| 1. Prepare the consolidation entries. |

| 2. Create and Complete the consolidation worksheet, using formulas where applicable. Answer check: Consolidated NI attrib to NCS $17,680 Consolidated NI attrib to CI $344,420 EOY RE Parent = Consolidated = $840,480 Goodwill = $68,000 Total Debits=Credits =$885,700 End Noncontrolling Interest $162,520 |

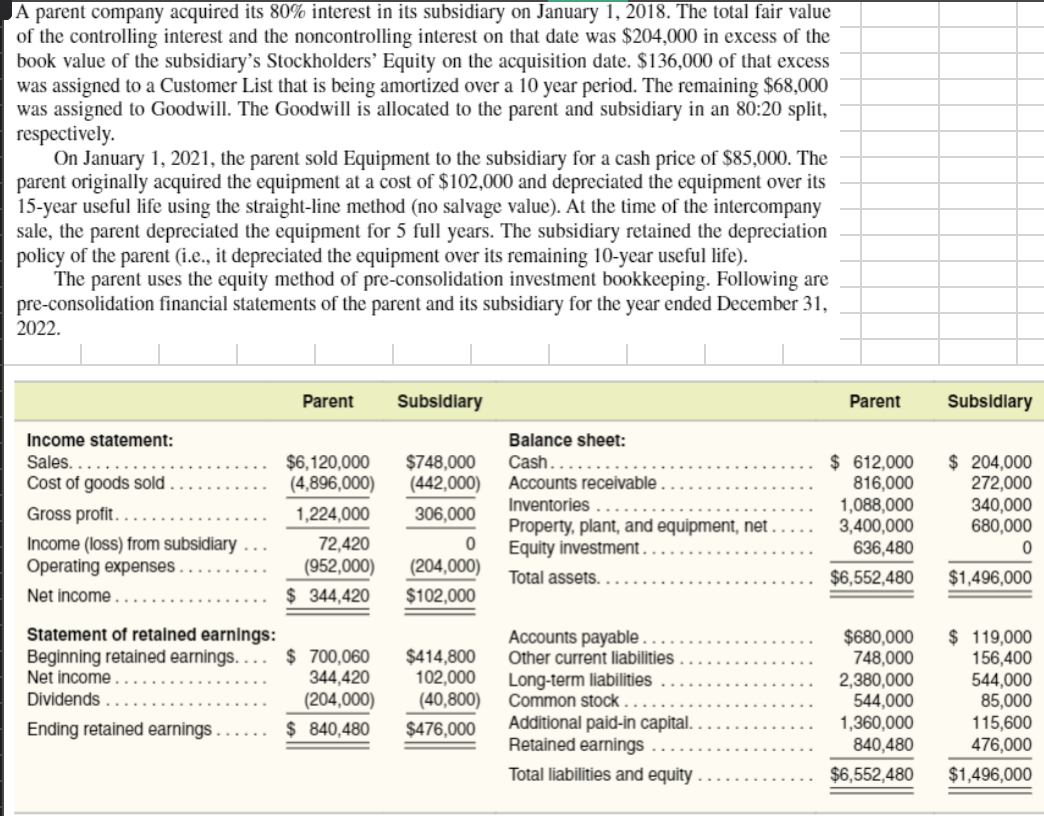

A parent company acquired its 80% interest in its subsidiary on January 1,2018 . The total fair value of the controlling interest and the noncontrolling interest on that date was $204,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. $136,000 of that excess was assigned to a Customer List that is being amortized over a 10 year period. The remaining $68,000 was assigned to Goodwill. The Goodwill is allocated to the parent and subsidiary in an 80:20 split, respectively. On January 1, 2021, the parent sold Equipment to the subsidiary for a cash price of $85,000. The parent originally acquired the equipment at a cost of $102,000 and depreciated the equipment over its 15-year useful life using the straight-line method (no salvage value). At the time of the intercompany sale, the parent depreciated the equipment for 5 full years. The subsidiary retained the depreciation policy of the parent (i.e., it depreciated the equipment over its remaining 10-year useful life). The parent uses the equity method of pre-consolidation investment bookkeeping. Following are pre-consolidation financial statements of the parent and its subsidiary for the year ended December 31 , A parent company acquired its 80% interest in its subsidiary on January 1,2018 . The total fair value of the controlling interest and the noncontrolling interest on that date was $204,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. $136,000 of that excess was assigned to a Customer List that is being amortized over a 10 year period. The remaining $68,000 was assigned to Goodwill. The Goodwill is allocated to the parent and subsidiary in an 80:20 split, respectively. On January 1, 2021, the parent sold Equipment to the subsidiary for a cash price of $85,000. The parent originally acquired the equipment at a cost of $102,000 and depreciated the equipment over its 15-year useful life using the straight-line method (no salvage value). At the time of the intercompany sale, the parent depreciated the equipment for 5 full years. The subsidiary retained the depreciation policy of the parent (i.e., it depreciated the equipment over its remaining 10-year useful life). The parent uses the equity method of pre-consolidation investment bookkeeping. Following are pre-consolidation financial statements of the parent and its subsidiary for the year ended December 31