in US$ for the possible future spot rates if Beaker enters into this option market hedge. (iv) If Beaker wanted to hedge this cash flow in the money market, what transactions would it need to enter into? Also, show the end-of-period cash flows in USS for the possible future spot rates if Beaker enters into this money market hedge. 2. Kojak, a US corporation, will receive A$1,000,000 after 90 days from its customer in Sydney. Following quotes are current in the market: 90-day Australian interest rate 2.00 percent 90-day US interest rate 1.50 percent Spot exchange rate A$1.3333/US$ 90-day forward exchange rate A$1.3400/US$ Calls and Puts with exercise price = the forward rate are available. Assume that the spot rate after 90 days can be A$1.3000/USS, A$ 1.3400/USS, or A$1.3700/USS. (i) Show the end-of-period cash flows in US$ for the possible future spot rates if Kojak stays unhedged. (ii) If Kojak wanted to hedge this cash flow in the forward market, what contract would it need to enter into? Also, show the end-of-period cash flows in USS for the possible future spot rates if Kojak enters into this forward market hedge. (iii) If Kojak wanted to hedge this cash flow in the options market, what would it need to do? Also, show the end-of-period cash flows in USS for the possible future spot rates if Kojak enters into this option market hedge. (iv) If Kojak wanted to hedge this cash flow in the money market, what transactions would it need to enter into? Also, show the end-of-period cash flows in USS for the possible future spot rates if Kojak enters into this money market hedge. 3. Your US firm needs to hedge the 10 million it will receive in 180 days. The following exchange and interest rates are current. Spot rate: $1.68-72/; 180-day forward rate: $1.65-69/, interest rate (annualized): 6.75% - 7% p.a., US$ interest rate (annualized): 2.9% - 3.2%. Show the calculations for deciding whether you should hedge this exposure using a forward market hedge or a money market hedge. LLOC Hub 1 U HU ILUL Hubu. 4. (i) You are a US firm and expect to receive 10,000,000 Malaysian Ringitt (MR) from a customer for sure after six months. How would you achieve a complete hedge if you had the following: Spot rate $0.22/MR, six month US$ risk-free rate = 2.5 percent and six month MR risk-free rate is 3.5 percent. Describe the transactions in detail. (ii) Suppose the payment in MR from your customer is not certain, and, in addition to the spot and risk-free rates mentioned above, you also have an options market in which MR calls trade. How would you construct the appropriate hedge in this case? Describe the transactions in detail