Question

Video Tech Ltd manufactures video game machines. Market saturation and technological innovations have caused pricing pressures that have resulted in declining profits. To stem the

Video Tech Ltd manufactures video game machines. Market saturation and technological innovations have caused pricing pressures that have resulted in declining profits. To stem the slide in profits until new products can be introduced, top management has started to focus on achieving cost savings in manufacturing and increases in sales volume. Sales can be increased only if production volume increases. Therefore, an incentive program has been developed to reward those production managers who contribute to an increase in the number of units produced and achieve cost reductions. In addition, a just-in-time purchasing program has been implemented, and raw materials are purchased on an as-needed basis.

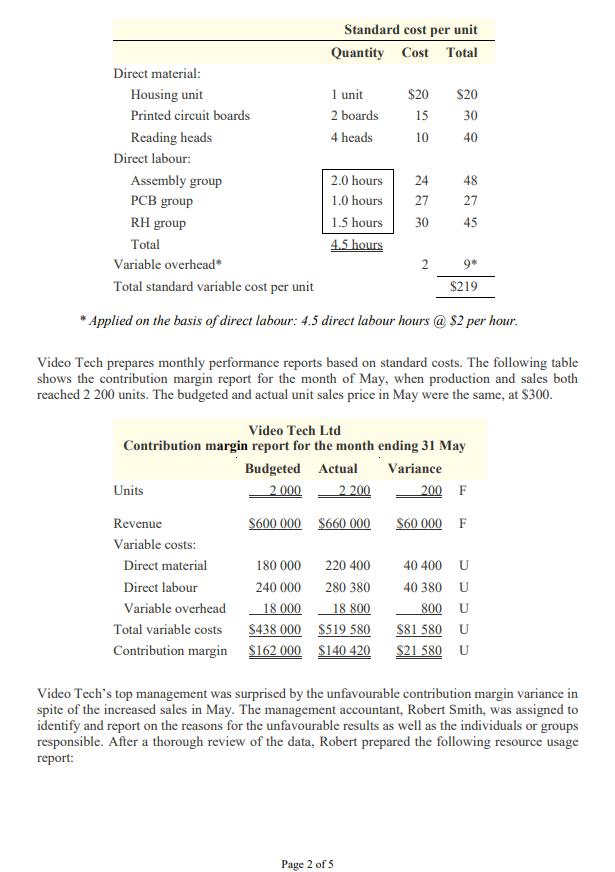

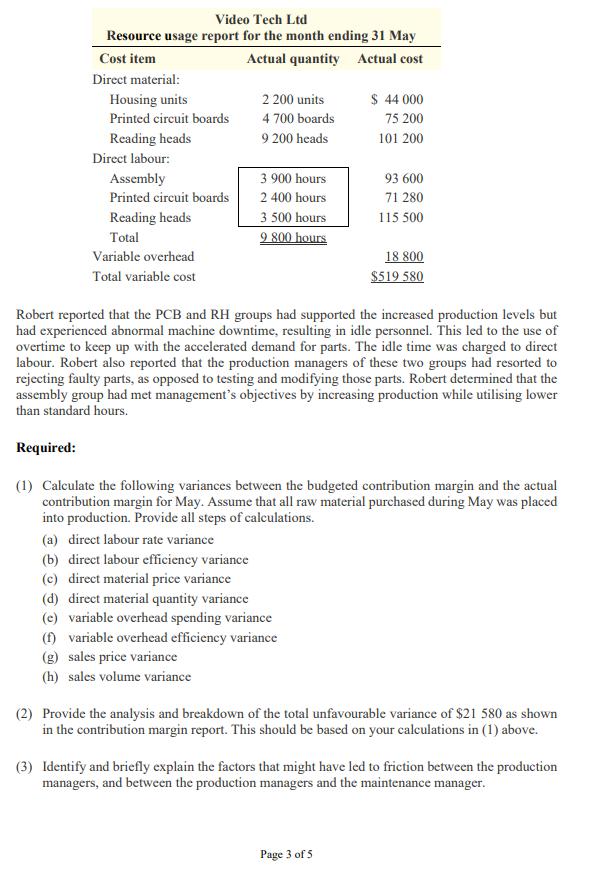

Direct material: Housing unit Printed circuit boards Reading heads Direct labour: Standard cost per unit Quantity Cost Total Assembly group PCB group RH group Total Variable overhead* 9* Total standard variable cost per unit $219 *Applied on the basis of direct labour: 4.5 direct labour hours @ $2 per hour. Units Revenue Variable costs: 1 unit 2 boards 4 heads Direct material Direct labour Variable overhead Total variable costs Contribution margin 2.0 hours 1.0 hours 1.5 hours 4.5 hours 180 000 240 000 18.000 $438 000 $162 000 $600 000 $660 000 $20 $20 15 30 10 40 223 220 400 280 380 18 800 $519 580 $140 420 Video Tech prepares monthly performance reports based on standard costs. The following table shows the contribution margin report for the month of May, when production and sales both reached 2 200 units. The budgeted and actual unit sales price in May were the same, at $300. 24 Video Tech Ltd Contribution margin report for the month ending 31 May Budgeted Actual Variance 2.000 2.200 Page 2 of 5 27 30 2 48 27 45 200 F $60 000 F 40 400 40 380 U U 800 U $81 580 U $21 580 U Video Tech's top management was surprised by the unfavourable contribution margin variance in spite of the increased sales in May. The management accountant, Robert Smith, was assigned to identify and report on the reasons for the unfavourable results as well as the individuals or groups responsible. After a thorough review of the data, Robert prepared the following resource usage report: Direct material: Housing unit Printed circuit boards Reading heads Direct labour: Standard cost per unit Quantity Cost Total Assembly group PCB group RH group Total Variable overhead* 9* Total standard variable cost per unit $219 *Applied on the basis of direct labour: 4.5 direct labour hours @ $2 per hour. Units Revenue Variable costs: 1 unit 2 boards 4 heads Direct material Direct labour Variable overhead Total variable costs Contribution margin 2.0 hours 1.0 hours 1.5 hours 4.5 hours 180 000 240 000 18.000 $438 000 $162 000 $600 000 $660 000 $20 $20 15 30 10 40 223 220 400 280 380 18 800 $519 580 $140 420 Video Tech prepares monthly performance reports based on standard costs. The following table shows the contribution margin report for the month of May, when production and sales both reached 2 200 units. The budgeted and actual unit sales price in May were the same, at $300. 24 Video Tech Ltd Contribution margin report for the month ending 31 May Budgeted Actual Variance 2.000 2.200 Page 2 of 5 27 30 2 48 27 45 200 F $60 000 F 40 400 40 380 U U 800 U $81 580 U $21 580 U Video Tech's top management was surprised by the unfavourable contribution margin variance in spite of the increased sales in May. The management accountant, Robert Smith, was assigned to identify and report on the reasons for the unfavourable results as well as the individuals or groups responsible. After a thorough review of the data, Robert prepared the following resource usage report: Direct material: Housing unit Printed circuit boards Reading heads Direct labour: Standard cost per unit Quantity Cost Total Assembly group PCB group RH group Total Variable overhead* 9* Total standard variable cost per unit $219 *Applied on the basis of direct labour: 4.5 direct labour hours @ $2 per hour. Units Revenue Variable costs: 1 unit 2 boards 4 heads Direct material Direct labour Variable overhead Total variable costs Contribution margin 2.0 hours 1.0 hours 1.5 hours 4.5 hours 180 000 240 000 18.000 $438 000 $162 000 $600 000 $660 000 $20 $20 15 30 10 40 223 220 400 280 380 18 800 $519 580 $140 420 Video Tech prepares monthly performance reports based on standard costs. The following table shows the contribution margin report for the month of May, when production and sales both reached 2 200 units. The budgeted and actual unit sales price in May were the same, at $300. 24 Video Tech Ltd Contribution margin report for the month ending 31 May Budgeted Actual Variance 2.000 2.200 Page 2 of 5 27 30 2 48 27 45 200 F $60 000 F 40 400 40 380 U U 800 U $81 580 U $21 580 U Video Tech's top management was surprised by the unfavourable contribution margin variance in spite of the increased sales in May. The management accountant, Robert Smith, was assigned to identify and report on the reasons for the unfavourable results as well as the individuals or groups responsible. After a thorough review of the data, Robert prepared the following resource usage report:

Step by Step Solution

3.50 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

Answer 1 Variances Direct material price variance 13900 Unfavorable Direct material quantity varianc...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial and Managerial Accounting

Authors: Horngren, Harrison, Oliver

3rd Edition

978-0132497992, 132913771, 132497972, 132497999, 9780132913775, 978-0132497978