Question

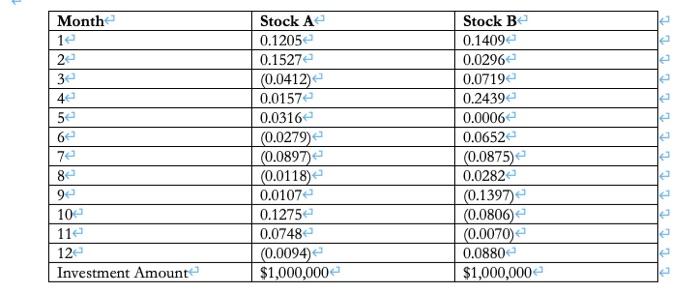

1. From the following monthly returns from stocks A & B and the investment amounts, calculate their average returns, standard deviations, portfolio weighting, and the

1. From the following monthly returns from stocks A & B and the investment amounts, calculate their average returns, standard deviations, portfolio weighting, and the correlation coefficient between stocks A & B. Then calculate the portfolio return and variance from a portfolio of stocks A & B with the given investment amounts. What can say about the portfolio ?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Housing Finance

Authors: Peter King

2nd Edition

0415432952, 978-0415432955