Question

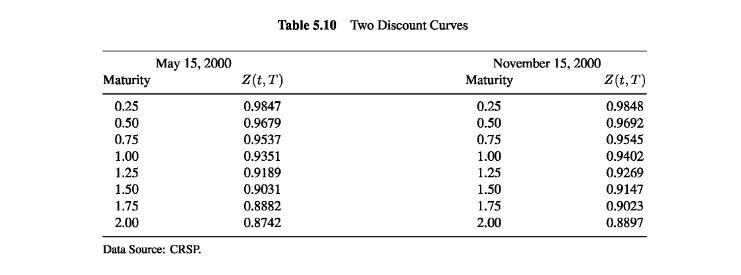

1. On May 15, 2000, a company is interested in purchasing $50 million worth of 1.5 -year zero coupon Treasuries with the proceeds of a

1. On May 15, 2000, a company is interested in purchasing $50 million worth of 1.5 -year zero coupon Treasuries with the proceeds of a sale of equipment to take place in 6 months. The company is interested in locking in the price of the Treasuries today through a forward contract.

Use the data in Table (note: the Maturity columns in the table should be interepreted as time to maturity, i.e. T-t) to answer.

A) What would the forward price be of the Treasuries?

B) How many bonds will the Company Purchase?

2. Consider Q1. Six months have now passed so that today is November 15, 2000. You want to calculate the payoff from being long the forward contract.

A) What is the amount of the payoff if you are long the forward contract?

B) Do you make money or lose money?

C) Assume that 3 months have passed after the forward contract initiation day and yoday is August 15,2000. What is the value of forward position on this day? Assume the discount curve on August 15,2000 is the same as the discount curve on November 15, 2000.

Table 5.10 Two Discount Curves May 15, 2000 November 15, 2000 Z(t, T) Z(t,T) 0.9848 0.9692 0.9545 0.9402 0.9269 0.9147 0.9023 0.8897 Maturity Maturity 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 0.9847 0.9679 0.9537 0.9351 0.9189 0.9031 0.8882 0.8742 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 Data Source: CRSPStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Social Economic And Environmental Impacts Between Sustainable Financial Systems And Financial Markets

Authors: Magdalena Ziolo

1st Edition

179981033X,1799810364