Question

1. i. Regarding the divisions 2021 financial year budget information and the related workings presented by the financial manager, draft a report (2 format marks)

1. i. Regarding the divisions 2021 financial year budget information and the related workings presented by the financial manager, draft a report (2 format marks) wherein you:

a. Identify any four principle errors in the provided information and the related working papers. Furthermore, provide a reason why you deem each identified.

b. Provide all the correct workings where applicable (only for the provided information and the related working papers).

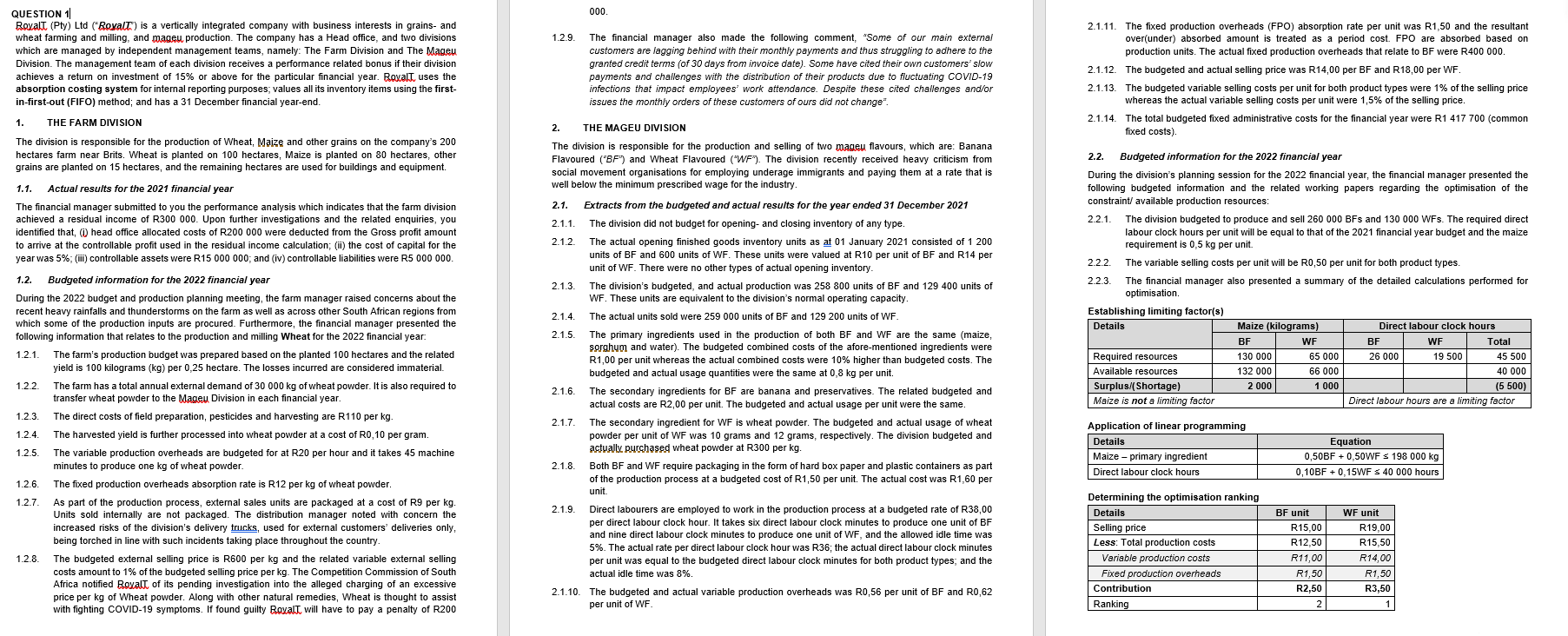

000. 1.2.9. The financial manager also made the following comment, "Some of our main external customers are lagging behind with their monthly payments and thus struggling to adhere to the granted credit terms (of 30 days from invoice date). Some have cited their own customers' slow payments and challenges with the distribution of their products due to fluctuating COVID-19 infections that impact employees' work attendance. Despite these cited challenges and/or issues the monthly orders of these customers of ours did not change". 1. QUESTION 11 Roxalt (Pty) Ltd ("Royalt") is a vertically integrated company with business interests in grains- and wheat farming and milling, and mageu production. The company has a Head office, and two divisions which are managed by independent management teams, namely: The Farm Division and The Mageu Division. The management team of each division receives a performance related bonus if their division achieves a return on investment of 15% or above for the particular financial year. Roxalt uses the absorption costing system for internal reporting purposes, values all its inventory items using the first- in-first-out (FIFO) method; and has a 31 December financial year-end. 1. THE FARM DIVISION The division is responsible for the production of Wheat, Maize and other grains on the company's 200 hectares farm near Brits. Wheat is planted on 100 hectares, Maize is planted on 80 hectares, other grains are planted on 15 hectares, and the remaining hectares are used for buildings and equipment. 1.1. Actual results for the 2021 financial year The financial manager submitted to you the performance analysis which indicates that the farm division achieved a residual income of R300 000. Upon further investigations and the related enquiries, you identified that, ( head office allocated costs of R200 000 were deducted from the Gross profit amount to arrive at the controllable profit used in the residual income calculation; (ii) the cost of capital for the year was 5%; (ii) controllable assets were R15 000 000; and (iv) controllable liabilities were R5 000 000 1.2. . Budgeted information for the 2022 financial year During the 2022 budget and production planning meeting, the farm manager raised concerns about the recent heavy rainfalls and thunderstorms on the farm as well as across other South African regions from which some of the production inputs are procured. Furthermore, the financial manager presented the following information that relates to the production and milling Wheat for the 2022 financial year. 1.2.1. The farm's production budget was prepared based on the planted 100 hectares and the related yield is 100 kilograms (kg) per 0,25 hectare. The losses incurred are considered immaterial. 1.2.2 The farm has a total annual external demand of 30 000 kg of wheat powder. It is also required to transfer wheat powder to the Mageu Division in each financial year. 1.2.3. The direct costs of field preparation, pesticides and harvesting are R110 per kg. 1.2.4. The harvested yield is further processed into wheat powder at a cost of R0,10 per gram. 1.2.5. The variable production overheads are budgeted for at R20 per hour and it takes 45 machine minutes to produce one kg of wheat powder. 1.2.6 The fixed production overheads absorption rate is R12 per kg of wheat powder. 1.2.7 As part of the production process, external sales units are packaged at a cost of R9 per kg. Units sold internally are not packaged. The distribution manager noted with concern the increased risks of the division's delivery trucks, used for external customers' deliveries only, being torched in line with such incidents taking place throughout the country. 1.2.8. The budgeted external selling price is R600 per kg and the related variable exter selling costs amount to 1% of the budgeted selling price per kg. The Competition Commission of South Africa notified Roxalt of its pending investigation into the alleged charging of an excessive price per kg of Wheat powder. Along with other natural remedies, Wheat is thought to assist with fighting COVID-19 symptoms. If found guilty Royalt will have to pay a penalty of R200 2. THE MAGEU DIVISION The division is responsible for the production and selling of two mageu flavours, which are: Banana Flavoured ("BF) and Wheat Flavoured ("WF"). The division recently received heavy criticism from social movement organisations for employing underage immigrants and paying them at a rate that is well below the minimum prescribed wage for the industry. 2.1. Extracts from the budgeted and actual results for the year ended 31 December 2021 2.1.1. The division did not budget for opening and closing inventory of any type. 2.1.2. The actual opening finished goods inventory units as at 01 January 2021 consisted of 1 200 units of BF and 600 units of WF. These units were valued at R10 per unit of BF and R14 per unit of WF. There were no other types of actual opening inventory 2.1.3. The division's budgeted, and actual production was 258 800 units of BF and 129 400 units of WF. These units are equivalent to the division's normal operating capacity. 2.1.4. The actual units sold were 259 000 units of BF and 129 200 units of WF. 2.1.5. The primary ingredients used in the production of both BF and WF are the same (maize, sorghum and water). The budgeted combined costs of the afore-mentioned ingredients were R1,00 per unit whereas the actual combined costs were 10% higher than budgeted costs. The budgeted and actual usage quantities were the same at 0,8 kg per unit. 2.1.6. The secondary ingredients for BF are banana and preservatives. The related budgeted and actual costs are R2,00 per unit. The budgeted and actual usage per unit were the same 2.1.7. The secondary ingredient for WF is wheat powder. The budgeted and actual usage of wheat powder per unit of WF was 10 grams and 12 grams, respectively. The division budgeted and actually purchased wheat powder at R300 per kg. 2.1.8. Both BF and WF require packaging in the form of hard box paper and plastic containers as part of the production process at a budgeted cost of R1,50 per unit. The actual cost was R1,60 per unit. 2.1.9. Direct labourers are employed to work in the production process at a budgeted rate of R38,00 per direct labour clock hour. It takes six direct labour clock minutes to produce one unit of BF and nine direct labour clock minutes to produce one unit of WF, and the allowed idle time was 5%. The actual rate per direct labour clock hour was R36; the actual direct labour clock minutes per unit was equal to the budgeted direct labour clock minutes for both product types, and the actual idle time was 8%. 2.1.10. The budgeted and actual variable production overheads was R0,56 per unit of BF and R0,62 per unit of WF 2.1.11. The fixed production overheads (FPO) absorption rate per unit was R1,50 and the resultant over(under) absorbed amount is treated as a period cost. FPO are absorbed based on production units. The actual fixed production overheads that relate to BF were R400 000. 2.1.12. The budgeted and actual selling price was R14,00 per BF and R18,00 per WF 2.1.13. The budgeted variable selling costs per unit for both product types were 1% of the selling price whereas the actual variable selling costs per unit were 1,5% of the selling price. 2.1.14 The total budgeted fixed administrative costs for the financial year were R1 417 700 (common fixed costs). 2.2. Budgeted information for the 2022 financial year During the division's planning session for the 2022 financial year, the financial manager presented the following budgeted information and the related working papers regarding the optimisation of the constraint/ available production resources: 2.2.1. The division budgeted to produce and sell 260 000 BFs and 130 000 WFs. The required direct labour clock hours per unit will be equal to that of the 2021 financial year budget and the maize requirement is 0,5 kg per unit. 2.2.2. The variable selling costs per unit will be R0,50 per unit for both product types. 2.2.3 The financial manager also presented a summary of the detailed calculations performed for optimisation Establishing limiting factor(s) Details Maize (kilograms) Direct labour clock hours BF WF BF WF Total Required resources 130 000 65 000 26 000 19 500 45 500 Available resources 132 000 66 000 40 000 Surplus/ Shortage) 2 000 1 000 (5 500) Maize is not a limiting factor Direct labour hours are a limiting factor Application of linear programming Details Maize - primary ingredient Direct labour clock hours Equation 0,50BF +0,50WF S 198 000 kg 0,10BF +0,15WF $ 40 000 hours WF unit R19.00 R15.50 Determining the optimisation ranking Details Selling price Less: Total production costs Variable production costs Fixed production overheads Contribution Ranking BF unit R15,00 R12,50 R11,00 R1,50 R2,50 2 R 14,00 R1,50 R3,50 1 000. 1.2.9. The financial manager also made the following comment, "Some of our main external customers are lagging behind with their monthly payments and thus struggling to adhere to the granted credit terms (of 30 days from invoice date). Some have cited their own customers' slow payments and challenges with the distribution of their products due to fluctuating COVID-19 infections that impact employees' work attendance. Despite these cited challenges and/or issues the monthly orders of these customers of ours did not change". 1. QUESTION 11 Roxalt (Pty) Ltd ("Royalt") is a vertically integrated company with business interests in grains- and wheat farming and milling, and mageu production. The company has a Head office, and two divisions which are managed by independent management teams, namely: The Farm Division and The Mageu Division. The management team of each division receives a performance related bonus if their division achieves a return on investment of 15% or above for the particular financial year. Roxalt uses the absorption costing system for internal reporting purposes, values all its inventory items using the first- in-first-out (FIFO) method; and has a 31 December financial year-end. 1. THE FARM DIVISION The division is responsible for the production of Wheat, Maize and other grains on the company's 200 hectares farm near Brits. Wheat is planted on 100 hectares, Maize is planted on 80 hectares, other grains are planted on 15 hectares, and the remaining hectares are used for buildings and equipment. 1.1. Actual results for the 2021 financial year The financial manager submitted to you the performance analysis which indicates that the farm division achieved a residual income of R300 000. Upon further investigations and the related enquiries, you identified that, ( head office allocated costs of R200 000 were deducted from the Gross profit amount to arrive at the controllable profit used in the residual income calculation; (ii) the cost of capital for the year was 5%; (ii) controllable assets were R15 000 000; and (iv) controllable liabilities were R5 000 000 1.2. . Budgeted information for the 2022 financial year During the 2022 budget and production planning meeting, the farm manager raised concerns about the recent heavy rainfalls and thunderstorms on the farm as well as across other South African regions from which some of the production inputs are procured. Furthermore, the financial manager presented the following information that relates to the production and milling Wheat for the 2022 financial year. 1.2.1. The farm's production budget was prepared based on the planted 100 hectares and the related yield is 100 kilograms (kg) per 0,25 hectare. The losses incurred are considered immaterial. 1.2.2 The farm has a total annual external demand of 30 000 kg of wheat powder. It is also required to transfer wheat powder to the Mageu Division in each financial year. 1.2.3. The direct costs of field preparation, pesticides and harvesting are R110 per kg. 1.2.4. The harvested yield is further processed into wheat powder at a cost of R0,10 per gram. 1.2.5. The variable production overheads are budgeted for at R20 per hour and it takes 45 machine minutes to produce one kg of wheat powder. 1.2.6 The fixed production overheads absorption rate is R12 per kg of wheat powder. 1.2.7 As part of the production process, external sales units are packaged at a cost of R9 per kg. Units sold internally are not packaged. The distribution manager noted with concern the increased risks of the division's delivery trucks, used for external customers' deliveries only, being torched in line with such incidents taking place throughout the country. 1.2.8. The budgeted external selling price is R600 per kg and the related variable exter selling costs amount to 1% of the budgeted selling price per kg. The Competition Commission of South Africa notified Roxalt of its pending investigation into the alleged charging of an excessive price per kg of Wheat powder. Along with other natural remedies, Wheat is thought to assist with fighting COVID-19 symptoms. If found guilty Royalt will have to pay a penalty of R200 2. THE MAGEU DIVISION The division is responsible for the production and selling of two mageu flavours, which are: Banana Flavoured ("BF) and Wheat Flavoured ("WF"). The division recently received heavy criticism from social movement organisations for employing underage immigrants and paying them at a rate that is well below the minimum prescribed wage for the industry. 2.1. Extracts from the budgeted and actual results for the year ended 31 December 2021 2.1.1. The division did not budget for opening and closing inventory of any type. 2.1.2. The actual opening finished goods inventory units as at 01 January 2021 consisted of 1 200 units of BF and 600 units of WF. These units were valued at R10 per unit of BF and R14 per unit of WF. There were no other types of actual opening inventory 2.1.3. The division's budgeted, and actual production was 258 800 units of BF and 129 400 units of WF. These units are equivalent to the division's normal operating capacity. 2.1.4. The actual units sold were 259 000 units of BF and 129 200 units of WF. 2.1.5. The primary ingredients used in the production of both BF and WF are the same (maize, sorghum and water). The budgeted combined costs of the afore-mentioned ingredients were R1,00 per unit whereas the actual combined costs were 10% higher than budgeted costs. The budgeted and actual usage quantities were the same at 0,8 kg per unit. 2.1.6. The secondary ingredients for BF are banana and preservatives. The related budgeted and actual costs are R2,00 per unit. The budgeted and actual usage per unit were the same 2.1.7. The secondary ingredient for WF is wheat powder. The budgeted and actual usage of wheat powder per unit of WF was 10 grams and 12 grams, respectively. The division budgeted and actually purchased wheat powder at R300 per kg. 2.1.8. Both BF and WF require packaging in the form of hard box paper and plastic containers as part of the production process at a budgeted cost of R1,50 per unit. The actual cost was R1,60 per unit. 2.1.9. Direct labourers are employed to work in the production process at a budgeted rate of R38,00 per direct labour clock hour. It takes six direct labour clock minutes to produce one unit of BF and nine direct labour clock minutes to produce one unit of WF, and the allowed idle time was 5%. The actual rate per direct labour clock hour was R36; the actual direct labour clock minutes per unit was equal to the budgeted direct labour clock minutes for both product types, and the actual idle time was 8%. 2.1.10. The budgeted and actual variable production overheads was R0,56 per unit of BF and R0,62 per unit of WF 2.1.11. The fixed production overheads (FPO) absorption rate per unit was R1,50 and the resultant over(under) absorbed amount is treated as a period cost. FPO are absorbed based on production units. The actual fixed production overheads that relate to BF were R400 000. 2.1.12. The budgeted and actual selling price was R14,00 per BF and R18,00 per WF 2.1.13. The budgeted variable selling costs per unit for both product types were 1% of the selling price whereas the actual variable selling costs per unit were 1,5% of the selling price. 2.1.14 The total budgeted fixed administrative costs for the financial year were R1 417 700 (common fixed costs). 2.2. Budgeted information for the 2022 financial year During the division's planning session for the 2022 financial year, the financial manager presented the following budgeted information and the related working papers regarding the optimisation of the constraint/ available production resources: 2.2.1. The division budgeted to produce and sell 260 000 BFs and 130 000 WFs. The required direct labour clock hours per unit will be equal to that of the 2021 financial year budget and the maize requirement is 0,5 kg per unit. 2.2.2. The variable selling costs per unit will be R0,50 per unit for both product types. 2.2.3 The financial manager also presented a summary of the detailed calculations performed for optimisation Establishing limiting factor(s) Details Maize (kilograms) Direct labour clock hours BF WF BF WF Total Required resources 130 000 65 000 26 000 19 500 45 500 Available resources 132 000 66 000 40 000 Surplus/ Shortage) 2 000 1 000 (5 500) Maize is not a limiting factor Direct labour hours are a limiting factor Application of linear programming Details Maize - primary ingredient Direct labour clock hours Equation 0,50BF +0,50WF S 198 000 kg 0,10BF +0,15WF $ 40 000 hours WF unit R19.00 R15.50 Determining the optimisation ranking Details Selling price Less: Total production costs Variable production costs Fixed production overheads Contribution Ranking BF unit R15,00 R12,50 R11,00 R1,50 R2,50 2 R 14,00 R1,50 R3,50 1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Core Concepts Of Accounting Information Systems

Authors: Nancy A. Bagranoff, Mark G. Simkin, Carolyn Strand Norman

11th Edition

9780470507025, 0470507020