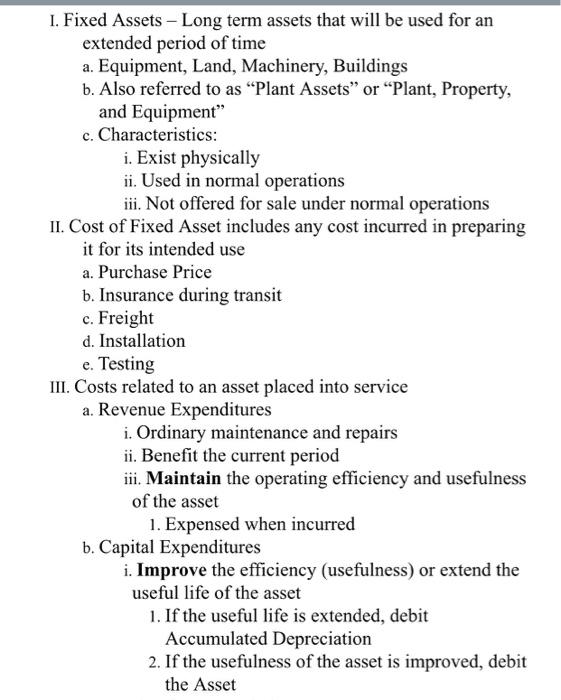

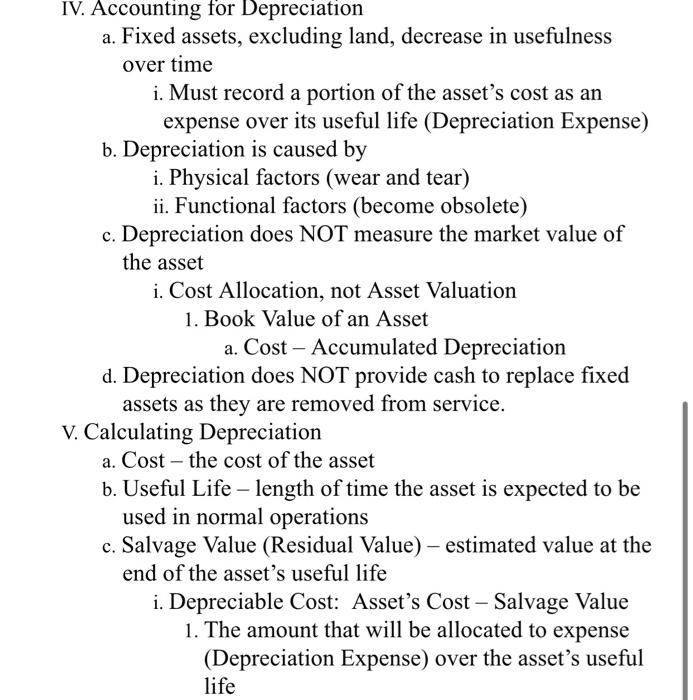

1. Fixed Assets Long term assets that will be used for an extended period of time a. Equipment, Land, Machinery, Buildings b. Also referred to as Plant Assets or Plant, Property, and Equipment c. Characteristics: i. Exist physically ii. Used in normal operations iii. Not offered for sale under normal operations II. Cost of Fixed Asset includes any cost incurred in preparing it for its intended use a. Purchase Price b. Insurance during transit c. Freight d. Installation e. Testing III. Costs related to an asset placed into service a. Revenue Expenditures i. Ordinary maintenance and repairs ii. Benefit the current period iii. Maintain the operating efficiency and usefulness of the asset 1. Expensed when incurred b. Capital Expenditures i. Improve the efficiency (usefulness) or extend the useful life of the asset 1. If the useful life is extended, debit Accumulated Depreciation 2. If the usefulness of the asset is improved, debit the Asset IV. Accounting for Depreciation a. Fixed assets, excluding land, decrease in usefulness over time i. Must record a portion of the asset's cost as an expense over its useful life (Depreciation Expense) b. Depreciation is caused by i. Physical factors (wear and tear) ii. Functional factors (become obsolete) c. Depreciation does NOT measure the market value of the asset i. Cost Allocation, not Asset Valuation 1. Book Value of an Asset a. Cost - Accumulated Depreciation d. Depreciation does NOT provide cash to replace fixed assets as they are removed from service. V. Calculating Depreciation Cost - the cost of the asset b. Useful Life - length of time the asset is expected to be used in normal operations c. Salvage Value (Residual Value) - estimated value at the end of the asset's useful life i. Depreciable Cost: Asset's Cost - Salvage Value 1. The amount that will be allocated to expense (Depreciation Expense) over the asset's useful life 1. Fixed Assets Long term assets that will be used for an extended period of time a. Equipment, Land, Machinery, Buildings b. Also referred to as Plant Assets or Plant, Property, and Equipment c. Characteristics: i. Exist physically ii. Used in normal operations iii. Not offered for sale under normal operations II. Cost of Fixed Asset includes any cost incurred in preparing it for its intended use a. Purchase Price b. Insurance during transit c. Freight d. Installation e. Testing III. Costs related to an asset placed into service a. Revenue Expenditures i. Ordinary maintenance and repairs ii. Benefit the current period iii. Maintain the operating efficiency and usefulness of the asset 1. Expensed when incurred b. Capital Expenditures i. Improve the efficiency (usefulness) or extend the useful life of the asset 1. If the useful life is extended, debit Accumulated Depreciation 2. If the usefulness of the asset is improved, debit the Asset IV. Accounting for Depreciation a. Fixed assets, excluding land, decrease in usefulness over time i. Must record a portion of the asset's cost as an expense over its useful life (Depreciation Expense) b. Depreciation is caused by i. Physical factors (wear and tear) ii. Functional factors (become obsolete) c. Depreciation does NOT measure the market value of the asset i. Cost Allocation, not Asset Valuation 1. Book Value of an Asset a. Cost - Accumulated Depreciation d. Depreciation does NOT provide cash to replace fixed assets as they are removed from service. V. Calculating Depreciation Cost - the cost of the asset b. Useful Life - length of time the asset is expected to be used in normal operations c. Salvage Value (Residual Value) - estimated value at the end of the asset's useful life i. Depreciable Cost: Asset's Cost - Salvage Value 1. The amount that will be allocated to expense (Depreciation Expense) over the asset's useful life