Question

1-. In the 1980s, Mr. Boesky made millions of dollars for himself and his investors by investing in take-over targets. Did he disprove the efficient

1-. In the 1980s, Mr. Boesky made millions of dollars for himself and his investors by investing in take-over targets. Did he disprove the efficient market hypothesis by predicting who would be take-over targets in the coming months?

2-What is the current situation of Ivan Boesky?

3- What happen to Dennis Levine, the banker who gave Ivan Boesky the insider information?

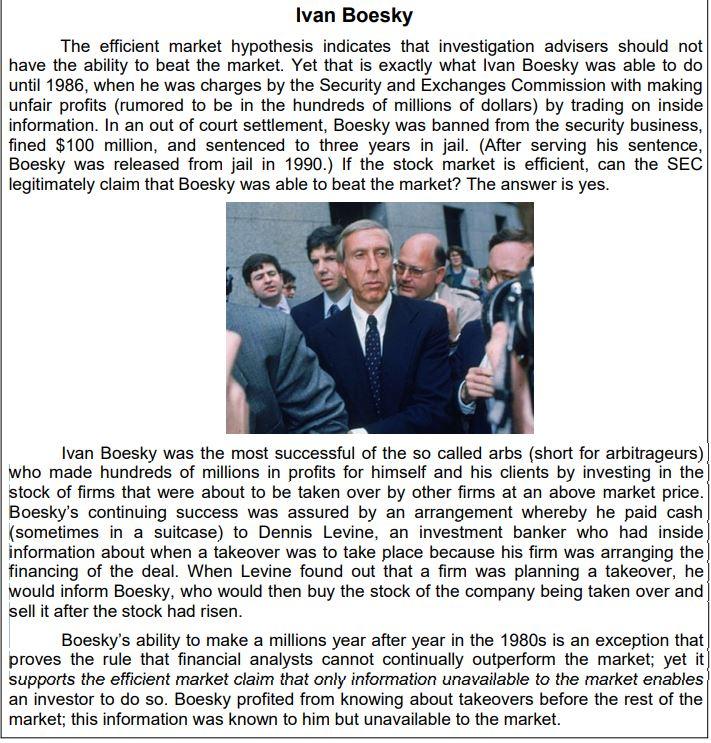

Ivan Boesky The efficient market hypothesis indicates that investigation advisers should not have the ability to beat the market. Yet that is exactly what Ivan Boesky was able to do until 1986, when he was charges by the Security and Exchanges Commission with making unfair profits (rumored to be in the hundreds of millions of dollars) by trading on inside information. In an out of court settlement, Boesky was banned from the security business, fined $100 million, and sentenced to three years in jail. (After serving his sentence, Boesky was released from jail in 1990.) If the stock market is efficient, can the SEC legitimately claim that Boesky was able to beat the market? The answer is yes. Ivan Boesky was the most successful of the so called arbs (short for arbitrageurs) who made hundreds of millions in profits for himself and his clients by investing in the stock of firms that were about to be taken over by other firms at an above market price. Boesky's continuing success was assured by an arrangement whereby he paid cash (sometimes in a suitcase) to Dennis Levine, an investment banker who had inside information about when a takeover was to take place because his firm was arranging the financing of the deal. When Levine found out that a firm was planning a takeover, he would inform Boesky, who would then buy the stock of the company being taken over and sell it after the stock had risen. Boesky's ability to make a millions year after year in the 1980s is an exception that proves the rule that financial analysts cannot continually outperform the market; yet it supports the efficient market claim that only information unavailable to the market enables an investor to do so. Boesky profited from knowing about takeovers before the rest of the market; this information was known to him but unavailable to the marketStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Makers And Takers The Rise Of Finance And The Fall Of American Business

Authors: Rana Foroohar

1st Edition

0553447238, 978-0553447231