Answered step by step

Verified Expert Solution

Question

1 Approved Answer

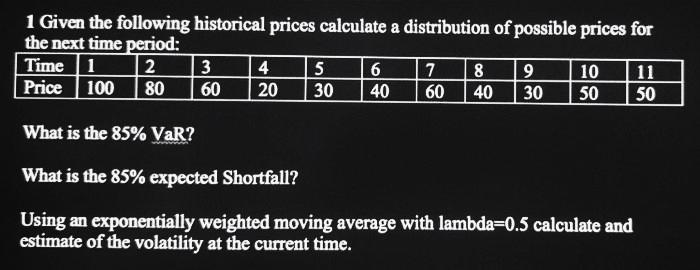

1 Given the following historical prices calculate a distribution of possible prices for the next time period: Time 1 2 Price 100 What is

1 Given the following historical prices calculate a distribution of possible prices for the next time period: Time 1 2 Price 100 What is the 85% VaR? What is the 85% expected Shortfall? Using an exponentially weighted moving average with lambda=0.5 calculate and estimate of the volatility at the current time. 80 3 60 4 20 5 30 6 40 60 7 89 40 30 10 11 50 50

Step by Step Solution

★★★★★

3.45 Rating (171 Votes )

There are 3 Steps involved in it

Step: 1

FREQUNCY 201 60 50 4...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction to the Mathematics of financial Derivatives

Authors: Salih N. Neftci

2nd Edition

978-0125153928, 9780080478647, 125153929, 978-0123846822