Answered step by step

Verified Expert Solution

Question

1 Approved Answer

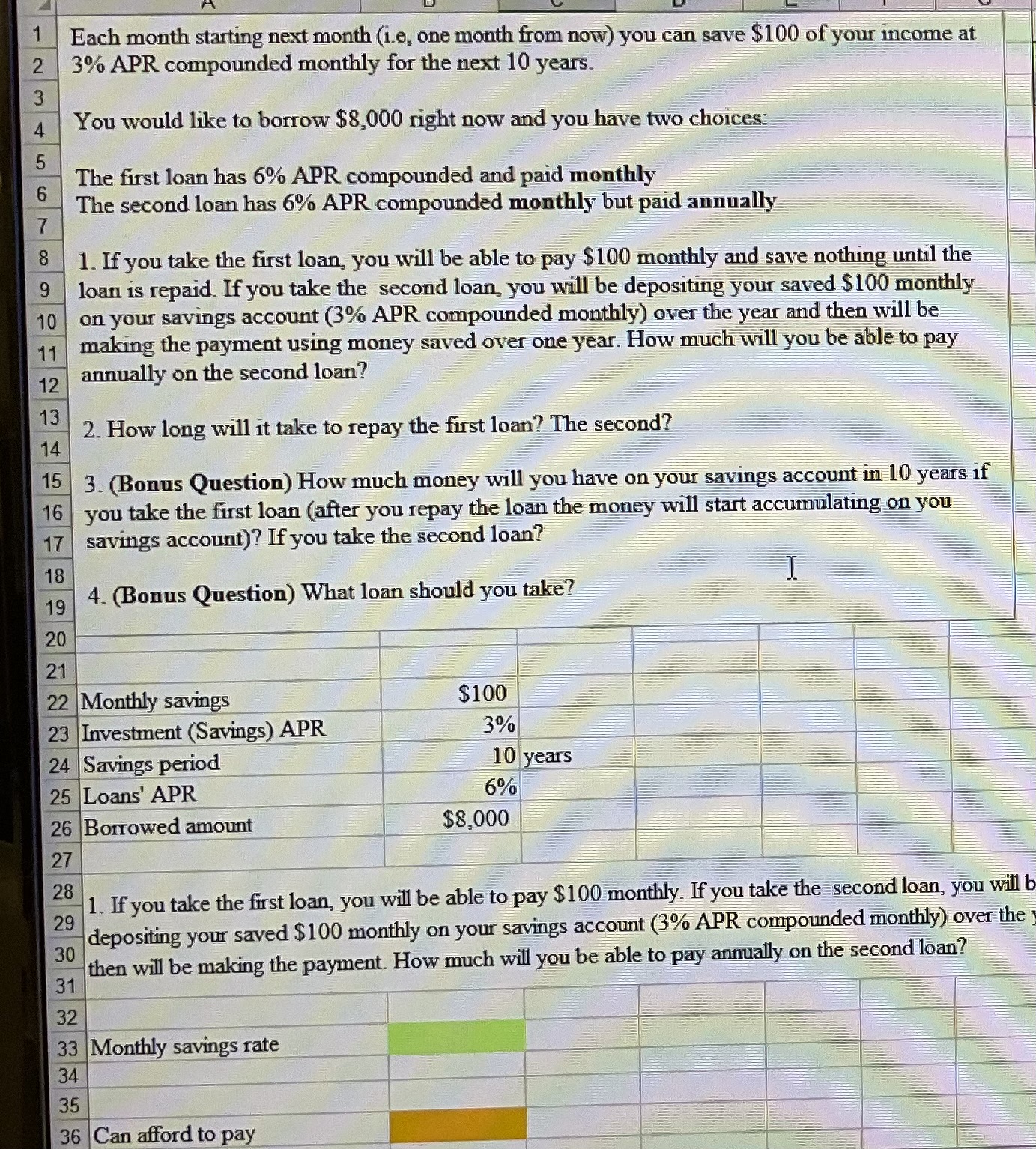

1. If you take the first loan, you will be able to pay $100 monthly and save nothing until the loan is repaid. If you

1. If you take the first loan, you will be able to pay $100 monthly and save nothing until the loan is repaid. If you take the second loan, you will be depositing your saved $100 monthly on your savings account ( 3% APR compounded monthly) over the year and then will be making the payment using money saved over one year. How much will you be able to pay annually on the second loan? 2. How long will it take to repay the first loan? The second? 3. (Bonus Question) How much money will you have on your savings account in 10 years if you take the first loan (after you repay the loan the money will start accumulating on you savings account)? If you take the second loan? 4. (Bonus Question) What loan should you take? 1. If you take the first loan, you will be able to pay $100 monthly. If you take the second loan, you will depositing your saved $100 monthly on your savings account (3\% APR compounded monthly) over the then will be making the payment. How much will you be able to pay annually on the second loan

1. If you take the first loan, you will be able to pay $100 monthly and save nothing until the loan is repaid. If you take the second loan, you will be depositing your saved $100 monthly on your savings account ( 3% APR compounded monthly) over the year and then will be making the payment using money saved over one year. How much will you be able to pay annually on the second loan? 2. How long will it take to repay the first loan? The second? 3. (Bonus Question) How much money will you have on your savings account in 10 years if you take the first loan (after you repay the loan the money will start accumulating on you savings account)? If you take the second loan? 4. (Bonus Question) What loan should you take? 1. If you take the first loan, you will be able to pay $100 monthly. If you take the second loan, you will depositing your saved $100 monthly on your savings account (3\% APR compounded monthly) over the then will be making the payment. How much will you be able to pay annually on the second loan

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Franchise Handbook A Complete Guide To All Aspects Of Buying Selling Or Investing In A Franchise

Authors: Atlantic Publishing Co

1st Edition

0910627541, 978-0910627542