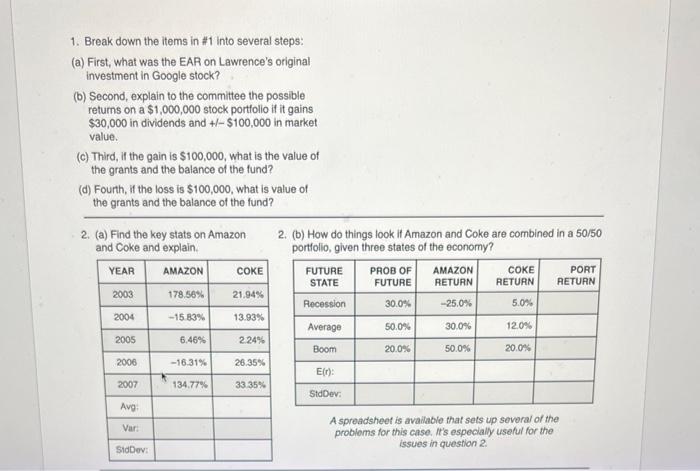

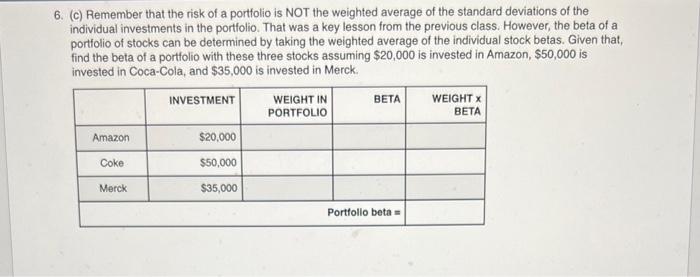

1. Break down the items in #1 into several steps: (a) First, what was the EAR on Lawrence's original investment in Google stock? (b) Second, explain to the committee the possible returns on a $1,000,000 stock porttolio it it gains $30,000 in dividends and +1$100,000 in market value. (c) Third, if the gain is $100,000, what is the value of the grants and the balance of the fund? (d) Fourth, if the loss is $100,000, what is value of the grants and the balance of the fund? 2. (a) Find the key stats on Amazon 2. (b) How do things look it Amazon and Coke are combined in a 50/50 and Coke and explain. portiolio, given three states of the economy? A spreadsheet is avallable that sets up several of the problems for this case. It's especially useful for the issues in question 2. 3. Committee members would like to invest in very sale things that also give a very high return. When they ask about this, how should Don Kraska reply? 4. As you determined in question #1, Google was a 5. (a) How many stocks should the committee want to pretty good investment. Why might Lawrence had see in the porttolio? been so insistent on the town of Webley selling (b) If this is a portfolio that is well-diversified, what Google and investing in a porttolio of stocks? should happen to systematic risk and unsystematic risk? (c) If this portfolio earns the historical large-cap market return of 12.0% and pays out about 5.0% a year in grants, by about how much should the porttolio grow (typically) each year? 6. (a) Explain the capital asset pricing model (CAPM). Tough so soon after seeing it for the first time. Try this: - First, for investors, the important risk of a stock isn't how the stock behaves by itself. (That is the stock's standard deviation, or its stand-alone risk.) Instead, what's important is how the stock affects a welldiversified porttolio. - Second, a measure of how a single stock affects a well-diversified portfolio - really, how it affects investing in the market overall - is something called beta. This beta measures how sensitive the returns on any particular stock are to the returns on the market. - Third, because of how beta is calculated (which we won't do), the beta of the market is 1.0. You can think of that as the average risk. So if you buy into the market - you bought an index fund for the S\&P 500 , for example - your return should be the risk-free rate plus a return for accepting average risk. This is r+ average risk premium = the expected return on the market, or E(r)=rf+(rmr)1.0. (Work that out to see what it really is.) A stock beta of, say, 2.0, means that this investment has 2x the average risk; a stock with a beta of, say, 0.5 has 1/2 the average risk. 6. (c) Remember that the risk of a portfolio is NOT the weighted average of the standard deviations of the individual investments in the portfolio. That was a key lesson from the previous class. However, the beta of a portfolio of stocks can be determined by taking the weighted average of the individual stock betas. Given that, find the beta of a portfolio with these three stocks assuming $20,000 is invested in Amazon, $50,000 is invested in Coca-Cola, and $35,000 is invested in Merck. 1. Break down the items in #1 into several steps: (a) First, what was the EAR on Lawrence's original investment in Google stock? (b) Second, explain to the committee the possible returns on a $1,000,000 stock porttolio it it gains $30,000 in dividends and +1$100,000 in market value. (c) Third, if the gain is $100,000, what is the value of the grants and the balance of the fund? (d) Fourth, if the loss is $100,000, what is value of the grants and the balance of the fund? 2. (a) Find the key stats on Amazon 2. (b) How do things look it Amazon and Coke are combined in a 50/50 and Coke and explain. portiolio, given three states of the economy? A spreadsheet is avallable that sets up several of the problems for this case. It's especially useful for the issues in question 2. 3. Committee members would like to invest in very sale things that also give a very high return. When they ask about this, how should Don Kraska reply? 4. As you determined in question #1, Google was a 5. (a) How many stocks should the committee want to pretty good investment. Why might Lawrence had see in the porttolio? been so insistent on the town of Webley selling (b) If this is a portfolio that is well-diversified, what Google and investing in a porttolio of stocks? should happen to systematic risk and unsystematic risk? (c) If this portfolio earns the historical large-cap market return of 12.0% and pays out about 5.0% a year in grants, by about how much should the porttolio grow (typically) each year? 6. (a) Explain the capital asset pricing model (CAPM). Tough so soon after seeing it for the first time. Try this: - First, for investors, the important risk of a stock isn't how the stock behaves by itself. (That is the stock's standard deviation, or its stand-alone risk.) Instead, what's important is how the stock affects a welldiversified porttolio. - Second, a measure of how a single stock affects a well-diversified portfolio - really, how it affects investing in the market overall - is something called beta. This beta measures how sensitive the returns on any particular stock are to the returns on the market. - Third, because of how beta is calculated (which we won't do), the beta of the market is 1.0. You can think of that as the average risk. So if you buy into the market - you bought an index fund for the S\&P 500 , for example - your return should be the risk-free rate plus a return for accepting average risk. This is r+ average risk premium = the expected return on the market, or E(r)=rf+(rmr)1.0. (Work that out to see what it really is.) A stock beta of, say, 2.0, means that this investment has 2x the average risk; a stock with a beta of, say, 0.5 has 1/2 the average risk. 6. (c) Remember that the risk of a portfolio is NOT the weighted average of the standard deviations of the individual investments in the portfolio. That was a key lesson from the previous class. However, the beta of a portfolio of stocks can be determined by taking the weighted average of the individual stock betas. Given that, find the beta of a portfolio with these three stocks assuming $20,000 is invested in Amazon, $50,000 is invested in Coca-Cola, and $35,000 is invested in Merck