Answered step by step

Verified Expert Solution

Question

1 Approved Answer

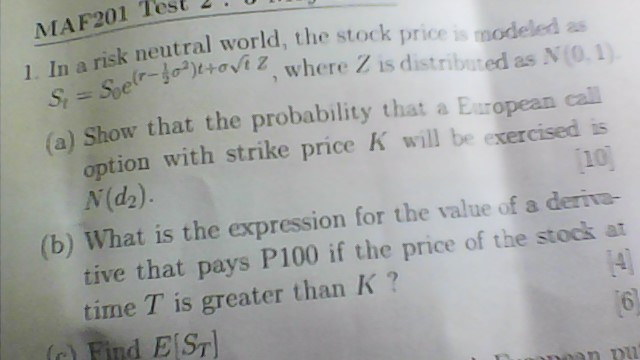

1. In a risk neutral world, the stock price is modeled a St=S0e(r212)t+tZ, where Z is distributed as N (a) Show that the probability that

1. In a risk neutral world, the stock price is modeled a St=S0e(r212)t+tZ, where Z is distributed as N (a) Show that the probability that a European cal option with strike price K will be exercised is (b) What is the expression for the value of 3 detive N(d2). tive that pays P100 if the price of the stocis time T is greater than K

1. In a risk neutral world, the stock price is modeled a St=S0e(r212)t+tZ, where Z is distributed as N (a) Show that the probability that a European cal option with strike price K will be exercised is (b) What is the expression for the value of 3 detive N(d2). tive that pays P100 if the price of the stocis time T is greater than K Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foreign Direct Investment Smart Approaches To Differentiation And Engagement

Authors: Daniel Nicholls

1st Edition

1409423573,1409471381