Question

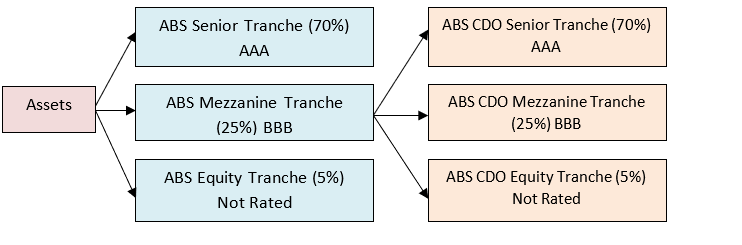

1. Given the ABS & ABS CDO shown below, what is the minimum loss on the portfolio of underlying assets when: a) Senior ABS tranche

1. Given the ABS & ABS CDO shown below, what is the minimum loss on the portfolio of underlying assets when:

a) Senior ABS tranche a 50% has loss of principal?

b) Equity ABS CDO tranche has a 100% loss of principal?

c) Mezzanine ABS CDO tranche has a 100% loss of principal?

d) Senior ABS CDO tranche has a 50% loss of principal?

e) Senior ABS CDO tranche has a 100% loss of principal?

f) Why is it likely that the AAA-rated tranche of this ABS CDO is more risky than the AAA-rated tranche of the ABS?

g) Why are the risks in ABS CDOs misjudged by the market? What did we learn about this in 2007?

Please provide step-by-step work to answer this problem, thank you. **

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management for Public Health and Not for Profit Organizations

Authors: Steven A. Finkler, Thad Calabrese

4th edition

133060411, 132805669, 9780133060416, 978-0132805667