Answered step by step

Verified Expert Solution

Question

1 Approved Answer

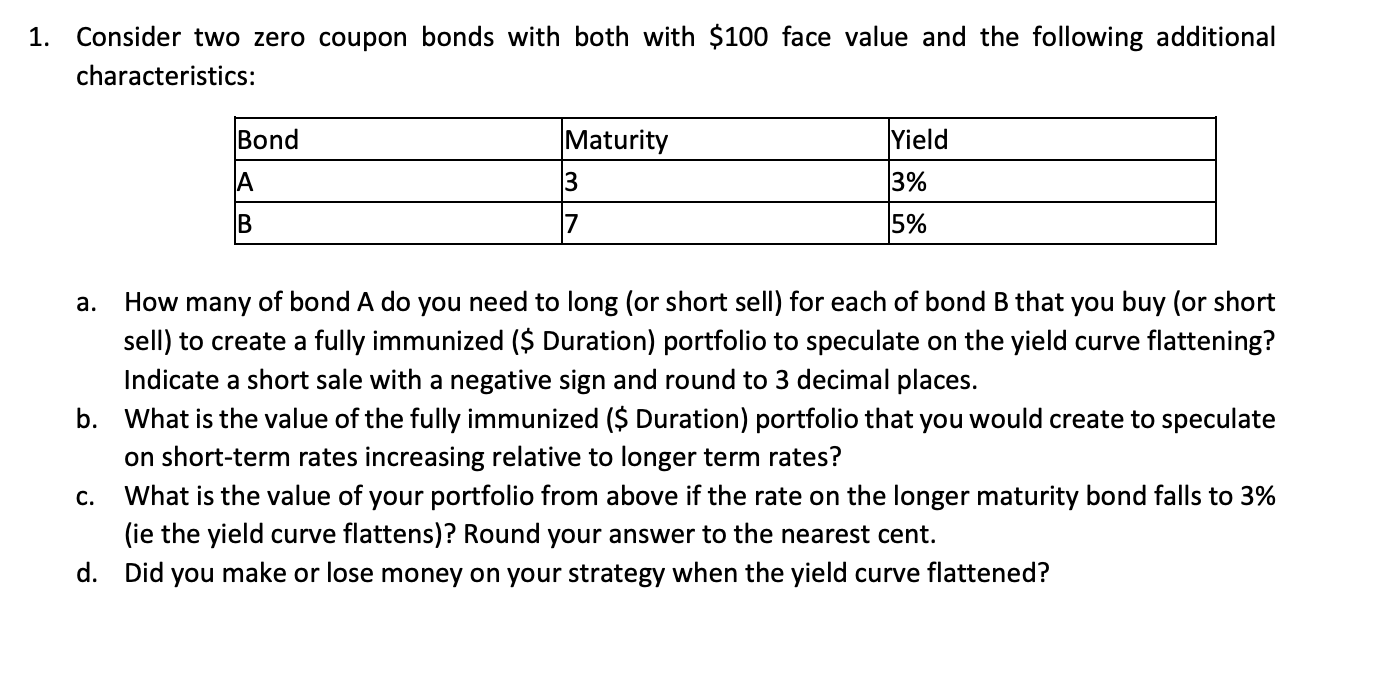

1. Consider two zero coupon bonds with both with $100 face value and the following additional characteristics: Bond A B Maturity 3 7 Yield

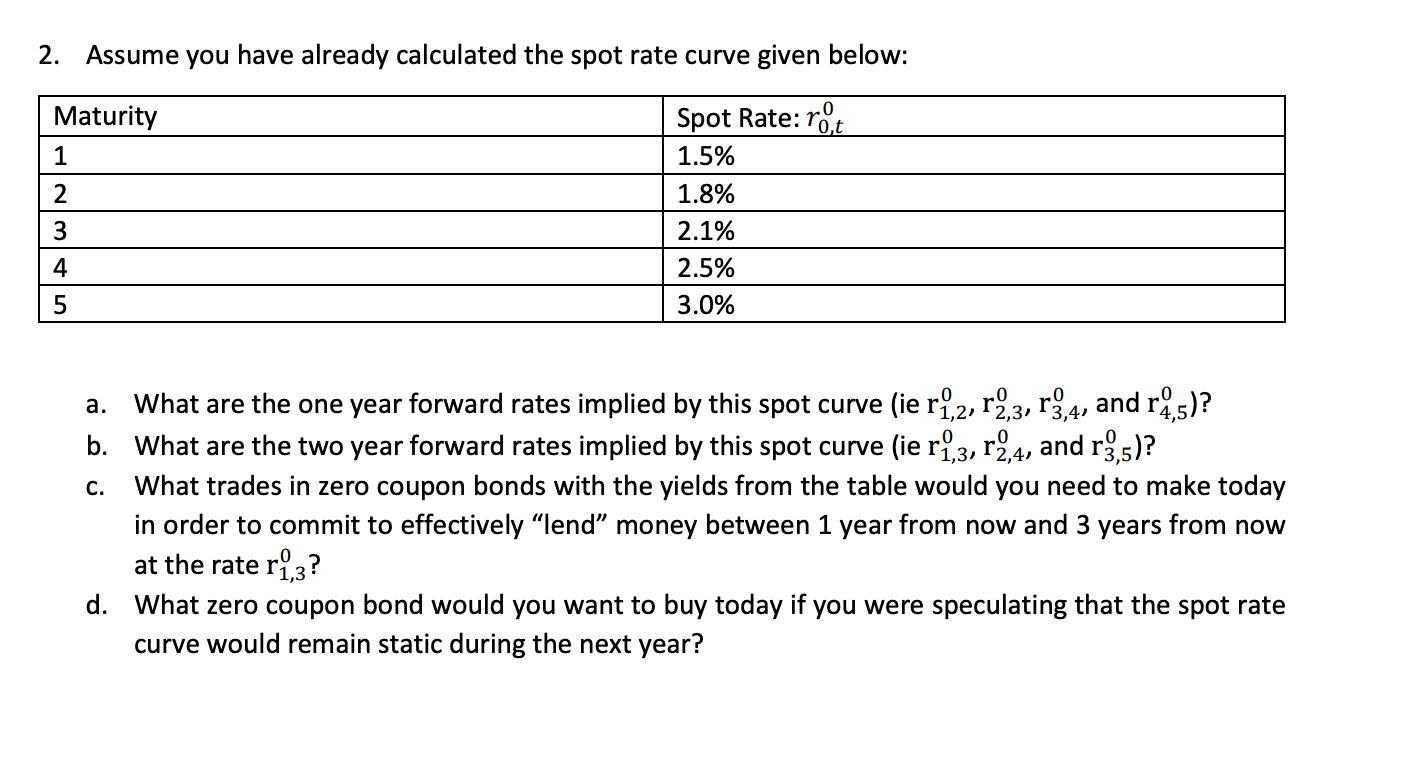

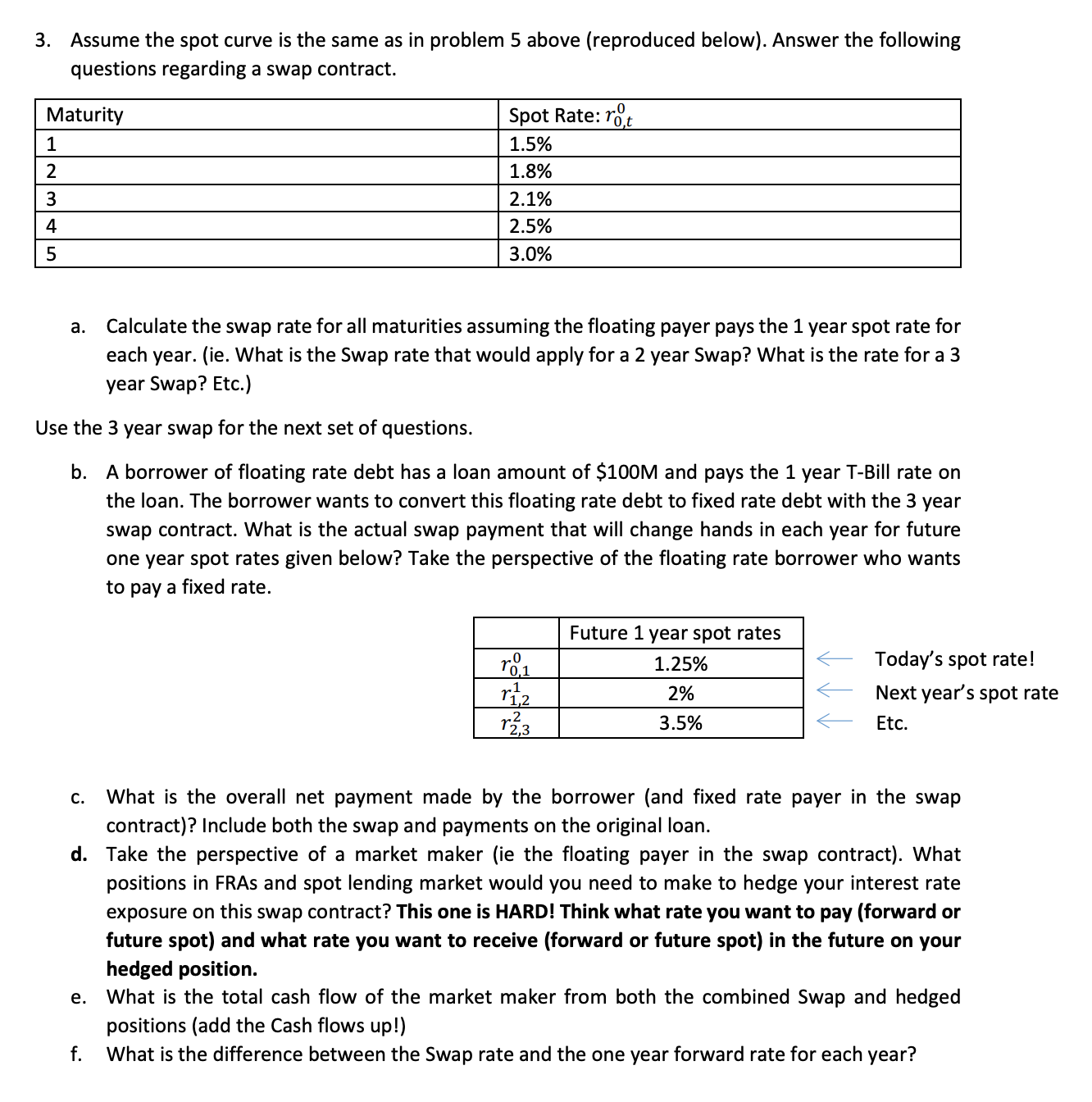

1. Consider two zero coupon bonds with both with $100 face value and the following additional characteristics: Bond A B Maturity 3 7 Yield 3% 5% a. How many of bond A do you need to long (or short sell) for each of bond B that you buy (or short sell) to create a fully immunized ($ Duration) portfolio to speculate on the yield curve flattening? Indicate a short sale with a negative sign and round to 3 decimal places. b. What is the value of the fully immunized ($ Duration) portfolio that you would create to speculate on short-term rates increasing relative to longer term rates? C. What is the value of your portfolio from above if the rate on the longer maturity bond falls to 3% (ie the yield curve flattens)? Round your answer to the nearest cent. d. Did you make or lose money on your strategy when the yield curve flattened? 2. Assume you have already calculated the spot rate curve given below: Maturity 1 2 3 45 Spot Rate: rot 1.5% 1.8% 2.1% 2.5% 3.0% a. What are the one year forward rates implied by this spot curve (ie r,2, r2,3, r3,4, and r4,5)? b. What are the two year forward rates implied by this spot curve (ie r1,3, r2,4, and r3,5)? C. What trades in zero coupon bonds with the yields from the table would you need to make today in order to commit to effectively "lend" money between 1 year from now and 3 years from now at the rate r,3? d. What zero coupon bond would you want to buy today if you were speculating that the spot rate curve would remain static during the next year? 3. Assume the spot curve is the same as in problem 5 above (reproduced below). Answer the following questions regarding a swap contract. Maturity 1 2 3 4 5 Spot Rate: rot .0 1.5% 1.8% 2.1% 2.5% 3.0% a. Calculate the swap rate for all maturities assuming the floating payer pays the 1 year spot rate for each year. (ie. What is the Swap rate that would apply for a 2 year Swap? What is the rate for a 3 year Swap? Etc.) Use the 3 year swap for the next set of questions. b. A borrower of floating rate debt has a loan amount of $100M and pays the 1 year T-Bill rate on the loan. The borrower wants to convert this floating rate debt to fixed rate debt with the 3 year swap contract. What is the actual swap payment that will change hands in each year for future one year spot rates given below? Take the perspective of the floating rate borrower who wants to pay a fixed rate. Future 1 year spot rates .0 r01 1 1,2 2 1.25% 2% 12,3 3.5% Today's spot rate! Next year's spot rate Etc. C. What is the overall net payment made by the borrower (and fixed rate payer in the swap contract)? Include both the swap and payments on the original loan. d. Take the perspective of a market maker (ie the floating payer in the swap contract). What positions in FRAS and spot lending market would you need to make to hedge your interest rate exposure on this swap contract? This one is HARD! Think what rate you want to pay (forward or future spot) and what rate you want to receive (forward or future spot) in the future on your hedged position. e. f. What is the total cash flow of the market maker from both the combined Swap and hedged positions (add the Cash flows up!) What is the difference between the Swap rate and the one year forward rate for each year?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding financial statements

Authors: Lyn M. Fraser, Aileen Ormiston

9th Edition

136086241, 978-0136086246