Answered step by step

Verified Expert Solution

Question

1 Approved Answer

1. Less than, equal to, greater than 2. above, below, equivilent to 3. finite, infinite 4. mature, start up 5. mature, start up 6. A,B,C,D,E

1. Less than, equal to, greater than

1. Less than, equal to, greater than

2. above, below, equivilent to

3. finite, infinite

4. mature, start up

5. mature, start up

6. A,B,C,D,E

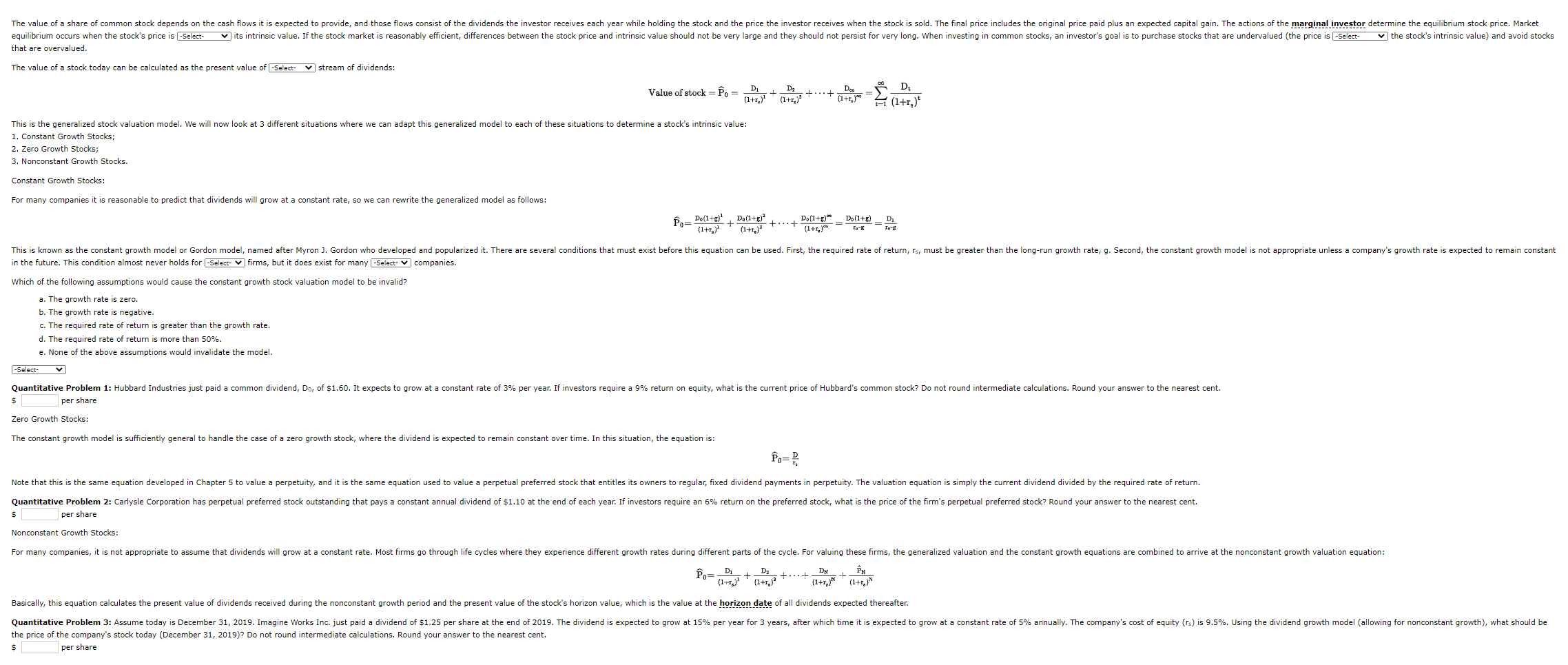

The value of a share of common stock depends on the cash flows it is expected to provide, and those flows consist of the dividends the investor receives each year while holding the stock and the price the investor receives when the stock is sold. The final price includes the original price paid plus an expected capital gain. The actions of the marginal investor determine the equilibrium stock price. Market equilibrium occurs when the stock's price is -Select its intrinsic value. If the stock market is reasonably efficient, differences between the stock price and intrinsic value should not be very large and they should not persist for very long. When investing in common stocks, an investor's goal is to purchase stocks that are undervalued (the price is -Select the stock's intrinsic value) and avoid stocks that are overvalued. The value of a stock today can be calculated as the present value of -Select- stream of dividends: D De Value of stock = PO D1 (1+r) D (1+r) This is the generalized stock valuation model. We will now look at 3 different situations where we can adapt this generalized model to each of these situations to determine a stock's intrinsic value: 1. Constant Growth Stocks; 2. Zero Growth Stocks; 3. Nonconstant Growth Stocks. Constant Growth Stocks: For many companies it is reasonable to predict that dividends will grow at a constant rate, so we can rewrite the generalized model as follows: for Do(1+8) D. (1+) Do(1+) +...+ + D. (1+) E-8 D TE This is known as the constant growth model or Gordon model, named after Myron J. Gordon who developed and popularized it. There are several conditions that must exist before this equation can be used. First, the required rate of return, rs, must be greater than the long-run growth rate, g. Second, the constant growth model is not appropriate unless a company's growth rate is expected to remain constant in the future. This condition almost never holds for -Select- firms, but it does exist for many -Select- companies. Which of the following assumptions would cause the constant growth stock valuation model to be invalid? a. The growth rate is zero. b. The growth rate is negative. c. The required rate of return is greater than the growth rate. d. The required rate of return is more than 50%. e. None of the above assumptions would invalidate the model. -Select- common dividend, Do, of $1.50. It expects to grow at a constant rate of 3% per year. If investors require a 9% return on equity, what is the current price of Hubbard's common stock? Do not round intermediate calculations. Round your answer to the nearest cent. Quantitative Problem 1: Hubbard Industries just paid $ per share Zero Growth Stocks: The constant growth model is sufficiently general to handle the case of a zero growth stock, where the dividend is expected to remain constant over time. In this situation, the equation is: Porr Note that this is the same equation developed in Chapter 5 to value a perpetuity, and it is the same equation used to value a perpetual preferred stock that entitles its owners to regular, fixed dividend payments in perpetuity. The valuation equation is simply the current dividend divided by the required rate of return. Quantitative Problem 2: Carlysle Corporation has perpetual preferred stock outstanding that pays a constant annual dividend of $1.10 at the end of each year. If investors require an 6% return on the preferred stock, what is the price of the firm's perpetual preferred stock? Round your answer to the nearest cent. $ per share Nonconstant Growth Stocks: For many companies, it is not appropriate to assume that dividends will grow at a constant rate. Most firms go through life cycles where they experience different growth rates during different parts of the cycle. For valuing these firms, the generalized valuation and the constant growth equations are combined to arrive at the nonconstant growth valuation equation: L fo=D D Dx + EN (1+1,)" (141)N Basica this equation calculates the present value of received during the nonconstant growth period and the present value of the stock's horizon value, which is value at the horizon date of all expected thereafter. Quantitative Problem 3: Assume today is December 31, 2019. Imagine Works Inc. just paid a dividend of $1.25 per share at the end of 2019. The dividend is expected to grow at 15% per year for 3 years, after which time it is expected to grow at a constant rate of 5% annually. The company's cost of equity (cs) is 9.5%. Using the dividend growth model (allowing for nonconstant growth), what should be the price of the company's stock today (December 31, 2019)? Do not round intermediate calculations. Round your answer to the nearest cent. $ per share The value of a share of common stock depends on the cash flows it is expected to provide, and those flows consist of the dividends the investor receives each year while holding the stock and the price the investor receives when the stock is sold. The final price includes the original price paid plus an expected capital gain. The actions of the marginal investor determine the equilibrium stock price. Market equilibrium occurs when the stock's price is -Select its intrinsic value. If the stock market is reasonably efficient, differences between the stock price and intrinsic value should not be very large and they should not persist for very long. When investing in common stocks, an investor's goal is to purchase stocks that are undervalued (the price is -Select the stock's intrinsic value) and avoid stocks that are overvalued. The value of a stock today can be calculated as the present value of -Select- stream of dividends: D De Value of stock = PO D1 (1+r) D (1+r) This is the generalized stock valuation model. We will now look at 3 different situations where we can adapt this generalized model to each of these situations to determine a stock's intrinsic value: 1. Constant Growth Stocks; 2. Zero Growth Stocks; 3. Nonconstant Growth Stocks. Constant Growth Stocks: For many companies it is reasonable to predict that dividends will grow at a constant rate, so we can rewrite the generalized model as follows: for Do(1+8) D. (1+) Do(1+) +...+ + D. (1+) E-8 D TE This is known as the constant growth model or Gordon model, named after Myron J. Gordon who developed and popularized it. There are several conditions that must exist before this equation can be used. First, the required rate of return, rs, must be greater than the long-run growth rate, g. Second, the constant growth model is not appropriate unless a company's growth rate is expected to remain constant in the future. This condition almost never holds for -Select- firms, but it does exist for many -Select- companies. Which of the following assumptions would cause the constant growth stock valuation model to be invalid? a. The growth rate is zero. b. The growth rate is negative. c. The required rate of return is greater than the growth rate. d. The required rate of return is more than 50%. e. None of the above assumptions would invalidate the model. -Select- common dividend, Do, of $1.50. It expects to grow at a constant rate of 3% per year. If investors require a 9% return on equity, what is the current price of Hubbard's common stock? Do not round intermediate calculations. Round your answer to the nearest cent. Quantitative Problem 1: Hubbard Industries just paid $ per share Zero Growth Stocks: The constant growth model is sufficiently general to handle the case of a zero growth stock, where the dividend is expected to remain constant over time. In this situation, the equation is: Porr Note that this is the same equation developed in Chapter 5 to value a perpetuity, and it is the same equation used to value a perpetual preferred stock that entitles its owners to regular, fixed dividend payments in perpetuity. The valuation equation is simply the current dividend divided by the required rate of return. Quantitative Problem 2: Carlysle Corporation has perpetual preferred stock outstanding that pays a constant annual dividend of $1.10 at the end of each year. If investors require an 6% return on the preferred stock, what is the price of the firm's perpetual preferred stock? Round your answer to the nearest cent. $ per share Nonconstant Growth Stocks: For many companies, it is not appropriate to assume that dividends will grow at a constant rate. Most firms go through life cycles where they experience different growth rates during different parts of the cycle. For valuing these firms, the generalized valuation and the constant growth equations are combined to arrive at the nonconstant growth valuation equation: L fo=D D Dx + EN (1+1,)" (141)N Basica this equation calculates the present value of received during the nonconstant growth period and the present value of the stock's horizon value, which is value at the horizon date of all expected thereafter. Quantitative Problem 3: Assume today is December 31, 2019. Imagine Works Inc. just paid a dividend of $1.25 per share at the end of 2019. The dividend is expected to grow at 15% per year for 3 years, after which time it is expected to grow at a constant rate of 5% annually. The company's cost of equity (cs) is 9.5%. Using the dividend growth model (allowing for nonconstant growth), what should be the price of the company's stock today (December 31, 2019)? Do not round intermediate calculations. Round your answer to the nearest cent. $ per shareStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen

17th Edition

126001391X, 978-1260013917