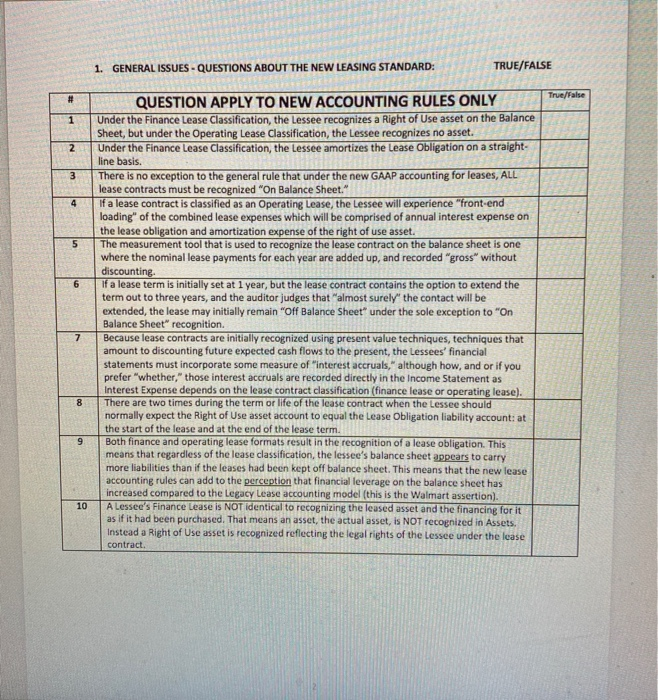

1. GENERAL ISSUES - QUESTIONS ABOUT THE NEW LEASING STANDARD: TRUE/FALSE # True/False 1 2 3 4 5 6 QUESTION APPLY TO NEW ACCOUNTING RULES ONLY Under the Finance Lease Classification, the Lessee recognizes a Right of Use asset on the Balance Sheet, but under the Operating Lease Classification, the Lessee recognizes no asset. Under the Finance Lease Classification, the lessee amortizes the Lease Obligation on a straight- line basis. There is no exception to the general rule that under the new GAAP accounting for leases, ALL lease contracts must be recognized "On Balance Sheet." If a lease contract is classified as an Operating Lease, the Lessee will experience "front-end loading" of the combined lease expenses which will be comprised of annual interest expense on the lease obligation and amortization expense of the right of use asset. The measurement tool that is used to recognize the lease contract on the balance sheet is one where the nominal lease payments for each year are added up, and recorded "gross" without discounting If a lease term is initially set at 1 year, but the lease contract contains the option to extend the term out to three years, and the auditor judges that almost surely" the contact will be extended, the lease may initially remain "Off Balance Sheet" under the sole exception to "On Balance Sheet" recognition. Because lease contracts are initially recognized using present value techniques, techniques that amount to discounting future expected cash flows to the present, the lessees' financial statements must incorporate some measure of "interest accruals," although how, and or if you prefer "whether," those interest accruals are recorded directly in the Income Statement as Interest Expense depends on the lease contract classification (finance lease or operating lease). There are two times during the term or life of the lease contract when the Lessee should normally expect the Right of Use asset account to equal the Lease Obligation liability account: at the start of the lease and at the end of the lease term. Both finance and operating lease formats result in the recognition of a lease obligation. This means that regardless of the lease classification, the lessee's balance sheet appears to carry more liabilities than if the leases had been kept off balance sheet. This means that the new lease accounting rules can add to the perception that financial leverage on the balance sheet has increased compared to the Legacy Lease accounting model (this is the Walmart assertion) A Lessee's Finance Lease is NOT identical to recognizing the leased asset and the financing for it as if it had been purchased. That means an asset, the actual asset, is NOT recognized in Assets. Instead a Right of Use asset is recognized reflecting the legal rights of the Lessee under the lease contract. 7 8 9 10