Answered step by step

Verified Expert Solution

Question

1 Approved Answer

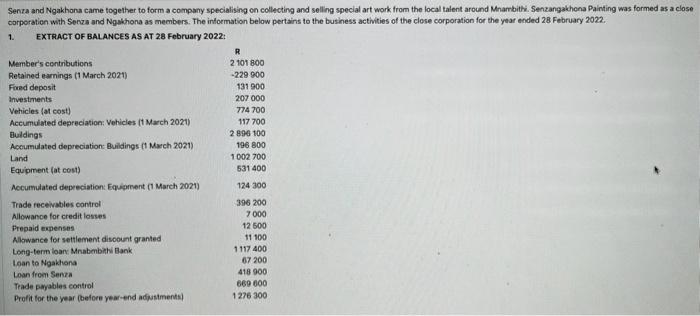

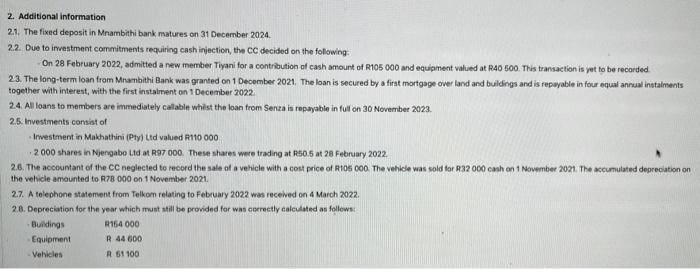

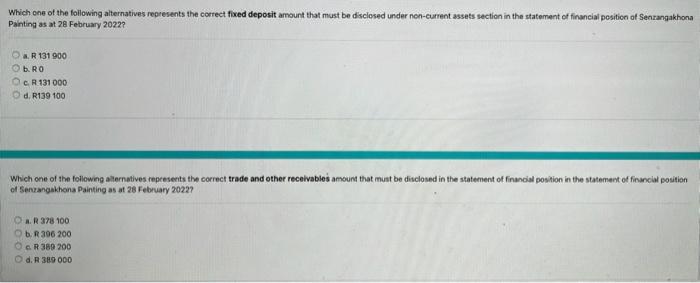

1. EXTRACT OF BALANCES AS AT 28 February 2022: 2.1. The fixed deposit in Mnambithi bank matures on 31 December 2024. 2.2. Due to irwestment

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting The Theoretical And Regulatory Framework

Authors: D A V I D Alexander

2nd Edition

0412357909, 978-0412357909