Question

1. Consider the partial durations as from the Table 1 below and: a) Estimate the effect of a shift in the yield curve where the

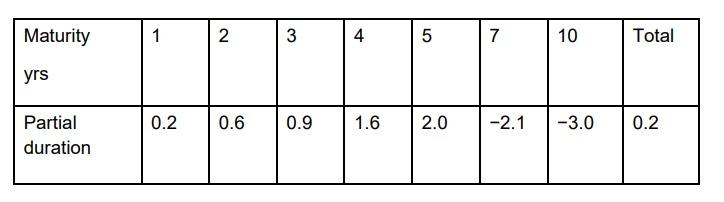

1. Consider the partial durations as from the Table 1 below and:

a) Estimate the effect of a shift in the yield curve where the ten-year rate stays the same, the one-year rate moves up by 9e, and the movements in intermediate rates are calculated by interpolation between 9e and 0. (20 marks)

b) Estimate the percentage change in the portfolio value arising from the rotation? (10 marks)

Maturity yrs Partial duration 1 0.2 2 0.6 3 4 0.9 1.6 5 2.0 7 -2.1 Total 10 -3.0 0.2 Maturity yrs Partial duration 1 0.2 2 0.6 3 4 0.9 1.6 5 2.0 7 -2.1 Total 10 -3.0 0.2Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Developments In Entrepreneurial Finance And Technology

Authors: David B. Audretsch, Maksim Belitski, Nada Rejeb, Rosa Caiazza

1st Edition

1800884338,1800884346