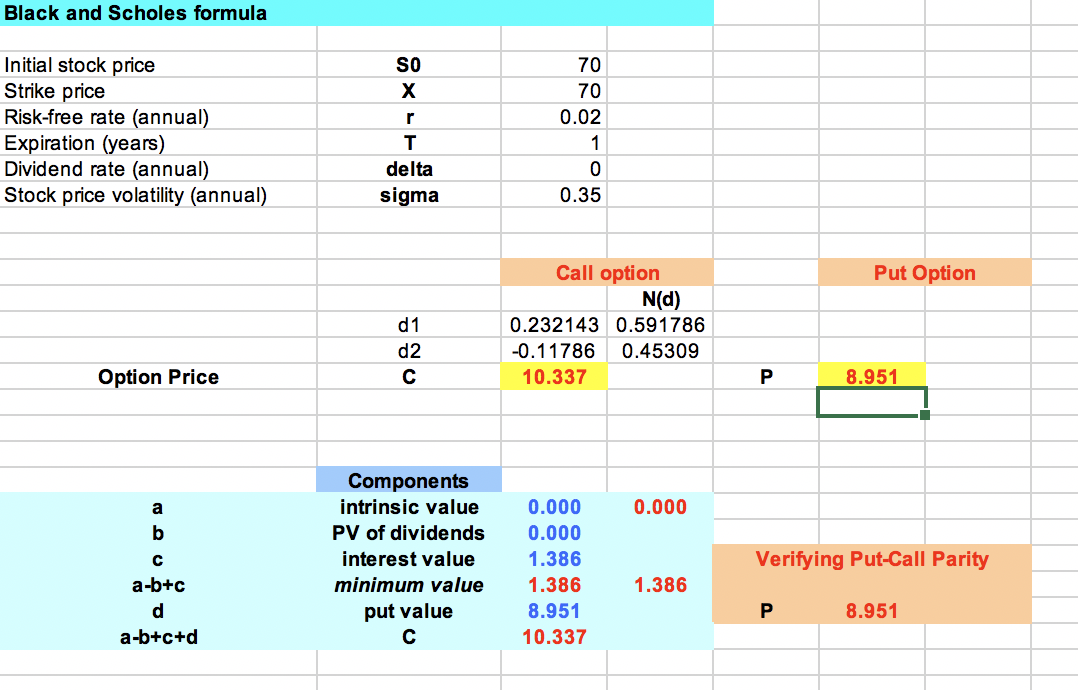

1 Duration 1. A zero coupon bond with 2.5 years to maturity has a annualized yield to maturity of 5%. A 3-year maturity annual-pay coupon bond has as face value of $1000 and a 5% coupon rate. The coupon bond also has a yield to maturity of 5%. Please calculate the duration of each bond. Which bond has the higher duration and why? Using the formula that approximates bond price change as a function of the duration, please calculate the price change of both bonds if yields drop from 5% to 4%. 2 Options 2. Construct profit diagrams at expiration time to show what position in IBM puts, calls and/or underlying stock best expresses the investor's objectives described below. IBM currently sells for $150 so that profit diagrams between $100 and $200 in $10 increments are appropriate. Also assume that at-the-money puts and calls currently cost $20 each. The call with strike $140 costs $25 and the call with strike $160 costs $17. (a) An investor wants to benefit from IBM price drops, but does not want to lose more than $20 on the investment. (b) An investor wants to capture profits if IBM price declines and losses if IBM price increases. The investor wants to break even if IBM price does not change. (c) An investor wants to bet that the upcoming IBM earnings announcement is very close to market expectationsmeaning that the price will not move by more than $10 dollars. 3. Excel Question. Use the Black and Scholes file posted on the class website. Current stock price is So = 70, the annual stock volatility is o = 35%, and the annual dividend yield is 8 = 0. The current risk-free interest rate is r = .01 = 1%. (a) Calculate the Black-Scholes prices of call options with strike K = 70 and maturity of 1, 2, 5, 10, 50, and 100 years. What will happen to call option prices as the time to maturity keeps increasing? (b) Keeping every other parameter constant, suppose the dividend yield is now d = 0.01 = 1%. Again calculate call option prices for strike K = 70 at the above maturities. What happens to option prices as time to maturity increases? (c) What accounts for the difference between (a) and (b)? Black and Scholes formula SO 70 70 0.02 Initial stock price Strike price Risk-free rate (annual) Expiration (years) Dividend rate (annual) Stock price volatility (annual) T delta sigma 0 0.35 Put Option d1 Call option N(d) 0.232143 0.591786 -0.11786 0.45309 10.337 d2 Option Price 8.951 0.000 Components intrinsic value PV of dividends interest value minimum value put value Verifying Put-Call Parity 0.000 0.000 1.386 1.386 8.951 10.337 a-b+c 1.386 8.951 a-b+c+d