Answered step by step

Verified Expert Solution

Question

1 Approved Answer

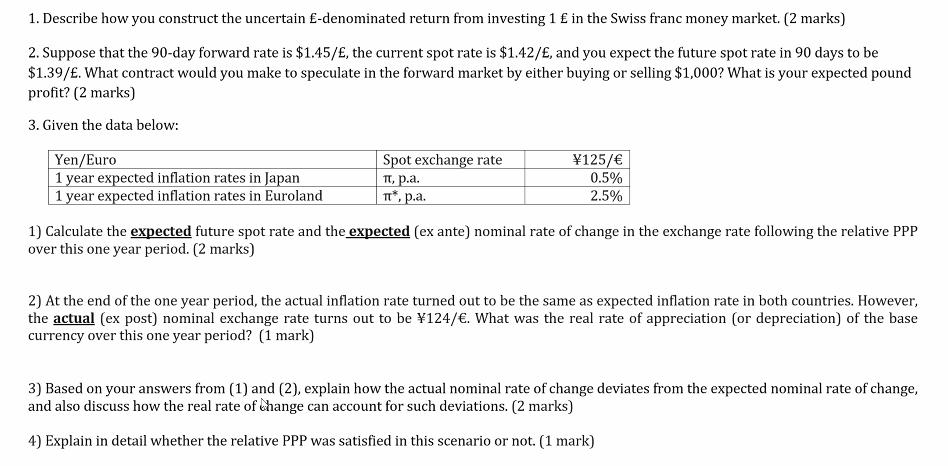

1. Describe how you construct the uncertain -denominated return from investing 1 in the Swiss franc money market. (2 marks) 2. Suppose that the

1. Describe how you construct the uncertain -denominated return from investing 1 in the Swiss franc money market. (2 marks) 2. Suppose that the 90-day forward rate is $1.45/, the current spot rate is $1.42/, and you expect the future spot rate in 90 days to be $1.39/. What contract would you make to speculate in the forward market by either buying or selling $1,000? What is your expected pound profit? (2 marks) 3. Given the data below: Yen/Euro 1 year expected inflation rates in Japan 1 year expected inflation rates in Euroland Spot exchange rate , p.a. *, p.a. 125/ 0.5% 2.5% 1) Calculate the expected future spot rate and the expected (ex ante) nominal rate of change in the exchange rate following the relative PPP over this one year period. (2 marks) 2) At the end of the one year period, the actual inflation rate turned out to be the same as expected inflation rate in both countries. However, the actual (ex post) nominal exchange rate turns out to be 124/. What was the real rate of appreciation (or depreciation) of the base currency over this one year period? (1 mark) 3) Based on your answers from (1) and (2), explain how the actual nominal rate of change deviates from the expected nominal rate of change, and also discuss how the real rate of change can account for such deviations. (2 marks) 4) Explain in detail whether the relative PPP was satisfied in this scenario or not. (1 mark)

Step by Step Solution

★★★★★

3.41 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

1 To construct the uncertain Edenominated return from investing 1 E in the Swiss franc money market you would consider the interest rate offered in the Swiss franc money market Lets assume the annual ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Geert Bekaert, Robert J. Hodrick

2nd edition

013299755X, 132162768, 9780132997553, 978-0132162760