Question

1. Construct a n = 10n=10-period binomial model for the short-rate, r_{i,j}r i,j . The lattice parameters are: r_{0,0}= 5%r 0,0 =5%, u=1.1u=1.1, d=0.9d=0.9 and

1. Construct a n = 10n=10-period binomial model for the short-rate, r_{i,j}r i,j . The lattice parameters are: r_{0,0}= 5\%r 0,0 =5%, u=1.1u=1.1, d=0.9d=0.9 and q=1-q=1/2q=1q=1/2. This is the same lattice that you constructed in Assignment 5. Assume that the 1-step hazard rate in node (i,j)(i,j) is given by h_{ij} = a b^{j-\frac{i}{2}}h ij =ab j 2 i where a = 0.01a=0.01 and b = 1.01b=1.01. Compute the price of a zero-coupon bond with face value F = 100F=100 and recovery R = 20\%R=20%. Submission Guideline: Give your answer rounded to two decimal places. For example, if you compute the answer to be 73.2367, submit 73.24.

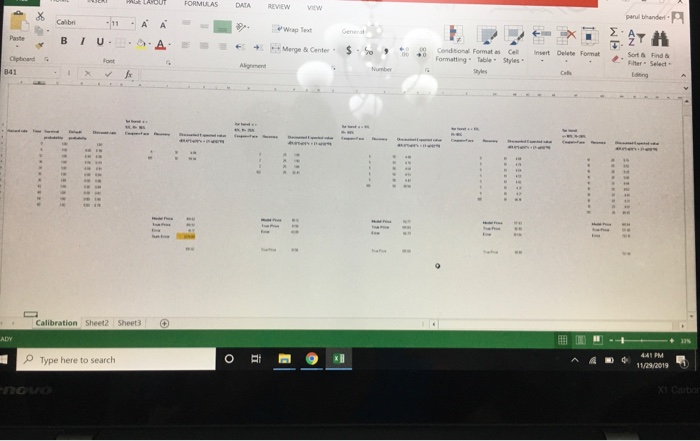

2. The true price of 5 different defaultable coupon paying bonds with non-zero recovery are specified in worksheet Calibration in the workbook Assignment5_cds.xlsx. The interest rate is r = 5\%r=5% per annum. Calibrate the six month hazard rates A6 to A16 to by minimizing the SumError ensuring that the term structure of hazard rates are non-decreasing. You can model the non-decreasing hazard rates by adding constraints of the form A6A7,,A15A16. Report the hazard rate at time 00 as a percentage. Submission Guideline: Give your answer in percent rounded to two decimal places. For example, if you compute the answer to be 73.2367%, submit 73.24.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Finance

Authors: Michael Fardon

1st Edition

1872962319, 1872962173, 978-1872962313, 978-1872962177