Answered step by step

Verified Expert Solution

Question

1 Approved Answer

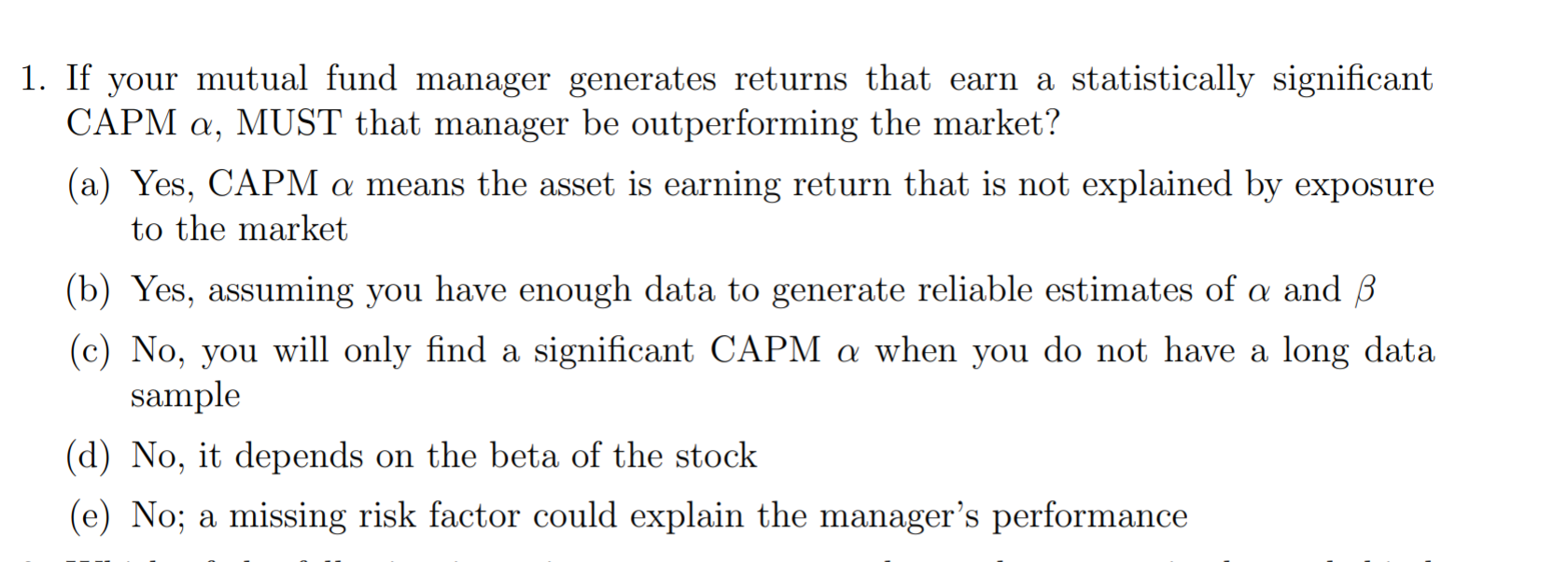

1. If your mutual fund manager generates returns that earn a statistically significant CAPM a, MUST that manager be outperforming the market? (a) Yes, CAPM

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Guide To Financial Modeling

Authors: Thomas S Y Ho, Sang Bin Lee

1st Edition

019516962X, 9780195169621