Answered step by step

Verified Expert Solution

Question

1 Approved Answer

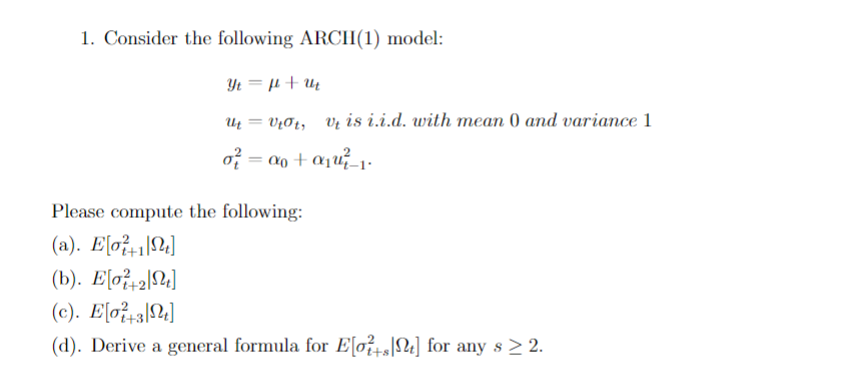

1. Consider the following ARCH(1) model: ut=vot, vt is i.i.d. with mean 0 and variance 1 Please compute the following: (a). E[+] (b). E[+2]

1. Consider the following ARCH(1) model: ut=vot, vt is i.i.d. with mean 0 and variance 1 Please compute the following: (a). E[+] (b). E[+2] (c). E[+] (d). Derive a general formula for E[+] for any s 2.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Analysis and Portfolio Management

Authors: Frank K. Reilly, Keith C. Brown

10th Edition

538482109, 1133711774, 538482389, 9780538482103, 9781133711773, 978-0538482387