Question

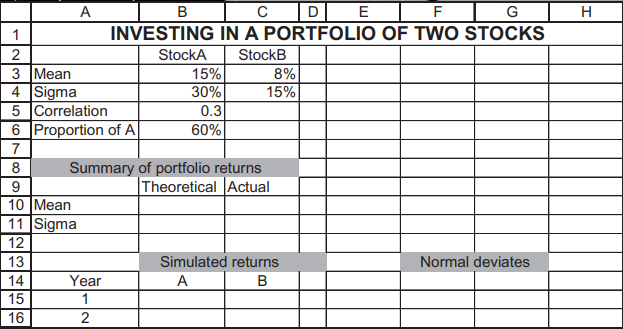

1. Consider a portfolio of two stocks whose statistical parameters are given below. Stock A: Annual mean return = 15%, annual standard deviation of return

1. Consider a portfolio of two stocks whose statistical parameters are given below. Stock A: Annual mean return = 15%, annual standard deviation of return = 30%. Stock B: = 8%, = 15%. Correlation(A,B) = = 0.3 721 An investor with a buy-and-hold strategy buys a portfolio composed of 60% A and 40% B and holds it for 20 years. Simulate the annual returns on the portfolio.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

New Developments Of The Exchange Rate Regimes In Developing Countries

Authors: H. Mitsuo

1st Edition

0230004733,023062555X