Answered step by step

Verified Expert Solution

Question

1 Approved Answer

( 1 point) Consider an n=1 step binomial tree with T=.5. Suppose r, the annualized risk-free rate is 4%, and delta, the annualized dividend rate

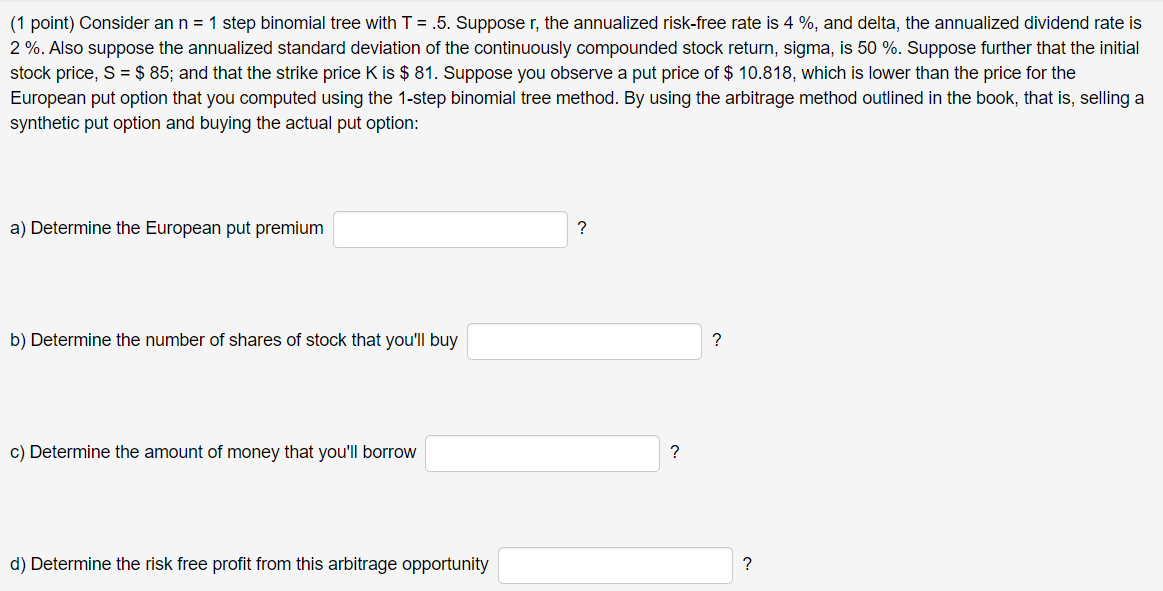

( 1 point) Consider an n=1 step binomial tree with T=.5. Suppose r, the annualized risk-free rate is 4%, and delta, the annualized dividend rate is 2%. Also suppose the annualized standard deviation of the continuously compounded stock return, sigma, is 50%. Suppose further that the initial stock price, S=$85; and that the strike price K is $81. Suppose you observe a put price of $10.818, which is lower than the price for the European put option that you computed using the 1-step binomial tree method. By using the arbitrage method outlined in the book, that is, selling a synthetic put option and buying the actual put option: a) Determine the European put premium ? b) Determine the number of shares of stock that you'll buy ? c) Determine the amount of money that you'll borrow ? d) Determine the risk free profit from this arbitrage opportunity

( 1 point) Consider an n=1 step binomial tree with T=.5. Suppose r, the annualized risk-free rate is 4%, and delta, the annualized dividend rate is 2%. Also suppose the annualized standard deviation of the continuously compounded stock return, sigma, is 50%. Suppose further that the initial stock price, S=$85; and that the strike price K is $81. Suppose you observe a put price of $10.818, which is lower than the price for the European put option that you computed using the 1-step binomial tree method. By using the arbitrage method outlined in the book, that is, selling a synthetic put option and buying the actual put option: a) Determine the European put premium ? b) Determine the number of shares of stock that you'll buy ? c) Determine the amount of money that you'll borrow ? d) Determine the risk free profit from this arbitrage opportunity Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stocks For The Long Run

Authors: Jeremy Siegel

6th Edition

1264269803, 978-1264269808