Answered step by step

Verified Expert Solution

Question

1 Approved Answer

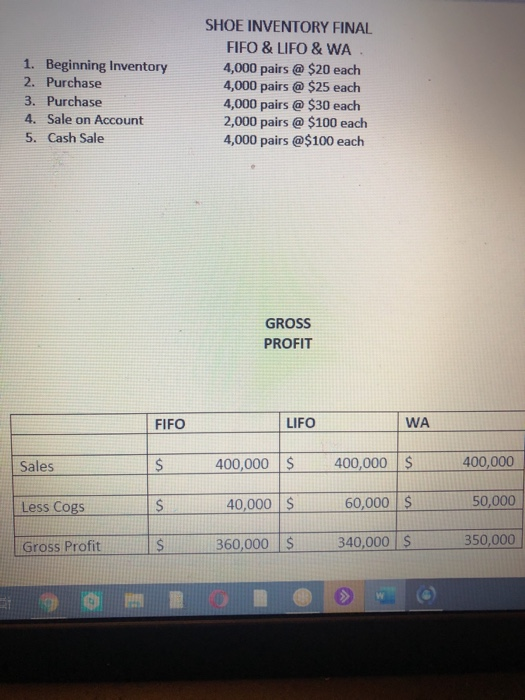

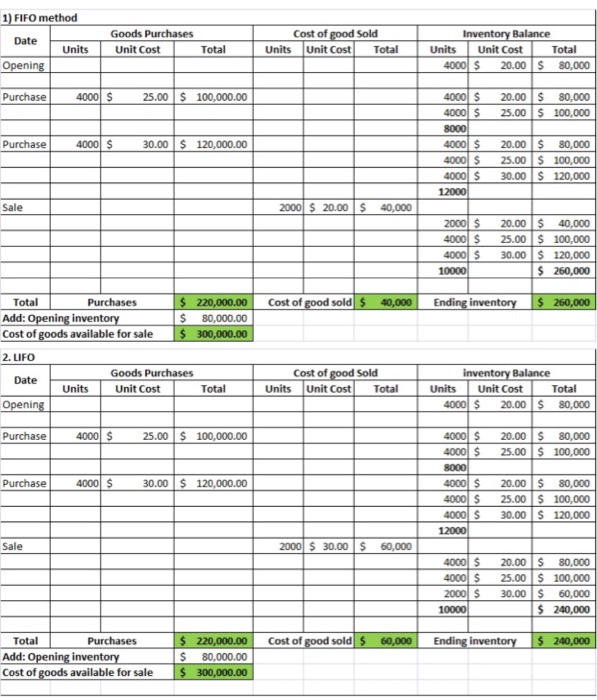

1. Beginning Inventory 2. Purchase 3. Purchase 4. Sale on Account 5. Cash Sale SHOE INVENTORY FINAL FIFO & LIFO & WA 4,000 pairs @

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Plant Auditing A Powerful Tool For Improving Metallurgical Plant Performance

Authors: Deepak Malhotra

1st Edition

0873354125, 978-0873354127