1. Case Analysis Required Elements (Explain in detail): a. Identification and explanation of the main cost management problem using the cost management theory. b. Identify and explain of (5) external or internal causes that originates the proposed main cost management problem. c. With the information above, propose an adequate variance analysis for Xavier Mental Healths situation. d. With the results obtained above, Define and explain (5) cost management strategies oriented to solve the main cost management problem. e. Explain how these strategies could be implemented in your proposed Xavier Mental Healths cost management variance management system.

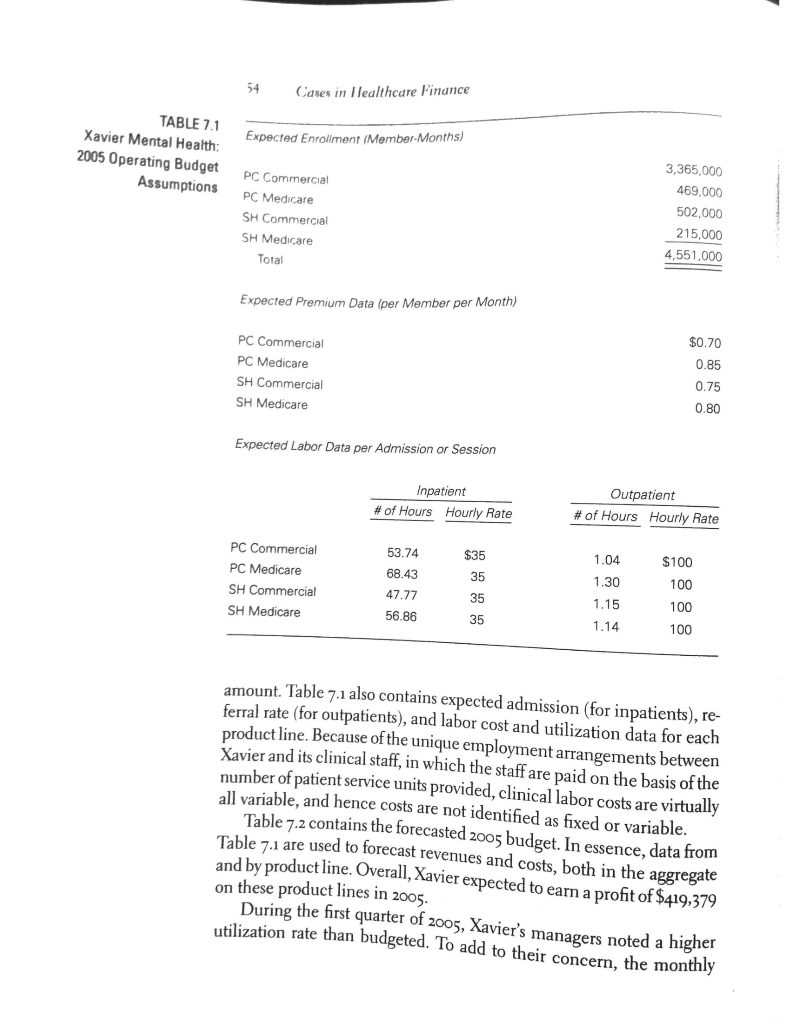

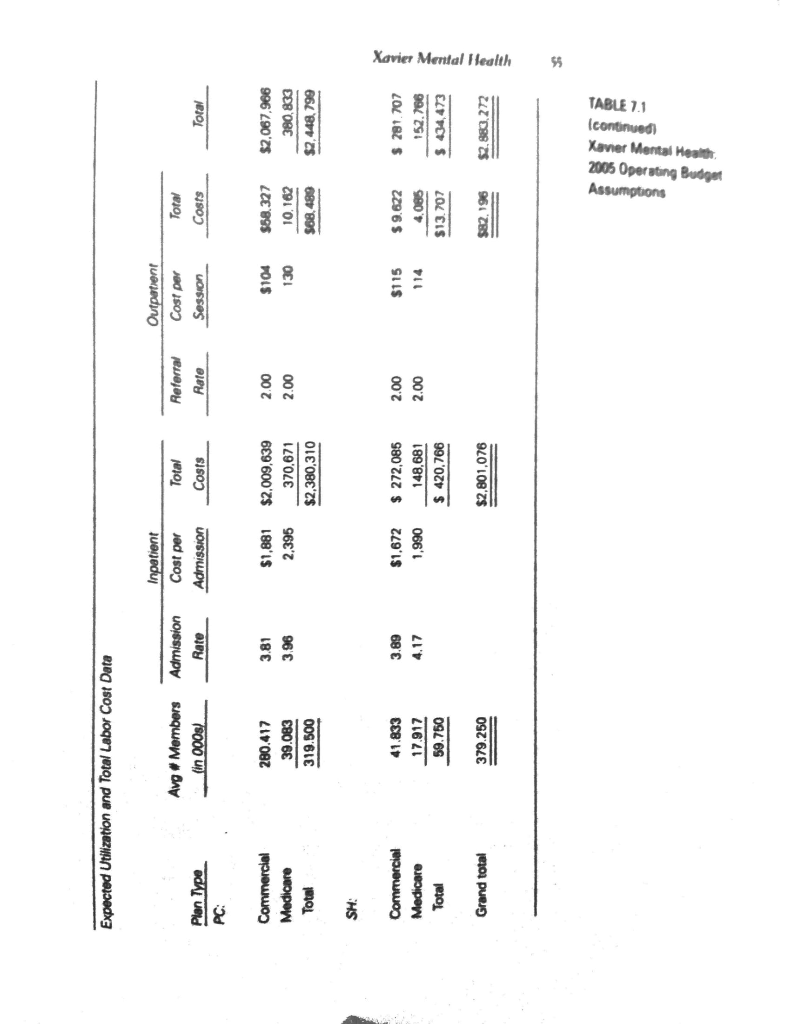

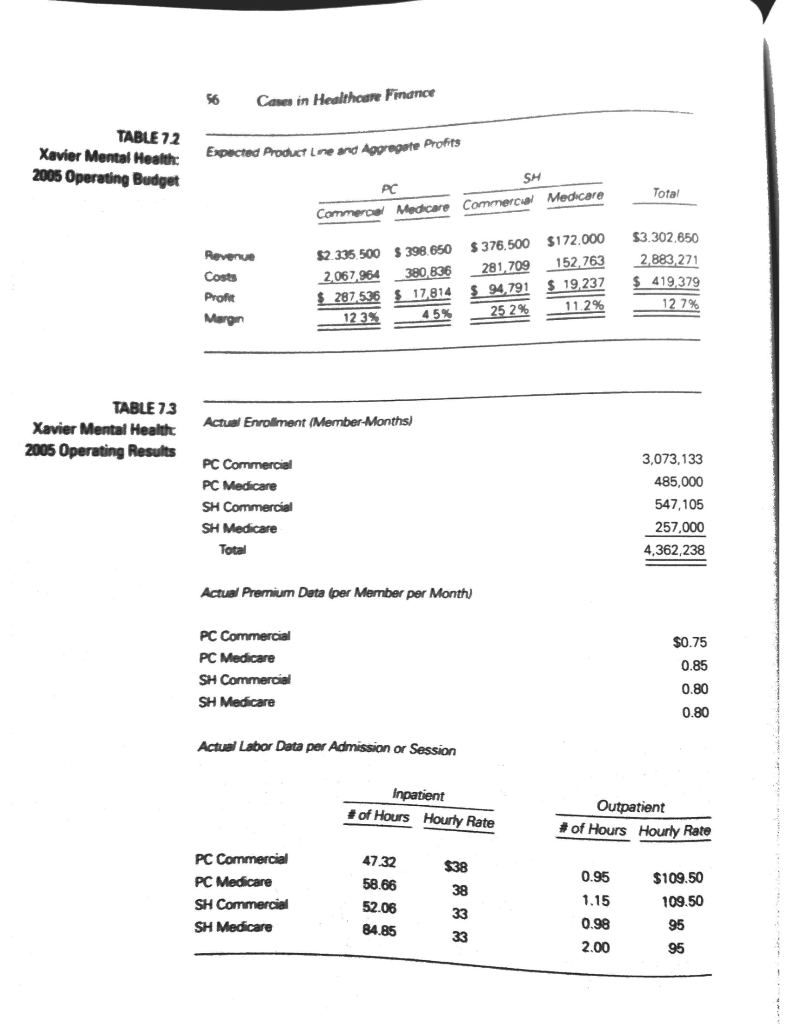

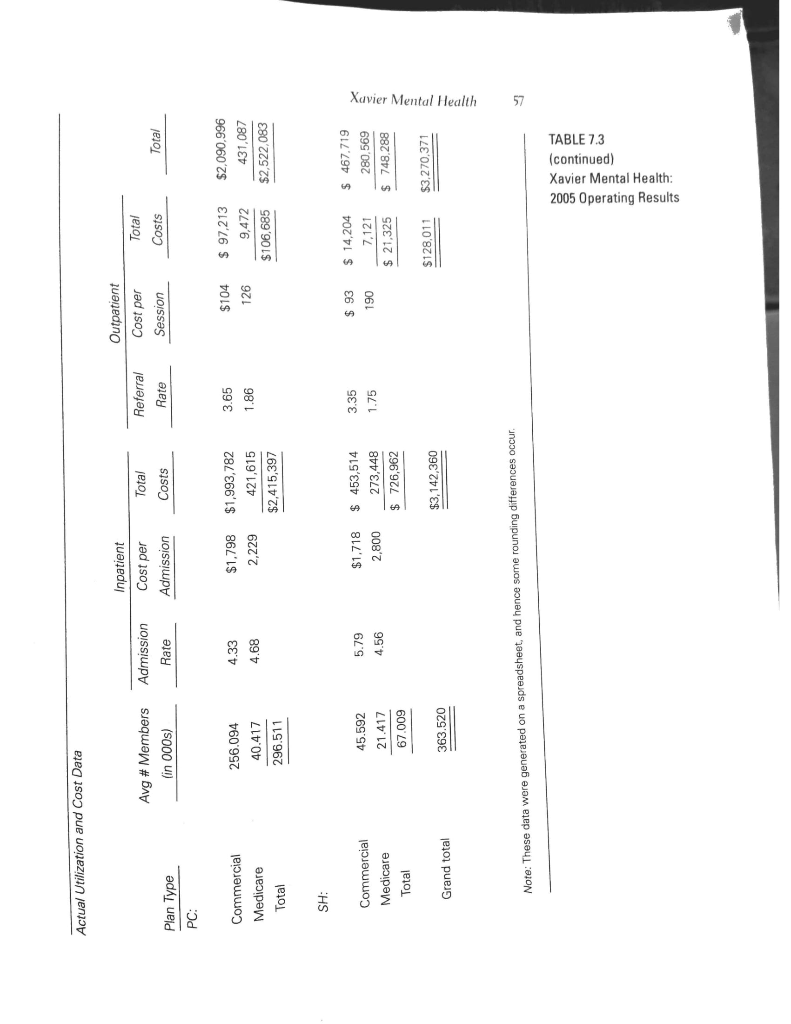

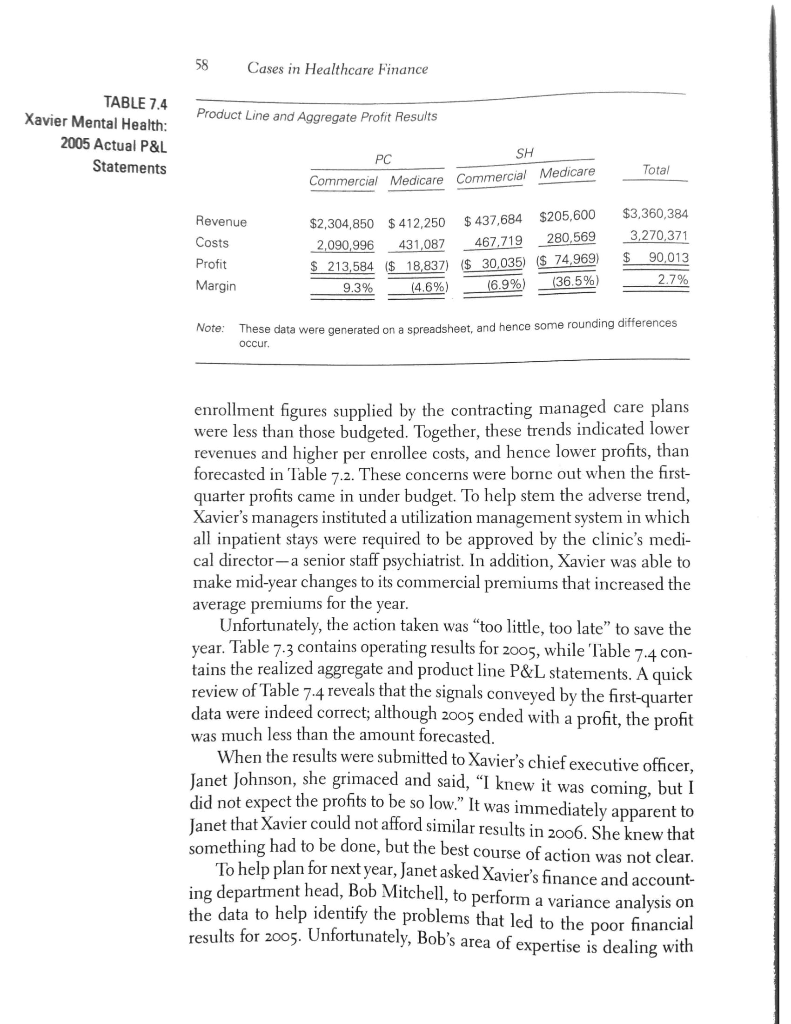

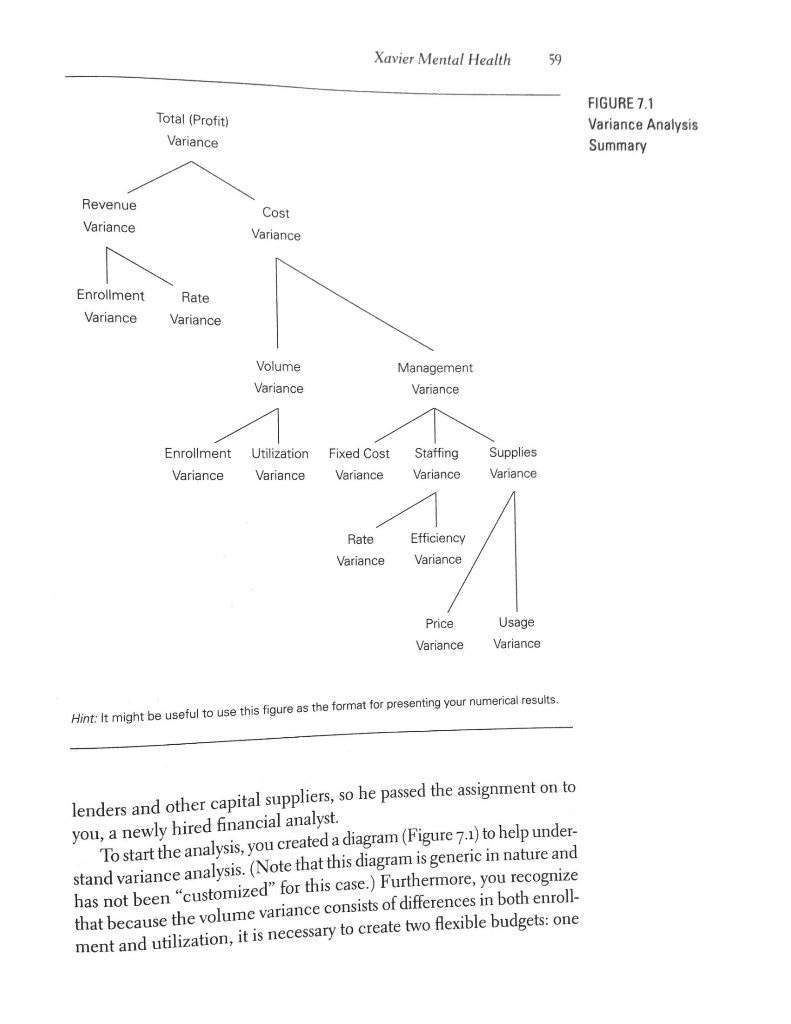

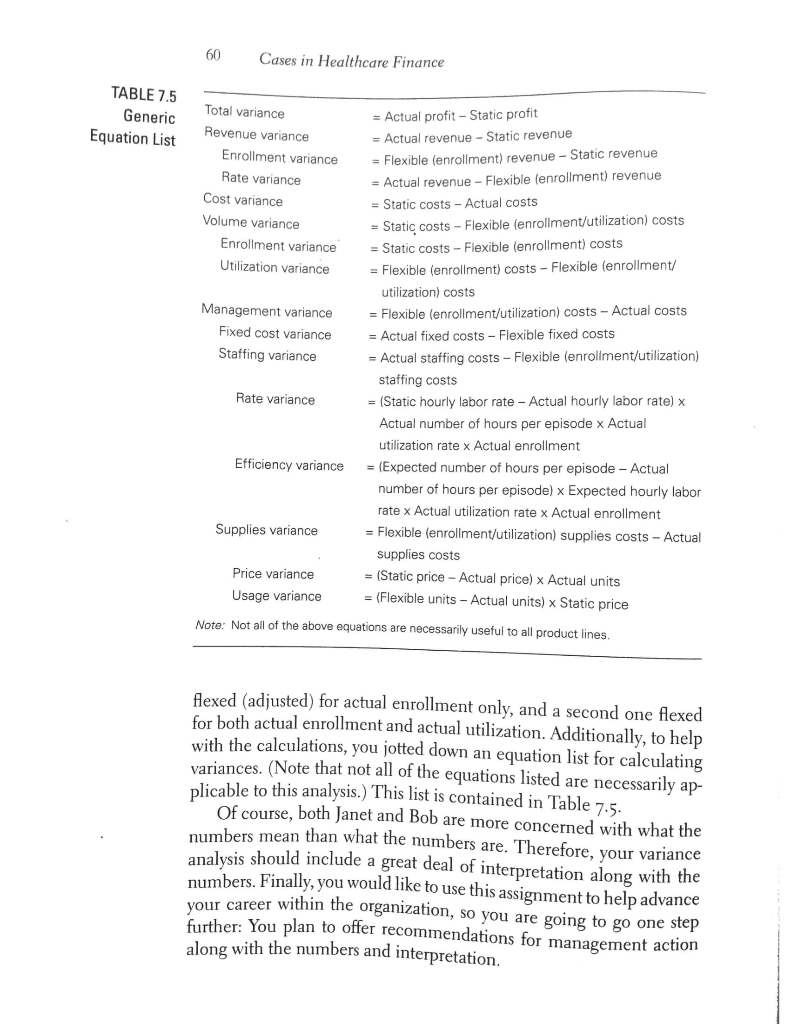

XAVIER MENTAL ** HEALTH VARIANCE ANALYSIS XAVIER MENTAL HEALTH is a not-for-profit, multidisciplinary mental health provider that offers both inpatient and outpatient services on a full-risk (capitated) basis to members of managed care plans. Its clinical staff consists primarily of psychiatrists, psychologists, psychiatric nurses, social workers, and chemical dependency counselors. Currently, Xavier has major contracts with two large managed care organizations in its service area: Physician Care (PC) and Share Healthplans (SH). Each of these organizations has both commercial and Medicare HMO contracts with Xavier. Thus, in total, there are four separate product lines. Xavier is partially funded by state and local governments. The agree- ment with the funding agencies is that funds received would be used to cover overhead and capital expenses. Furthermore, expenses for drugs and other medical and administrative supplies are billed separately to the HMOs at cost. Thus, overhead and supplies expenses are not part of this budget, which means that the analysis focuses on clinical labor expenses. If the assumption is made that other payment mechanisms cover overhead, capital expenses, and supplies at cost, then Xavier's profitability is solely a function of its ability to create revenues that exceed labor costs. Thus, its operating budget focuses on enrollment per member premiums, utilization, and labor costs. Table 7.1 contains the assumptions used to prepare Xavier's 2005 operating budget. Note that the four product lines are expected to pro- vide a total of 4.551,000 member-months of revenue during 2005. Also, note that each product line has a different PMPM payment (premium) 53 54 Cases in Healthcare Finance TABLE 7.1 Xavier Mental Health: 2005 Operating Budget Assumptions Expected Enrollment (Member-Months) PC Commercial PC Medicare SH Commercial SH Medicare Total 3,365,000 469,000 502,000 215,000 4,551,000 Expected Premium Data (per Member per Month) PC Commercial PC Medicare SH Commercial SH Medicare $0.70 0.85 0.75 0.80 Expected Labor Data per Admission or Session Inpatient # of Hours Hourly Rate Outpatient # of Hours Hourly Rate PC Commercial PC Medicare SH Commercial SH Medicare 53.74 68.43 47.77 56.86 1.04 1.30 1.15 1.14 $100 100 100 100 amount. Table 7.1 also contains expected admission (for inpatients), re- ferral rate (for outpatients), and labor cost and utilization data for each product line. Because of the unique employment arrangements between Xavier and its clinical staff, in which the staff are paid on the basis of the number of patient service units provided, clinical labor costs are virtually all variable, and hence costs are not identified as fixed or variable. Table 7.2 contains the forecasted 2005 budget. In essence, data from Table 7.1 are used to forecast revenues and costs, both in the aggregate and by product line. Overall, Xavier expected to earn a profit of $419,379 on these product lines in 2005. During the first quarter of 2005, Xavier's managers noted a higher utilization rate than budgeted. To add to their concern, the monthly Expected Utilization and Total Labor Cost Data Avg. Members fin 000s) Admission Rate Inpatient Cost per Admission Total Costs Referral Rate Outpatient Cost per Session Plen Type PC: Total Costs Total $2,067,966 Commercial Medicare Total 280.417 39.083 319.500 3.81 3.96 $1,881 2,395 $2,009,639 370.671 $2,380,310 2.00 2.00 $104 130 $58.327 10.162 $68,489 380,830 $2,448,799 SH: 2.00 Commercial Medicare Total $115 41.833 17.917 59.750 $1,672 1,990 4.17 $ 272,085 148,681 $ 420.766 2.00 114 $ 9.622 4.088 $13.707 152.766 $ 434,473 Xavier Mental Health Grand total 379.250 $2,801,076 $82, 198 $2.880.272 5 Assumptions TABLE 21 I continued) 2005 Operating Budget Xavier Mental Health 56 Cara in Healthcare Finance TABLE 12 Xavier Mental Health 2005 Operating Budget Expected Product Ine und Appregate Profits SA Total Commern Medicare Commercial Medicare Revenue Costs Profit Margon $2.335,500 $ 398,650 2067 964 380 B36 $ 287 536 17814 123% $376,500 281.709 $ 94,791 25 2% $172.000 152.763 $19.237 11.2% $3.302.650 2,883,271 $ 419,379 12 7% 4 5 % TABLE 73 Xavier Mental Health 2005 Operating Results Actual Enrollment (Member-Months) PC Commercial PC Medicare SH Commercial SH Medicare Total 3,073,133 485,000 547,105 257,000 4,362,238 Actual Premium Deta (per Member per Month PC Commercial PC Medicare SH Commercial SH Medicare $0.75 0.85 0.80 0.80 Actual Labor Data per Admission or Session Inpatient # of Hours Hourly Rate Outpatient # of Hours Hourly Rate $38 PC Commercial PC Medicare SH Commercial SH Medicare $109.50 109.50 0.95 1.15 0.98 2.00 B4.85 33 Actual Utilization and Cost Data Avg # Members (in 000s) Admission Rate Inpatient Cost per Admission Total Costs Referral Rate Outpatient Cost per Session Total Costs Total Plan Type PC: Commercial Medicare Total 256.094 40.417 296.511 4.33 4.68 $1,798 2,229 $104 126 $1,993,782 421,615 $2,415,397 3.65 1.86 $ 97,213 9,472 $106,685 $2,090,996 431,087 $2,522,083 SH: $1,718 2,800 5.79 4.56 45.592 21.417 67.009 Commercial Medicare Total 3.35 1.75 $ 453,514 273,448 $ 726,962 $ 93 $ 14,204 1907.121 $ 21,325 $467,719 280,569 $ 748,288 Xavier Mental Health $128,011 $3,142,360 $3.270,371 363.520 Grand total Note: These data were generated on a spreadsheet, and hence some rounding differences occur 57 TABLE 7.3 2005 Operating Results (continued) Xavier Mental Health: 58 Cases in Healthcare Finance Product Line and Aggregate Profit Results TABLE 7.4 Xavier Mental Health: 2005 Actual P&L Statements PC SH Commercial Medicare Commercial Medicare Total Revenue Costs $2,304,850 $ 412,250 $437,684 $205,600 2,090,996 431,087 467,719 280,569 $ 213,584 $ 18,837) $ 30,035) ($ 74,969) 9.3% (4.6%) (6.9%) (36.5%) $3,360,384 3 ,270,371 $ 90,013 2.7% Profit Margin Note: These data were generated on a spreadsheet, and hence some rounding differences occur. enrollment figures supplied by the contracting managed care plans were less than those budgeted. Together, these trends indicated lower revenues and higher per enrollee costs, and hence lower profits, than forecasted in Table 7.2. These concerns were borne out when the first- quarter profits came in under budget. To help stem the adverse trend, Xavier's managers instituted a utilization management system in which all inpatient stays were required to be approved by the clinic's medi- cal director-a senior staff psychiatrist. In addition, Xavier was able to make mid-year changes to its commercial premiums that increased the average premiums for the year. Unfortunately, the action taken was "too little, too late" to save the year. Table 7.3 contains operating results for 2005, while Table 7.4 con- tains the realized aggregate and product line P&L statements. A quick review of Table 7-4 reveals that the signals conveyed by the first-quarter data were indeed correct; although 2005 ended with a profit, the profit was much less than the amount forecasted. When the results were submitted to Xavier's chief executive officer, Lanet Johnson, she grimaced and said, I knew it was coming, but I did not expect the profits to be so low." It was immediately apparent to Janet that Xavier could not afford similar results in 2006. She knew that something had to be done, but the best course of action was not clear. To help plan for next year, Janet asked Xavier's finance and account- ing department head, Bob Mitchell, to perform a variance analysis on the data to help identify the problems that led to the poor financial results for 2005. Unfortunately, Bob's area of expertise is dealing with Xavier Mental Health 59 Total (Profit) Variance FIGURE 7.1 Variance Analysis Summary Revenue Variance Cost Variance Enrollment Variance Rate Variance Volume Variance Management Variance Enrollment Variance Utilization Variance Fixed Cost Variance Staffing Variance Supplies Variance Efficiency Variance Variance Price Variance Usage Variance Hint: It might be useful to use this figure as the format for presenting your numerical results. lenders and other capital suppliers, so he passed the assignment on to you, a newly hired financial analyst. To start the analysis, you created a diagram (Figure 7.1) to help under- stand variance analysis. (Note that this diagram is generic in nature and has not been "customized for this case.) Furthermore, you recognize that because the volume variance consists of differences in both enroll- ment and utilization, it is necessary to create two flexible budgets: one 60 Cases in Healthcare Finance TABLE 7.5 Generic Equation List Total variance Revenue variance Enrollment variance Rate variance Cost variance Volume variance Enrollment variance Utilization variance Management variance Fixed cost variance Staffing variance = Actual profit - Static profit = Actual revenue - Static revenue = Flexible (enrollment) revenue - Static revenue = Actual revenue - Flexible (enrollment) revenue = Static costs - Actual costs = Static costs - Flexible (enrollment/utilization) costs = Static costs - Flexible (enrollment) costs = Flexible (enrollment) costs - Flexible (enrollment/ utilization) costs = Flexible (enrollment/utilization) costs - Actual costs = Actual fixed costs - Flexible fixed costs = Actual staffing costs - Flexible (enrollment/utilization) staffing costs = (Static hourly labor rate - Actual hourly labor rate) x Actual number of hours per episode x Actual utilization rate x Actual enrollment = (Expected number of hours per episode - Actual number of hours per episode) x Expected hourly labor rate x Actual utilization rate x Actual enrollment = Flexible (enrollment/utilization) supplies costs - Actual supplies costs Rate variance Efficiency variance Supplies variance Price variance Usage variance = (Static price - Actual price) x Actual units = (Flexible units - Actual units) x Static price Note: Not all of the above equations are necessarily useful to all product lines. flexed (adjusted) for actual enrollment only, and a second one flexed for both actual enrollment and actual utilization. Additionally, to help with the calculations, you jotted down an equation list for calculating variances. (Note that not all of the equations listed are necessarily ap- plicable to this analysis.) This list is contained in Table 7.5. Of course, both Janet and Bob are more concerned with what the numbers mean than what the numbers are. Therefore, your variance analysis should include a great deal of interpretation along with the numbers. Finally, you would like to use this assignment to help advance your career within the organization, so you are going to go one step further: You plan to offer recommendations for management action along with the numbers and interpretation. XAVIER MENTAL ** HEALTH VARIANCE ANALYSIS XAVIER MENTAL HEALTH is a not-for-profit, multidisciplinary mental health provider that offers both inpatient and outpatient services on a full-risk (capitated) basis to members of managed care plans. Its clinical staff consists primarily of psychiatrists, psychologists, psychiatric nurses, social workers, and chemical dependency counselors. Currently, Xavier has major contracts with two large managed care organizations in its service area: Physician Care (PC) and Share Healthplans (SH). Each of these organizations has both commercial and Medicare HMO contracts with Xavier. Thus, in total, there are four separate product lines. Xavier is partially funded by state and local governments. The agree- ment with the funding agencies is that funds received would be used to cover overhead and capital expenses. Furthermore, expenses for drugs and other medical and administrative supplies are billed separately to the HMOs at cost. Thus, overhead and supplies expenses are not part of this budget, which means that the analysis focuses on clinical labor expenses. If the assumption is made that other payment mechanisms cover overhead, capital expenses, and supplies at cost, then Xavier's profitability is solely a function of its ability to create revenues that exceed labor costs. Thus, its operating budget focuses on enrollment per member premiums, utilization, and labor costs. Table 7.1 contains the assumptions used to prepare Xavier's 2005 operating budget. Note that the four product lines are expected to pro- vide a total of 4.551,000 member-months of revenue during 2005. Also, note that each product line has a different PMPM payment (premium) 53 54 Cases in Healthcare Finance TABLE 7.1 Xavier Mental Health: 2005 Operating Budget Assumptions Expected Enrollment (Member-Months) PC Commercial PC Medicare SH Commercial SH Medicare Total 3,365,000 469,000 502,000 215,000 4,551,000 Expected Premium Data (per Member per Month) PC Commercial PC Medicare SH Commercial SH Medicare $0.70 0.85 0.75 0.80 Expected Labor Data per Admission or Session Inpatient # of Hours Hourly Rate Outpatient # of Hours Hourly Rate PC Commercial PC Medicare SH Commercial SH Medicare 53.74 68.43 47.77 56.86 1.04 1.30 1.15 1.14 $100 100 100 100 amount. Table 7.1 also contains expected admission (for inpatients), re- ferral rate (for outpatients), and labor cost and utilization data for each product line. Because of the unique employment arrangements between Xavier and its clinical staff, in which the staff are paid on the basis of the number of patient service units provided, clinical labor costs are virtually all variable, and hence costs are not identified as fixed or variable. Table 7.2 contains the forecasted 2005 budget. In essence, data from Table 7.1 are used to forecast revenues and costs, both in the aggregate and by product line. Overall, Xavier expected to earn a profit of $419,379 on these product lines in 2005. During the first quarter of 2005, Xavier's managers noted a higher utilization rate than budgeted. To add to their concern, the monthly Expected Utilization and Total Labor Cost Data Avg. Members fin 000s) Admission Rate Inpatient Cost per Admission Total Costs Referral Rate Outpatient Cost per Session Plen Type PC: Total Costs Total $2,067,966 Commercial Medicare Total 280.417 39.083 319.500 3.81 3.96 $1,881 2,395 $2,009,639 370.671 $2,380,310 2.00 2.00 $104 130 $58.327 10.162 $68,489 380,830 $2,448,799 SH: 2.00 Commercial Medicare Total $115 41.833 17.917 59.750 $1,672 1,990 4.17 $ 272,085 148,681 $ 420.766 2.00 114 $ 9.622 4.088 $13.707 152.766 $ 434,473 Xavier Mental Health Grand total 379.250 $2,801,076 $82, 198 $2.880.272 5 Assumptions TABLE 21 I continued) 2005 Operating Budget Xavier Mental Health 56 Cara in Healthcare Finance TABLE 12 Xavier Mental Health 2005 Operating Budget Expected Product Ine und Appregate Profits SA Total Commern Medicare Commercial Medicare Revenue Costs Profit Margon $2.335,500 $ 398,650 2067 964 380 B36 $ 287 536 17814 123% $376,500 281.709 $ 94,791 25 2% $172.000 152.763 $19.237 11.2% $3.302.650 2,883,271 $ 419,379 12 7% 4 5 % TABLE 73 Xavier Mental Health 2005 Operating Results Actual Enrollment (Member-Months) PC Commercial PC Medicare SH Commercial SH Medicare Total 3,073,133 485,000 547,105 257,000 4,362,238 Actual Premium Deta (per Member per Month PC Commercial PC Medicare SH Commercial SH Medicare $0.75 0.85 0.80 0.80 Actual Labor Data per Admission or Session Inpatient # of Hours Hourly Rate Outpatient # of Hours Hourly Rate $38 PC Commercial PC Medicare SH Commercial SH Medicare $109.50 109.50 0.95 1.15 0.98 2.00 B4.85 33 Actual Utilization and Cost Data Avg # Members (in 000s) Admission Rate Inpatient Cost per Admission Total Costs Referral Rate Outpatient Cost per Session Total Costs Total Plan Type PC: Commercial Medicare Total 256.094 40.417 296.511 4.33 4.68 $1,798 2,229 $104 126 $1,993,782 421,615 $2,415,397 3.65 1.86 $ 97,213 9,472 $106,685 $2,090,996 431,087 $2,522,083 SH: $1,718 2,800 5.79 4.56 45.592 21.417 67.009 Commercial Medicare Total 3.35 1.75 $ 453,514 273,448 $ 726,962 $ 93 $ 14,204 1907.121 $ 21,325 $467,719 280,569 $ 748,288 Xavier Mental Health $128,011 $3,142,360 $3.270,371 363.520 Grand total Note: These data were generated on a spreadsheet, and hence some rounding differences occur 57 TABLE 7.3 2005 Operating Results (continued) Xavier Mental Health: 58 Cases in Healthcare Finance Product Line and Aggregate Profit Results TABLE 7.4 Xavier Mental Health: 2005 Actual P&L Statements PC SH Commercial Medicare Commercial Medicare Total Revenue Costs $2,304,850 $ 412,250 $437,684 $205,600 2,090,996 431,087 467,719 280,569 $ 213,584 $ 18,837) $ 30,035) ($ 74,969) 9.3% (4.6%) (6.9%) (36.5%) $3,360,384 3 ,270,371 $ 90,013 2.7% Profit Margin Note: These data were generated on a spreadsheet, and hence some rounding differences occur. enrollment figures supplied by the contracting managed care plans were less than those budgeted. Together, these trends indicated lower revenues and higher per enrollee costs, and hence lower profits, than forecasted in Table 7.2. These concerns were borne out when the first- quarter profits came in under budget. To help stem the adverse trend, Xavier's managers instituted a utilization management system in which all inpatient stays were required to be approved by the clinic's medi- cal director-a senior staff psychiatrist. In addition, Xavier was able to make mid-year changes to its commercial premiums that increased the average premiums for the year. Unfortunately, the action taken was "too little, too late" to save the year. Table 7.3 contains operating results for 2005, while Table 7.4 con- tains the realized aggregate and product line P&L statements. A quick review of Table 7-4 reveals that the signals conveyed by the first-quarter data were indeed correct; although 2005 ended with a profit, the profit was much less than the amount forecasted. When the results were submitted to Xavier's chief executive officer, Lanet Johnson, she grimaced and said, I knew it was coming, but I did not expect the profits to be so low." It was immediately apparent to Janet that Xavier could not afford similar results in 2006. She knew that something had to be done, but the best course of action was not clear. To help plan for next year, Janet asked Xavier's finance and account- ing department head, Bob Mitchell, to perform a variance analysis on the data to help identify the problems that led to the poor financial results for 2005. Unfortunately, Bob's area of expertise is dealing with Xavier Mental Health 59 Total (Profit) Variance FIGURE 7.1 Variance Analysis Summary Revenue Variance Cost Variance Enrollment Variance Rate Variance Volume Variance Management Variance Enrollment Variance Utilization Variance Fixed Cost Variance Staffing Variance Supplies Variance Efficiency Variance Variance Price Variance Usage Variance Hint: It might be useful to use this figure as the format for presenting your numerical results. lenders and other capital suppliers, so he passed the assignment on to you, a newly hired financial analyst. To start the analysis, you created a diagram (Figure 7.1) to help under- stand variance analysis. (Note that this diagram is generic in nature and has not been "customized for this case.) Furthermore, you recognize that because the volume variance consists of differences in both enroll- ment and utilization, it is necessary to create two flexible budgets: one 60 Cases in Healthcare Finance TABLE 7.5 Generic Equation List Total variance Revenue variance Enrollment variance Rate variance Cost variance Volume variance Enrollment variance Utilization variance Management variance Fixed cost variance Staffing variance = Actual profit - Static profit = Actual revenue - Static revenue = Flexible (enrollment) revenue - Static revenue = Actual revenue - Flexible (enrollment) revenue = Static costs - Actual costs = Static costs - Flexible (enrollment/utilization) costs = Static costs - Flexible (enrollment) costs = Flexible (enrollment) costs - Flexible (enrollment/ utilization) costs = Flexible (enrollment/utilization) costs - Actual costs = Actual fixed costs - Flexible fixed costs = Actual staffing costs - Flexible (enrollment/utilization) staffing costs = (Static hourly labor rate - Actual hourly labor rate) x Actual number of hours per episode x Actual utilization rate x Actual enrollment = (Expected number of hours per episode - Actual number of hours per episode) x Expected hourly labor rate x Actual utilization rate x Actual enrollment = Flexible (enrollment/utilization) supplies costs - Actual supplies costs Rate variance Efficiency variance Supplies variance Price variance Usage variance = (Static price - Actual price) x Actual units = (Flexible units - Actual units) x Static price Note: Not all of the above equations are necessarily useful to all product lines. flexed (adjusted) for actual enrollment only, and a second one flexed for both actual enrollment and actual utilization. Additionally, to help with the calculations, you jotted down an equation list for calculating variances. (Note that not all of the equations listed are necessarily ap- plicable to this analysis.) This list is contained in Table 7.5. Of course, both Janet and Bob are more concerned with what the numbers mean than what the numbers are. Therefore, your variance analysis should include a great deal of interpretation along with the numbers. Finally, you would like to use this assignment to help advance your career within the organization, so you are going to go one step further: You plan to offer recommendations for management action along with the numbers and interpretation